It’s hard to believe it’s already been half a year since we started our search for exceptional businesses and investment opportunities for The Intrinsic Value Portfolio.

Time flies — and over these past months, we’ve analyzed 25 companies, breaking them down week by week in the newsletter and on the podcast.

We’ve come across plenty of impressive businesses, but only eight have made it into our portfolio so far. I know… we’re picky. But great investing is often more about knowing when to say no than when to say yes. Each position must strike the right balance between price and value.

Some companies are truly outstanding, but the price Mr. Market is asking today doesn’t make for a great investment. Others might not be world-class, but the valuation makes them compelling opportunities.

Today, we’re revisiting our current holdings, briefly walking through the theses and updating you on what’s changed since we first made the investment.

Naturally, this newsletter is a bit longer. Feel free to skip to the companies that interest you most. If you want to revisit the pitches, I’ve linked to the deep dive for each company.

— Daniel

The Intrinsic Value Portfolio: Mid-Year Review

Ulta Beauty – Beautiful, Steady Compounding

Ulta Beauty was the first company added to the Intrinsic Value Portfolio, and until recently, it was also one of the largest positions. But after a strong Q1 earnings report and a solid run in the stock, we decided to trim the position slightly, rebalancing it from 7% down to 5%. At our average entry price of just over $400, the stock has already delivered a high-teens percentage return.

I’ll elaborate later on how we think about selling or trimming positions, but for readers who haven’t heard the Ulta pitch yet, here’s a quick recap of the investment thesis. Ulta holds a unique position in retail, a tough industry, but it continues to outperform. It generates high returns on capital (25%+), operates a network of highly profitable stores with a strong value-added experience, and has arguably the most effective loyalty program in the sector.

Being from Europe, I’ve never actually set foot in an Ulta store. But Shawn keeps telling me that everyone he knows who’s even slightly into beauty loves the place, and the numbers back that up.

About 95% of sales come from loyalty members. In an industry where switching costs are essentially zero, that creates a meaningful edge. Even more impressive, 76% of those members shop exclusively in-store, which demonstrates how Ulta’s experience, from product testing to community events and in-store salons, differentiates it from traditional retailers, especially giants like Amazon and Walmart.

At the same time, Ulta has built a strong app-driven e-commerce business. In Q1, online sales grew 10% YoY, and over 60% of that came through Ulta’s app. Owning the traffic gives Ulta control over the customer journey.

Now to the recent earnings. As mentioned, the market reacted very positively. Revenue grew 4.5% YoY, driven mostly by a higher average ticket size, and comparable sales were up as well. Margins held up, and EPS came in ahead of guidance, prompting Ulta to raise its full-year outlook for both revenue and profit.

In 2025, growth was primarily driven by increases in the ticket size.

Tariffs came up as well, of course, hard to avoid these days. But Ulta is one of the companies that seems to have a handle on the situation.

They increased inventory by 11% to get ahead of potential cost increases, and thanks to their relationships with major brand partners, they’ve got some flexibility in managing those pressures. All in all, management expects only a limited impact, which helped them actually raise guidance. A positive surprise, and probably why the market liked the earnings a lot

Ulta also continues to return capital through buybacks, repurchasing 4 to 6% of outstanding shares each year. That steady capital return, combined with solid execution, continues to support the long-term case.

Alphabet – Outgrowing AI fears

Alphabet is currently the largest position in our portfolio, accounting for 8%. While the stock is down around 2% since our entry and 6% year-to-date, it has rebounded strongly, up nearly 20% from its April lows. That recovery followed a strong earnings report that challenged the AI-doom narrative hanging over Google’s core business.

Starting with the headline numbers from Q1: Revenue rose 12% to $90.2 billion, and net income surged 46% to nearly $35 billion. That translated into stronger margins despite continued heavy investment in AI infrastructure. Management also announced a 5% dividend increase and a new $70 billion share buyback authorization, signaling a commitment to return capital to shareholders while funding long-term growth.

From 2021 to 2024, Alphabet has now repurchased stock worth almost a quarter of a trillion dollars. That’s a lot, even for a company worth 2 trillion dollars.

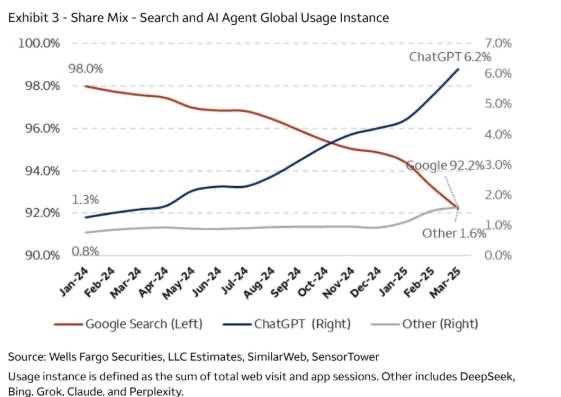

But what the market really cared about was Search. Despite all the headlines about ChatGPT and Perplexity chipping away at Google’s dominance, Search revenue still grew 10%. Google is losing some market share, but what matters is that overall search volume continues to increase. That’s one thing that the market, in our opinion, keeps ignoring. Looking at Google’s Search growth, it appears that overall search volume growth benefits Google more than losing market share in certain areas hurts the business. Otherwise, it wouldn’t grow.

What got us even more excited was hearing that Google’s AI-generated Search Overviews, already reaching 1.5 billion users each month, are being monetized at roughly the same rate as traditional search ads. Before, one bear argument has been that even if Google can gain market share through its AI search tool, monetization for those searches would be lower, so it would cannibalize its more profitable business. Apparently, that’s not the case.

But the market remains concerned. Especially since both Apple and Samsung reportedly explore partnerships with AI-first tools like Perplexity. There’s also speculation that Apple might not renew its agreement with Google, which keeps Google as the default search engine on iPhones, a deal worth around $20 billion per year.

Whether Apple will actually walk away from the Google deal is anyone’s guess. It might just be a negotiating tactic, a way to push for better terms or to show regulators that there’s more competition than they think. I’m not saying it was planned, but it’s worth noting that the comments came from Eddy Cue, Apple’s SVP, while testifying in the DOJ’s antitrust case against Google. That timing might not be a coincidence.

That said, there is no doubt that competition is increasing. Apple is even rumored to be eyeing a Perplexity acquisition.

Beyond Search, Alphabet is showing strength in two other major segments: Cloud and Waymo. Google Cloud revenue rose 28% in Q1, and operating margins nearly doubled to 18%. If margin expansion continues, as we’ve seen at AWS and Azure, Cloud could rival Search in value over the next decade. Alphabet is increasingly a business with multiple high-margin engines, not just an ad-funded search company.

Waymo is the other standout. The self-driving unit just crossed 10 million paid robotaxi rides, doubling its total in just five months. It now operates in Austin, LA, and San Francisco, completing around 250,000 rides per week, by far the leader in scale and safety. Uber partnerships help utilize that first-mover advantage.

To us, Alphabet today is a bet on a diversified set of highly cash-generative businesses — Search, YouTube, Cloud, and emerging bets like Waymo — with much of the downside already priced in.

Uber – Growing AV Fleets

Talking about Uber… its stock has been one of our strongest performers so far, returning over 40% from our average buy-in price of $62 per share. We initially established a 2% position.

Uber sits at the intersection of multiple powerful trends: autonomous driving, urban mobility, platform economics, and last-mile delivery. The big headline for 2025 was Uber’s deepening partnership with Waymo. Riders in Phoenix, Austin, and now Atlanta can order Waymo robotaxis directly through the Uber app.

If we dare to dream a bit into the future, this could reframe Uber not just as a ride-hailing company, but also as a demand aggregator. Waymo (and, in the future, other AVs) brings world-class AV technology but lacks Uber’s consumer interface and predictable volume. With 170 million monthly active users, Uber offers scale and efficiency, exactly what companies like Waymo need to reach commercial viability without building their own two-sided network. In the future, there might not just be Waymo but dozens of car brands with self-driving cars. Uber can then be the demand aggregator for all of them.

For Uber, the benefit is clear: lower costs, shorter wait times, and better margins. No driver means no commission. But more importantly, it turns a former existential threat — autonomous vehicles — into a tailwind. We are already seeing the beginnings. Starting in 2028, Uber will integrate Volkswagen’s autonomous vans into its LA operations.

Funny enough, I saw one of those VW vans in Hamburg just yesterday. It turns out that Hamburg is the city where VW already has these on the road for test drives. The one I saw still had a driver inside, a necessity for safety/regulatory reasons. I immediately googled after getting home, being sure that it would take years before they would be rolled out in Germany at scale (German/EU regulation is complex…). But I was wrong, next year they will be ready to go!

Back to Uber. When Shawn mentioned how many rides Uber facilitates, I initially thought I must have misheard. But I didn’t. The numbers are as insane as they sound… 3 billion rides just last quarter. That’s an increase of 18%, but even more notable is the operating income, which jumped to $1.2 billion, up by $1 billion(!) from the year before.

Hearing that Uber already facilitates 3 billion rides in a single quarter, you could think there’s no room for growth anymore. I mean, where should all these drives come from?

But today, only 5% of the adult population in Uber’s markets uses its services, and half of those users engage just once or twice per month. Meanwhile, cross-selling is improving: one-third of new Uber Eats users come from the rides app, and the Uber One subscription is making the ecosystem stickier across segments. So, onboarding new customers on either the mobility or delivery side will generate significantly more value in the future than it did a few years ago.

Add to that the ads business (no pun intended), which grew 60% to $1.5 billion in annual revenue. Still relatively small, but it’s a high-margin business, and with the incredibly valuable data Uber has, it’s an extremely compelling monetization lever, especially in mobility, where placement and timing matter.

Airbnb – Travel, Experiences, Services

Moving beyond the businesses directly tied to Google, let’s talk about Airbnb — a 5% position in our portfolio, currently up 6% from our average entry at $132 per share. While the stock has barely moved since its IPO in 2020, down 3% in over four years, the underlying business tells a much more compelling story. Airbnb has matured into a highly profitable platform, growing free cash flow at a 25% CAGR since 2020 and now trading at a reasonable 16x EV/OCF.

We have no earnings updates to discuss, but a couple of weeks ago, we received another big announcement. Airbnb introduced its (kind of) new Services and Experiences offerings. It’s more of a relaunch and expansion of the original 2016 initiative. When you now open the Airbnb app, you’ll see these new features that are rolled out across 650 cities for Experiences and 260 cities for Services. The goal is to expand Airbnb’s use case beyond just accommodations, transforming it into a comprehensive travel and lifestyle platform.

Experiences now include everything from local cooking classes and museum tours to niche cultural events like ramen-making or beach workouts. All hosted by locals. Services, on the other hand, focus on in-home offerings like chefs, massage therapists, personal trainers, and hairstylists, all vetted for quality, of course.

The updated Airbnb App

This move aims to capture more spend per user by boosting engagement within the app, and potentially setting the stage for future recurring revenue models, such as a subscription that combines perks across bookings, services, and experiences. How about… “Airbnb Plus”? And, like almost every other company we are discussing, it also offers the opportunity to introduce an advertising business.

What makes this new attempt to implement Experiences to Airbnb more promising is that the company now has the scale and operational maturity to pull this off. It has over $10 billion in cash and continues to generate substantial free cash flow.

In my mind, these updates could be a major new growth driver. Rather than just monetizing nights booked, Airbnb is now positioned to monetize the entire trip, and possibly even the time between trips. But it remains to be seen whether the Experience and Service offers are good enough to satisfy customers long-term. Combined with the strong financial foundation and still-reasonable valuation, we are happy with the position.

Adobe – Generating Billions despite Generative AI

Adobe is a 5% position in our portfolio and has gained around 10% since we initiated it at an average price of $380. While the stock has moved sideways over the past five years, largely due to concerns surrounding generative AI, Adobe’s latest earnings report reaffirmed why we believe those concerns are overblown.

The company reported record revenue of $5.87 billion in Q2, up 11%, and non-GAAP EPS of $5.06, up 13%. Operating cash flow reached a quarterly record of $2.19 billion, and Adobe repurchased 8.6 million shares, with over $10 billion still remaining under its authorization. Similar to Alphabet, this means that more than 10% of the outstanding shares have been repurchased since 2021.

Quite a lot of numbers, I know. But I think there are few better things than stating the facts when you try to figure out whether a business is in the process of getting disrupted.

For Adobe, all core segments delivered, especially those involving AI. Digital Media revenue grew 11%, bringing ARR to $18.1 billion, while monthly users of Acrobat and Express rose over 25%. On the enterprise side, Digital Experience revenue increased 10%, with standout growth in GenStudio and Firefly Services (Adobe’s AI products), both growing ARR at triple-digit rates. In other words, Adobe seems to be benefiting, not suffering, from the AI-driven wave of creative work.

The thesis for Adobe is pretty straightforward: most AI models are trained on unlicensed data. For enterprise customers, this could result in expensive lawsuits should a copyright dispute ever arise. Adobe has trained its Firefly models on licensed data, ensuring that such an incident can never happen.

Another key advantage for Adobe is how deeply integrated it is into the full creative workflow. Setting up a full-scale marketing campaign is more complex than it might seem, and Adobe’s ecosystem, from design to production to analytics, plays a role at every stage. That kind of end-to-end involvement creates a real moat through switching costs.

That said, AI is moving fast. It’s possible that other companies will build powerful tools that can replicate some — or even many — of Adobe’s features. But replicating the entire ecosystem? That’s much more difficult. And even then, competing tools don’t just need to be as good. They’d need to be significantly better to convince users to switch everything over.

Right now, Adobe is priced as if disruption is the more likely scenario. But the numbers suggest otherwise. With more than 90% recurring revenue, a capital-light model, and a mid-20s ROIC, it remains a cash machine. At a 4% FCF yield (adjusted for SBC) and less than 18x forward earnings, we still see Adobe as an undervalued compounder.

Reddit – Fast (and Profitable) Growth

Reddit is one of the smaller positions in our portfolio at 3%. It’s a high-growth opportunity, but naturally comes with a wider range of outcomes. The stock has rebounded sharply from its April lows and is now up more than 60% from our entry price.

If you’ve listened to our deep dive on Reddit, you’ll know I’ve voiced some reservations about the product itself — I’m just not much of a social media person. But clearly, most people are, and Reddit’s numbers confirm this.

Revenue grew by more than 60%, driven by strong growth in daily active users and Average Revenue per User (ARPU), as well as strong momentum in contextual advertising. Another impact has been the high-margin revenue from data licensing to AI companies, which now accounts for approximately 10% of total revenue.

International expansion has also picked up momentum. Thanks to AI-powered translations, traffic outside the U.S. rose 41%. That growth is led by markets like Brazil, where daily active users grew over 80%. The downside is that the ARPU remains significantly lower internationally, approximately $1.30, compared to over $6 in the U.S., but that is expected at this stage. The long-term bet is that this gap will narrow over time, especially in developed markets like Europe.

What continues to set Reddit apart is its uniquely human content. In a world increasingly shaped by generative AI, Reddit delivers something AI can’t easily replicate: real communities, authentic conversations, and feedback. So, while most companies benefit from using more AI, for Reddit, it’s somewhat the opposite.

Looking ahead, there are multiple monetization levers to scale:

Paid communities and marketplace features

Further ad platform development

Growth in international ARPU

Deeper AI data licensing partnerships

All of this supports a long growth runway. That said, we believe the current valuation already reflects a significant portion of that potential. Thus, we wouldn’t be buyers at current levels. But we’re also not planning to trim the position. Reddit has earned its spot in the portfolio.

Nike – Back on Track?

Despite being such a well-known and globally recognized brand with decades of flawless execution, Nike might be one of our riskiest positions. We initiated a 2% position in the mid-50s in the midst of the tariff turmoil. The brand is iconic, but its fundamentals remain under pressure. Since our entry, the stock has risen by around 25%, including a sharp 15% jump on Friday following Thursday’s earnings report.

Let’s be clear, though, the numbers weren’t great. In fact, they were terrible, and if the stock had been down 10% after, it would’ve been no problem to explain that as well. The only thing Nike had going for it was that expectations were incredibly low.

But the rally was likely not just about beating estimates. It was about early signs that the long-awaited turnaround might finally be taking shape.

Let’s quickly run through the numbers. We don’t need to dig deep to see that this quarter was rough. It delivered exactly what it promised — a mess. Revenue declined 12% to $11 billion, with decreases across all geographies and segments. China was hit the hardest, but Europe and the US declined in the low double digits as well. Nike Direct dropped 14%, mainly due to a sharp decline in the digital channel. Gross margins shrank by 440 basis points to just above 40%. EPS came in at $0.14, down 86%, yet still somehow managed to beat expectations.

So why did the stock rally? Mainly because early signs from Nike’s “Win Now” strategy, introduced last year by Elliott Hill, are beginning to show progress. According to management, newer products, particularly in the Running and Training Categories, are gaining traction. Discounts helped move aged inventory, and Nike is now seeing a higher share of full-price sales on the Direct channels.

Another reason the market reacted positively was due to tariff announcements. Similar to Ulta, Nike announced that the $1 billion in estimated tariff-related costs are expected to be “fully mitigated” through changes in the sourcing mix, supplier negotiations, and selective price increases. This helped ease some macro concerns.

But it’s not enough to materially boost next quarter’s numbers. Nike expects revenue to decline by mid-single digits in Q1 FY26, with gross margins compressing another 350 to 425 basis points. The second half of the fiscal year is when Nike expects to regain momentum and shift back to growth.

I know this might sound very bearish for a report that sent the stock up 15%. But looking at these numbers, I would lie if I portrayed this as a fantastic quarter. Still, we invested in Nike with the belief that the brand’s long-term strength would prevail and that the business would recover. These results don’t yet mark the turnaround, but they may mark the bottom. Momentum could be turning. We’re willing to be patient, but we won't pretend that the problems have disappeared.

Nubank – Revolutionizing LatAm Banking

Nubank is the latest addition to our portfolio — a 2% position initiated at just under $12 per share. Admittedly, it’s a bit outside our core circle of competence, but the numbers were simply too compelling to ignore. We believe it’s worth taking a calculated risk.

The unit economics are exceptional, with a customer lifetime value estimated to be 20–30 times higher than the acquisition cost. ARPAC (average revenue per active customer) currently sits at $10.70, rising to $25 in more mature cohorts. Operating margins are already at 25%, with a clear path toward 30%. Unlike legacy banks, Nubank operates without the costly branches and infrastructure typically associated with traditional banking. It serves 9,000 clients per employee, versus just 1,000 at traditional banks, and its customer acquisition costs are up to 58 times lower.

There’s still a massive growth runway ahead. Nubank has only captured about 5% market share across Brazil, Mexico, and Colombia. In Mexico, for instance, where credit card penetration is just 12%, over 20% of smartphone users have already applied for a Nubank product. That’s a strong sign of brand strength and distribution efficiency.

Of course, risks remain. 90-day non-performing loans have climbed to 7.7%, above the industry average of 5.5%, and a macroeconomic slowdown could test the resilience of the loan book. That said, Nubank worked on improving the credit mix. Nubank expanded its secured lending portfolio by over 600% last year, now representing a quarter of its total loans. It’s also expanding into lower-risk categories, such as payroll financing.

There’s a lot to unpack here. Just yesterday, we hosted a 90-minute deep dive in our Intrinsic Value Community to go through the full investment case. Since there haven’t been any major updates recently, though, I’d point you to our podcast episode and the full write-up in the newsletter archive if you want to dig into the thesis.

Portfolio Construction

One of the most common questions we get is: Why do we keep positions relatively small, even when you still have plenty of cash on the sidelines?

One reason is that this approach helps us clearly communicate our conviction levels. Our rough framework is to own around 20 equally weighted positions, which implies a 5% target weight per company. That 5% acts as a yardstick. If we believe an investment opportunity is truly exceptional, with a favorable risk-reward, we consider going above 5%. If the business is more uncertain or the upside more speculative, we size it below.

Just as our company deep dives also aim to teach the valuation process, our portfolio is meant to teach the process of building a portfolio from scratch. We want this podcast and newsletter to show what it looks like to build a portfolio in real time. You can find hundreds of “mature” portfolios online. What’s more interesting is seeing the decision-making in action. Why is this a 3% position, and that one 8%? How do we decide what to hold, trim, or pass on?

Of course, we’ll make mistakes along the way. We’ve already made some mistakes of omission. A great example is Nintendo, a great company that we should’ve bought but didn’t. We will make more such mistakes. And both you and we will learn from it.

Importantly, we don’t have a ready-made list of 20 great ideas (I’d love to have such a list, haha). If we did, we wouldn’t need to pitch a new company every week. Right now, we own eight. And maybe we’ll stop at 15. If we don’t find enough high-conviction opportunities, we won’t force it. We’ll just own fewer names and size them more assertively.

As for what types of companies we look at, long-time listeners know we’re pretty open. We’ve pitched fast-growers and slower compounders, large-caps and mid-caps, U.S. names and some emerging market plays.

That said, our current portfolio does have a slight bias toward large-cap, U.S.-based, asset-light businesses with strong platforms or tech leverage. That wasn’t our goal, but it reflects where we’ve found the best ideas recently. Companies like Alphabet, Adobe, and Uber are trading at attractive valuations, not because they’re broken businesses, but because the market fears disruption from AI, automation, and platform shifts. In each case, we believe those fears are overstated — or, in some cases, that the company is actually a beneficiary of the trend.

To be clear: this is not a buy-everything-we-pitch kind of portfolio. In fact, it’s quite the opposite. Reddit, Airbnb, and Uber are all companies we like, but that doesn’t mean we’d buy them again at today’s prices. If we get another drawdown, we might.

Ultimately, this is the theme of investing: Price matters. Many companies we cover are phenomenal businesses. The key is buying them at the right price. That’s what we’re trying to do here, and what we hope to help you do, too.

Weekly Update: The Intrinsic Value Portfolio

Notes

If you'd like us to revisit some of the companies we've put on our watchlist and highlight the most interesting ones, let us know by leaving a comment!

Quote of the Day

"The essence of portfolio management is the management of risk, not the management of returns. Well-managed portfolios start with this precept.”

— Benjamin Graham

What Else We’re Into

📺 WATCH: We Study Billionaires: The Mindset and Skills That Build Investing Legends w/ Ian Cassel

🎧 LISTEN: Richer, Wiser, Happier: Winning Ways w/ Bill Nygren

📖 READ: The new Memo by Howard Marks: More on Repealing the Laws of Economics

You can also read our archive of past Intrinsic Value breakdowns, in case you’ve missed any, here — we’ve covered companies ranging from Alphabet to Airbnb, AutoZone, Nintendo, John Deere, Coupang, and more!

Your Thoughts

Which is your favorite Position of The Intrinsic Value Portfolio?

See you next time!

Enjoy reading this newsletter? Forward it to a friend.

Was this newsletter forwarded to you? Sign up here.

Use the promo code STOCKS15 at checkout for 15% off our popular course “How To Get Started With Stocks.”

Follow us on Twitter.

Read our full archive of Intrinsic Value Breakdowns here

Keep an eye on your inbox for our newsletters on Sundays. If you have any feedback for us, simply respond to this email or message [email protected].

What did you think of today's newsletter?

All the best,

© The Investor's Podcast Network content is for educational purposes only. The calculators, videos, recommendations, and general investment ideas are not to be actioned with real money. Contact a professional and certified financial advisor before making any financial decisions. No one at The Investor's Podcast Network are professional money managers or financial advisors. The Investor’s Podcast Network and parent companies that own The Investor’s Podcast Network are not responsible for financial decisions made from using the materials provided in this email or on the website.