Can the “Magnificent 7” offer value? Depends on how you define value. They’d probably be too rich for ol’ Ben Graham’s tastes, but boy, they have done well. It’s not just their stocks running up unfoundedly, either — these are (mostly) incredibly profitable businesses with resilient revenue streams and inspiring growth prospects.

Tesla and Nvidia aside, my interest is in the less sensationally priced Cash Cows of the Mag7: Apple, Microsoft, Meta, Amazon, and Alphabet.

In particular, Alphabet has caught my eye because, well, I cannot imagine a business with a bigger moat than Google. How many companies are so synonymous with the service they provide that their name is also a commonly used verb describing what they do? (i.e., “I’m going to Google that!”)

That is almost always a good indicator of how dominant a company is in its space. I am embarrassed to say, though, that I had never dug deeply into understanding the nuances of Google’s parent company, and so, I recently began my ~search~ for value in Alphabet, pouring through the company’s financial statements.

What I found, below:

— Shawn

Alphabet: More Than Google

Where to begin? I can hardly imagine saying something unique about Alphabet that hasn’t already been covered by the scores of analysts who have tracked the company for far longer than I have, but for fun, let’s start with some eye-popping statistics:

Alphabet controls 92% of the global search engine market, making it by far the most-visited website on earth, generating 9 billion searches each day from over 4 billion users(!)

More than 1.5 billion people use Gmail, while YouTube has over 2.5 billion active users — 50% of American adults visit YouTube on a daily basis(!)

YouTube is so big that its search engine is the second largest in the world behind Google — roughly 400 hours of content are uploaded onto YouTube every 24 hours, adding to the 1 billion hours+ of content already on the site(!)

Not to be outshined by YouTube’s massive amount of data, Google Maps contains some 21 petabytes of satellite imagery — the equivalent of 330,000 64-gigabyte smartphones(!)

With all of these billions of users across different platforms, from Gmail to YouTube to Maps to Search, imagine all of the different ways Alphabet can further monetize these assets. Not to say I expect them to start charging regular people for Gmail, but there is room to charge more to businesses using Google Workspace, for example, or to perhaps charge higher licensing fees to companies like Uber that rely on the Google Maps API to power their navigation-based app.

The point is, with so much data and control over widely relied-upon platforms, that gives them ample room to expand into adjacent business models or to more aggressively monetize their existing revenue streams.

But those stats above hardly do any justice to how big Alphabet is, which is the conglomerate that not only owns Google and YouTube but also a range of related and less-related businesses.

Driving Is So 20th Century

What other businesses, you ask? Far from Alphabet’s most ambitious project, Waymo is perhaps the closest to becoming a major, viable unit. If you live in Austin or San Francisco, you’ve probably seen these autonomous vehicles whipping around, and maybe you’ve even hailed them for a lift.

Waymo vehicle

Waymos are incredibly impressive and, depending on who you ask in the industry, are typically seen as the leader in self-driving vehicle technology, rivaled namely by Tesla.

This technology promises not just to disrupt global vehicle markets but also derivative industries like trucking and ride-sharing. Consider, for a moment, the advantages of Waymo over Uber and Lyft.

Assuming Alphabet doesn’t eventually cut Uber out of the picture altogether and continues to partner with them, this would be a major upgrade for Uber’s network. Fleets of autonomous vehicles may make rides cheaper and thus even more popular since they strip out the human labor cost of drivers and the need for tips.

Additionally, parents of teenagers or younger school-aged children may happily pay for Waymo-powered Ubers to transport their kids back and forth from school, sports practices, and friends’ houses, to an extent parents might not be comfortable with when still facing the prospect of putting their beloveds in a vehicle with strangers.

Or imagine all the women who might breathe easier knowing that their late-night Uber won’t subject them to the anxiety of being chauffeured by strange men, thanks to Waymo.

The Cool Conglomerate

Alphabet is working on a ton of cool stuff besides Waymo, from Verily, which is devoted to researching new life-sciences technology, to Isomorphic Labs, which is working to discover new types of drugs with AI, and Calico, a research company devoted to overcoming age-related diseases.

Then, there’s Capital AG and GV, Alphabet’s private equity and venture capital funds managing tens of billions of dollars of investments in tech companies like Duolingo, Nest, Slack, and GitLab.

There’s also Google Fiber, a high-speed internet provider, as well as Wing, a drone-based delivery service that works with companies like Walmart to deliver groceries and other orders — supposedly, the technology is so precise that the drones can deliver hot coffee without any spillage.

Alphabet’s Wing drones making deliveries

What I love is that, unlike in traditional conglomerates where there can be a real degree of bureaucratic bloat that creates redundancies, many of Alphabet’s businesses benefit from their interconnections.

Waymo, for example, surely benefits from having access to Google Maps’ petabytes of data, and Waymo’s mapping of data on the ground can go toward improving Maps, too. Or, perhaps researchers using AI to cure certain diseases can get access to the most cutting-edge internally available AI models that aren’t otherwise publicly available.

With the vast amount of data and technology at Alphabet’s fingertips, you can imagine many different ways that the things one team is working on can complement something another division is doing.

This all illustrates the greater point that Alphabet embraces the solution to the innovator’s dilemma: as an incumbent tech leader, it’s constantly looking for the next disruptive technology, which it either incubates in-house with independent subsidiaries or invests in through its VC & PE funds.

Their track record of success with the widespread adoption of Google Search, YouTube, Docs, Sheets, Maps, Gmail, Android operating systems and devices, and more speaks for itself.

Bread And Butter

The above ventures, like Wing, are Alphabet’s so-called “Moonshot Bets,” and these are mostly money-losing endeavors that aim to be the next big thing. But the current big things for Alphabet are Search and YouTube.

Google Search is monetized primarily via sponsored search results. You ask Google for the best place in town to get a new suit, and local stores pay a premium to have their store recommended first. Interestingly, though, about 80% of Google searches aren’t monetized, meaning there is seemingly considerable room to keep expanding sponsored results and growing this $100 billion+ business.

Think of everything you search, clearly not every type of search is created equal. Some, like the suit example, are easily monetizable, while others, like “Who was the 38th president?” aren’t as fertile digital real estate.

YouTube also has a major advertising business. This is pretty intuitive because we’ve all opened up a video and been subject to a 5-second ad.

And then there’s AdSense, the advertising marketplace Alphabet runs, enabling website publishers to earn money from the eyeballs they get. Websites can opt into AdSense and get paid for their traffic, while Alphabet takes a chunky fee for connecting them with relevant advertisers who they might not otherwise be able to work with.

Banner ads like these are common through AdSense

Even Google Maps is monetized by advertising. Businesses can pay to have their addresses more prominently displayed on maps and suggested in searches. Unsurprisingly, then, around two-thirds of Alphabet’s revenues are tied to advertising. Advertising is very much Alphabet’s bread and butter, as they say.

With data on what just about everyone is doing, searching for, and shopping for, as well as billions of users across their platforms, advertising is a natural focus for the company.

The New Bread And Butter?

But advertising is cyclical. When the economy turns down, the first thing companies do is slash their marketing budget. It’s a way more palatable option than laying people off, which comes eventually but isn’t the first response typically to a business slowdown.

That makes Alphabet vulnerable, for even though YouTube’s ad-supported revenues and Google Search are vastly different products, they aren’t diversifying from a business mix perspective. They both rely heavily on digital advertisers continuing to spend on digital advertising.

Naturally, Alphabet is looking to minimize that cyclicality, and they’ve had great success in that thus far. Over 100 million people pay for YouTube Premium, giving them unfettered, ad-free access to an ocean of user-created content.

Side note: What’s great about YouTube from Alphabet’s perspective is that creators are doing all of the work creating the content and promoting it, while Alphabet passively pays them a percentage of all revenues received.

Contrast that with Netflix, which takes on the costly challenge of producing popular but short-lived content itself or purchasing the rights to existing shows and movies while having to do much of the marketing for this content.

On top of subscriptions to YouTube Premium, there’s also YouTube TV — a higher-priced service with more than 8 million subscribers meant to rival cable bundles, with channels like ABC, ESPN, Fox, AMC, and live sports.

YouTube is a lot of different things in one. In a way, it’s a blend of Netflix, cable, Spotify (video podcasts/YouTube Music), and TikTok (YouTube Shorts).

Beyond YouTube, there’s Google Cloud, arguably the most exciting part of the company and the source of much of its growth. Cloud is an enigmatic buzzword used loosely, but in short, it refers to outsourcing one’s computing power and storage.

An Alphabet data center

Alphabet has massive data centers and supercomputers that businesses can pay to tie into, effectively renting out computing resources at a tremendous scale.

And we haven’t even gotten to Google devices yet. Alphabet sells millions of smartphones and other smart devices annually through its Pixel brand, while the Android operating system is so widely used on mobile devices — from Pixel to Samsung — that it runs on roughly 70% of all mobile devices globally.

As a result, the Google Play app store is a huge moneymaker, too, since app developers end up paying Alphabet a commission for every purchase made — either in paying for the app initially, recurring subscriptions, or supplemental in-app purchases.

All of these different revenue streams and more round out Alphabet’s business model, diversifying its revenues across wide-moat businesses and contributing to its all-around “quality.”

The real advantage is Alphabet’s sheer scale. It could spend just 5% of its revenues on the research & development of new products or features, and that would still be roughly $16 billion — more than 100% of most listed tech companies’ revenues outside of the Mag7. In other words, Alphabet can devote a small percentage of its revenues to innovation and still be investing billions of dollars into future growth.

You can see why, then, so much power has been concentrated at the top of the tech world. No one can afford to spend nearly as much on data centers, researchers, or top programmers or absorb losses on unproven but promising, world-changing technologies to the same extent.

In reality, Alphabet actually spends closer to $44 billion on R&D…that’s pretty hard to compete with.

Valuing A Conglomerate

This is all well and good, but the question we want to answer is, as always: What is this company worth?

The best approach here is probably to breakout the company’s different business units separately, try to value them on their own, and sum everything back together.

How you carve out the business units is arbitrary. Maybe you value YouTube’s ad business separately from its subscription business, or you value YouTube as a single entity that includes both revenue streams.

For the sake of simplicity, I followed how Alphabet disaggregates its units, but I’ve seen others do the extra work to compile the financial results in a way that makes better sense to them (the way Alphabet divides things up is fairly confusing.)

What Search Is Worth

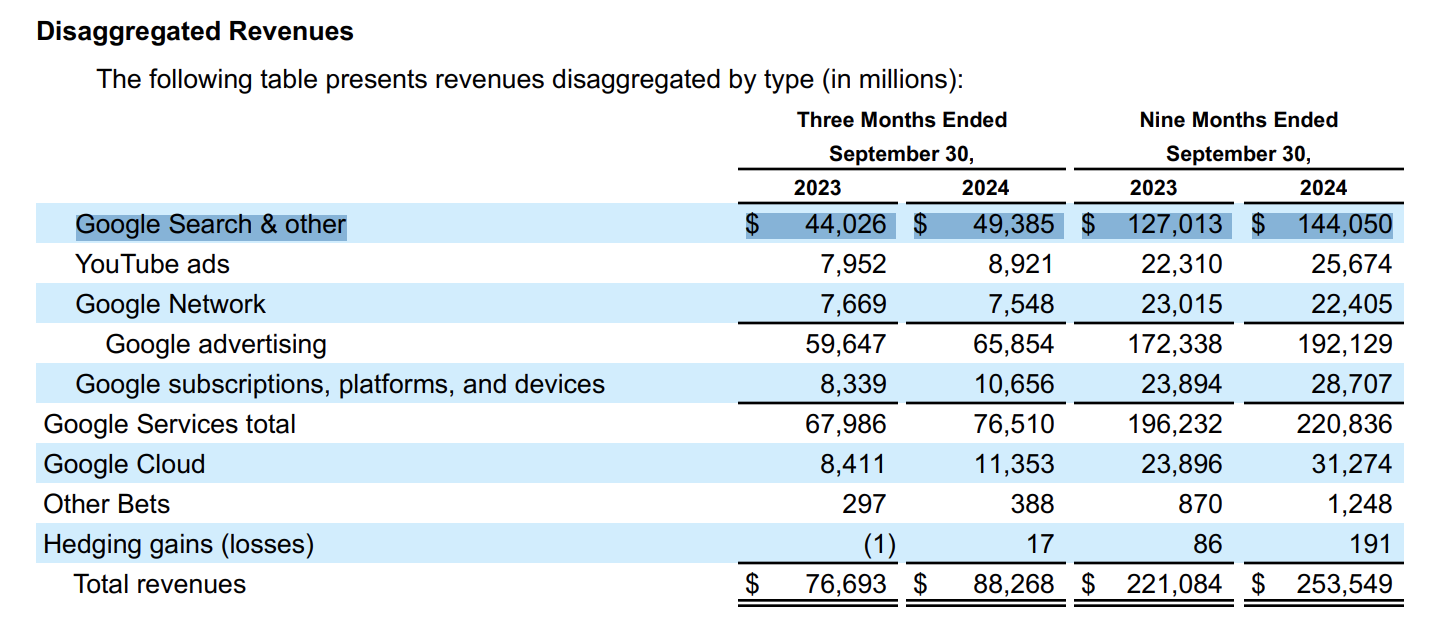

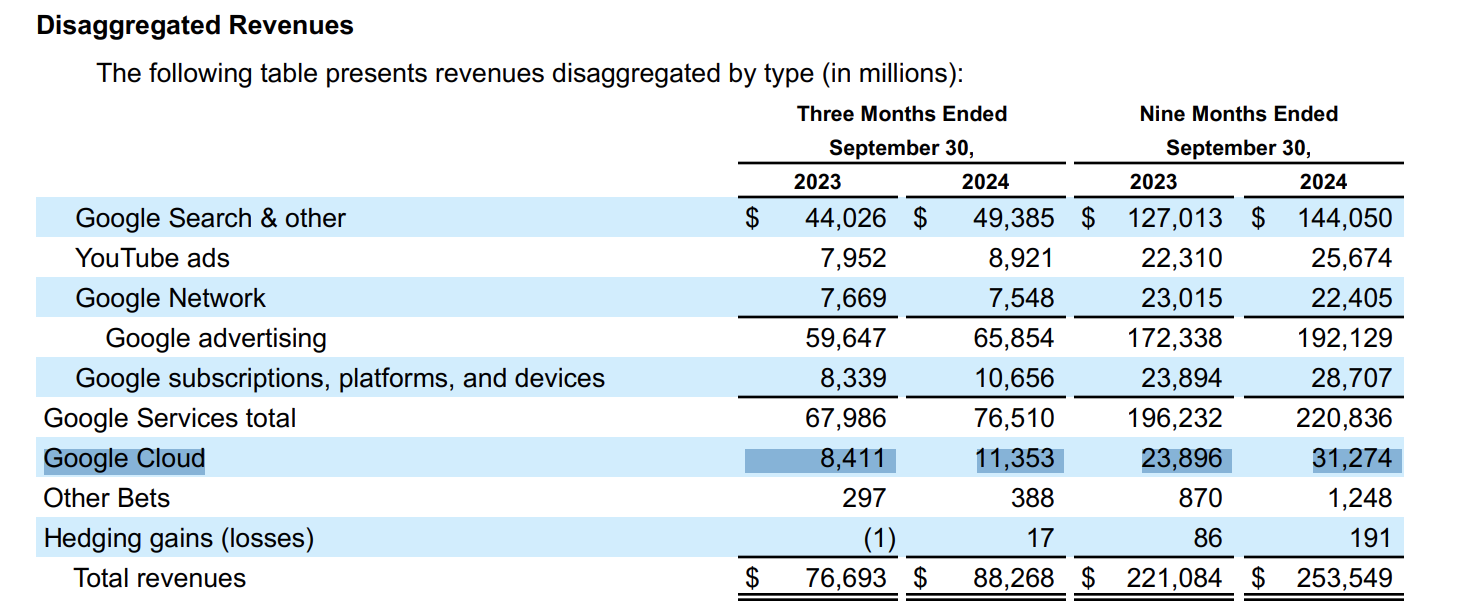

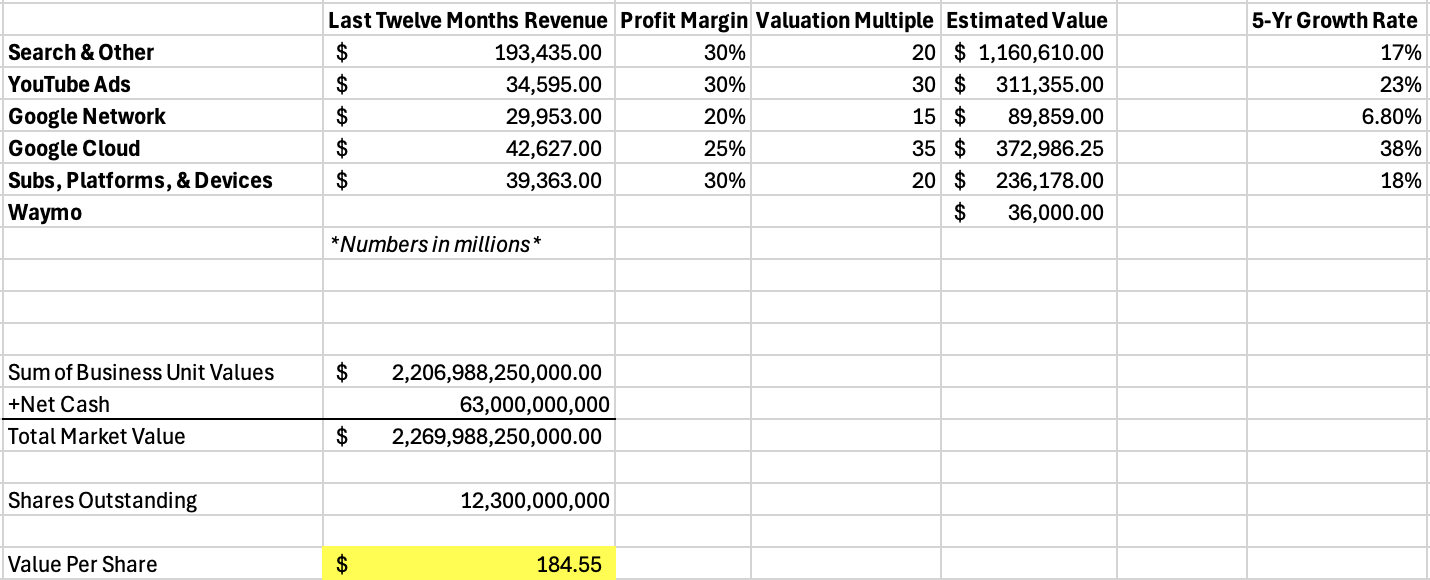

Starting with Google Search & Other, this is a business unit that, in the 12 months leading up to the end of Q3 2024, earned $193 billion ($49b + $144b.) This unit primarily refers to the advertising dollars earned from Google Search, as well as revenues tied to services like Google Maps.

To value this business unit, I start with the revenues above and multiply them by a profit margin. I went with 30%, since this isn’t spelled out explicitly but is in line with the company’s overall profit margin averaged across all business units.

This gives me about $58 billion in profit over the last year, and to estimate the total value of the Search business, I’d want to use a “multiple.” A multiple is the number you multiply current profits by to estimate the total value of a business, and correspondingly, there’s a lot baked into that single number. A multiple isn’t something to be taken lightly, as it will materially impact your understanding of a company’s valuation.

In general, the higher quality (more recurring & stable) a business is or, the faster growing it is, the higher the multiple you’d want to use, whereas, with slower growing or lower quality businesses, you’d want to use a lower multiple. Here’s a short article I wrote to help you better understand multiples and how to use them.

A multiple communicates investors’ required return, baking in assumptions about ongoing profitability and growth. Whenever you look at a price-to-earnings ratio, think of it through that lens.

Going back to Alphabet’s search business, using a multiple of 20 values the unit at $1.16 trillion (20 * $58 billion.)

20 is arbitrary in a sense — maybe you prefer to use 18 or 22 — but it communicates that an owner of Google Search as an isolated business paying 20x earnings would be earning a 5% return ($58 billion / $1.16 trillion.) That’s not too much more than what Treasury bonds pay, and given the extra risks of owning a stock, you’d want a higher return on your capital.

However, Google Search revenues have grown at an average of 17% per year in the last five years, so this unit is still growing at a decent clip, meaning you’ll likely earn more than 5% in future years.

Thus, you’re accepting a 5% return on your investment today with a multiple of 20, but you’re also paying a modest premium now for some of that desirable future growth. If you think Google Search revenues can grow even faster than they have in the recent past, you might value this unit at a multiple of 30x earnings.

A price-to-earnings ratio of 20 feels approximately right for the Google Search business, as this is not far from the P/E ratio that the whole company trades at, and I’d rather be approximately right than precisely wrong. To round up slightly, I get a $1.2 trillion estimated valuation of Google Search & Other.

YouTube Ads

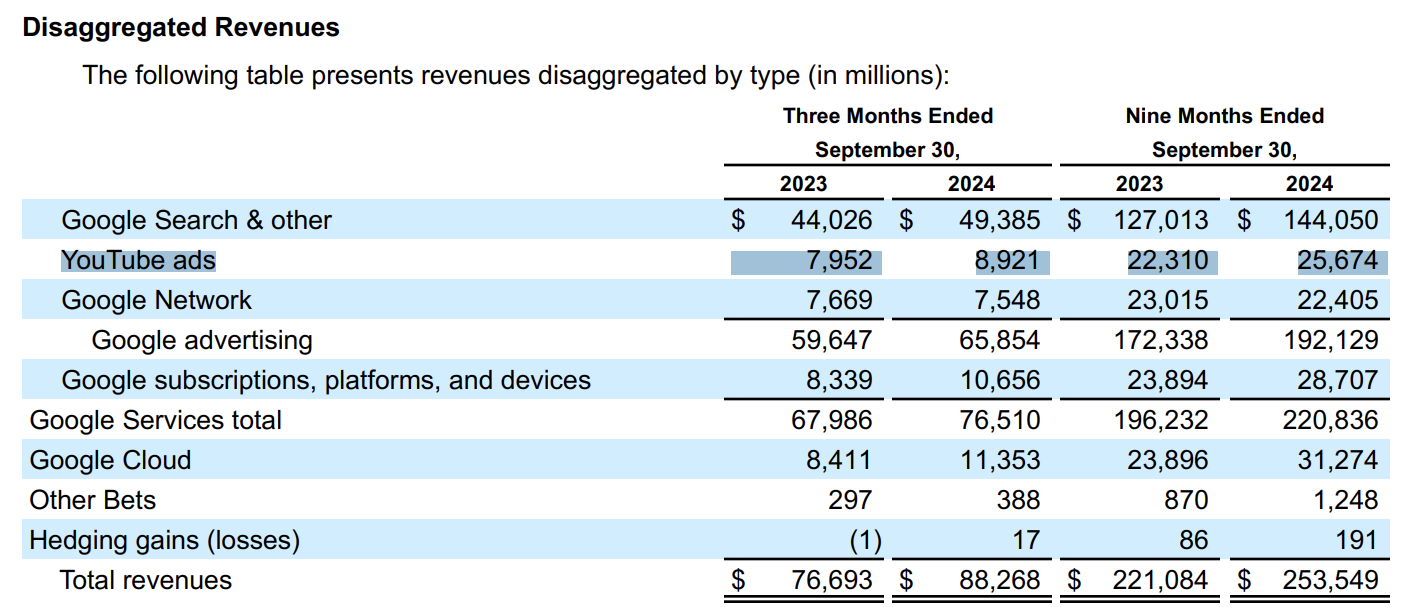

Let’s repeat the process again with the next business unit: YouTube ads. This includes only revenues from advertising, as YouTube Premium and YouTube TV subscriptions are accounted for in the Google Subscriptions, Platforms, and Devices unit, which we’ll get to in a moment.

In the last 12 months, this unit has generated about $35 billion in revenue, and I’ll assume that the profit margins on YouTube advertising are approximately similar to that of Google Search at 30%. Given that YouTube’s ad revenues have been growing at more than 20% per year, and I tend to be quite optimistic about how the service can continue to grow as a loyal user of YouTube myself, I’m comfortable with using a higher multiple of 30 to value this unit at $300 billion.

Summing up the parts, we are now at $1.5 trillion in total value, including my estimate of Google Search’s value.

Valuing A Slowing Business: Google Network

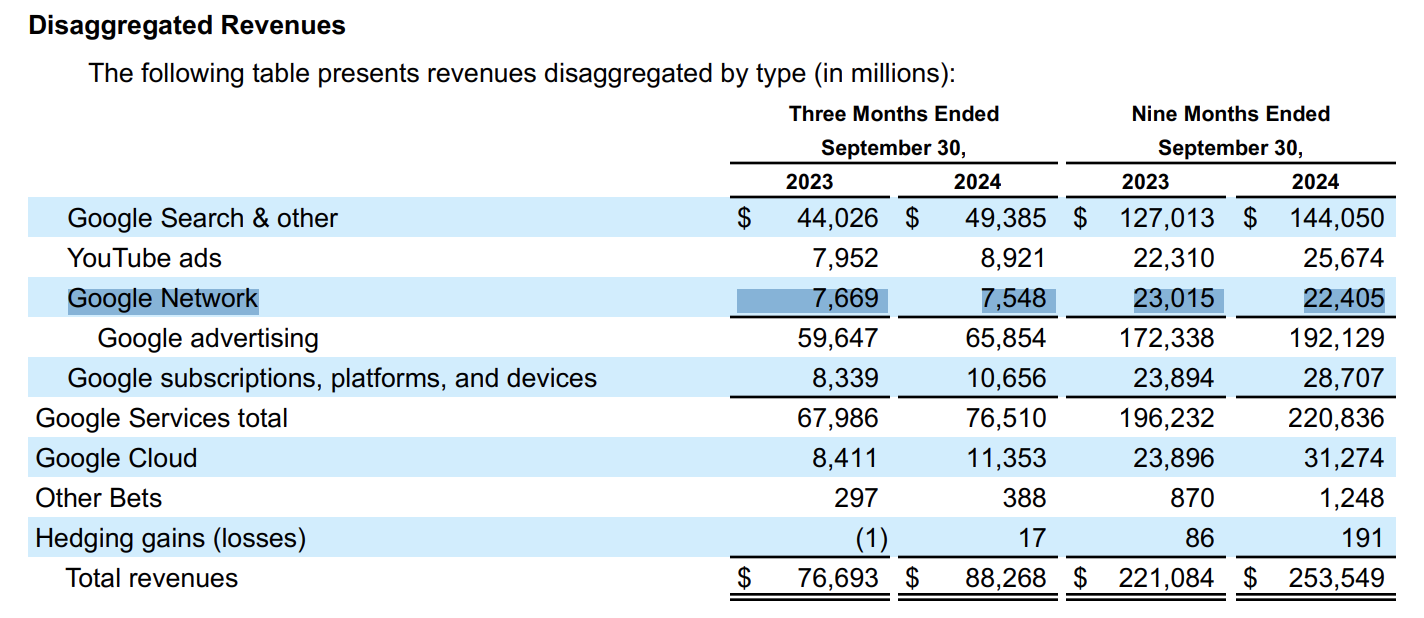

Unlike the fast growth we’ve seen in YouTube ads and Google Search, there is one unit that has been slowing and even declining at Alphabet: Google Network.

Google Network primarily refers to AdSense, which I mentioned earlier — the advertising exchange that allows publishers to run banner ads. This business is stagnating because people just don’t visit as many websites as they used to.

Most of us have a few ecosystems we live in primarily, including Facebook, X, Reddit, Instagram, and TikTok. Whereas we used to venture out to different websites for recipes, travel blogs, and restaurant recommendations, now we do so in these other ecosystems, driving less traffic to individual websites and reducing the advertising dollars that publishers can earn and fees that Alphabet can collect.

Google Network’s revenues actually declined slightly from the year before:

We also know that this is Alphabet’s least profitable unit, so I want to use much more conservative valuation assumptions. With about $30 billion of revenue, I assume only a 20% profit margin and use a smaller multiple of 15 on those profits to value this unit at about $90 billion.

Non-Advertising Businesses

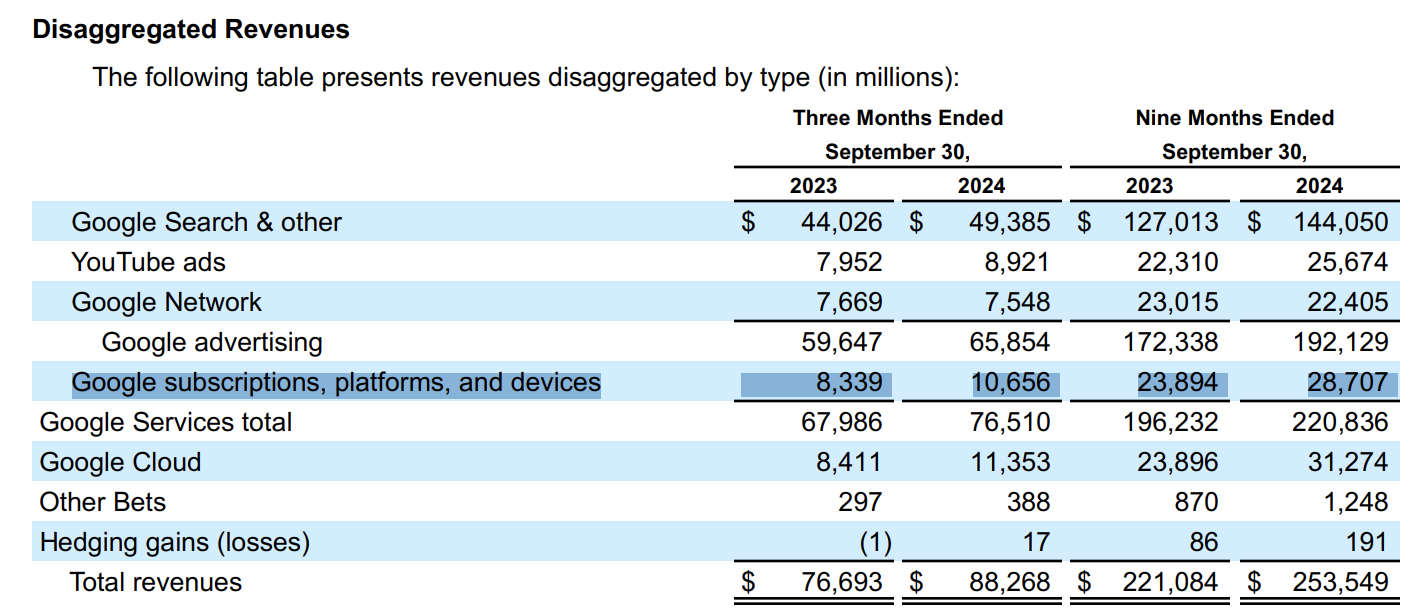

Turning to Google’s Subscription, Platforms, and Devices unit, which includes YouTube TV & Premium, Google Play, Pixel devices, and more, this is a unit generating over $39 billion in revenue.

This unit has grown as fast as Google Search, and without a ton of data on how much this unit earns off a pretty diverse subset of operations, all I can really do is assume its profit margins are roughly in line with the company’s broader average of 30%.

Using a multiple of 20, this values it at more than $230 billion.

The Cloud

And then there’s Google Cloud, the fastest-growing unit at Alphabet, rising nearly 40% per year in the last five years. Using Amazon Web Services’s profit margins as a peer comparison that Alphabet will probably attain once they’re investing less aggressively in growth, Google Cloud should have profit margins of around 25%.

Since this unit is growing so fast, I’m happy to use a more aggressive multiple of 35 to approximately value the business at about $400 billion.

All Together Now

Now, we’ve valued all of Alphabet’s core businesses, and all that’s left is the “Moonshot Bets” I mentioned earlier. These businesses are mostly money losers, but that doesn’t mean they’re without value. I just don’t know how to value them since there’s no real financial information about them.

To write them off, though, would be to write off the value of Waymo and the promise of similar breakthroughs.

Waymo has been through venture capital rounds that value it at about $45 billion (~$36 billion reflecting Alphabet’s stake), so we have a decent estimate of Waymo, but again, not for some of those other businesses. Rather than zero in on them too much, I’d prefer to account for those values by being slightly more aggressive elsewhere in my valuations of Alphabet’s core businesses.

I know Alphabet is an innovative company, and their Moonshot Bets help me justify using higher multiples to value their other units like Search and Cloud.

All that’s left, then, is to add in Alphabet’s cash, net of the company’s debts, and divide that number by the shares outstanding to get an estimate of Alphabet’s intrinsic value per share. See here:

I can easily justify a fair value of $2.3 trillion for Alphabet, or about $185 per share. Looking at today’s share prices, the company is roughly fairly valued, if not slightly overpriced.

Portfolio Decision

If the stock is fairly valued, you might think the answer here is that I don’t plan to add Alphabet to The Intrinsic Value Portfolio. And the answer is yes and no. Unlike other companies I’ve broken down, like Coupang and John Deere, where I estimated their value but felt they were well beyond my circle of competence, I feel differently with Alphabet.

Don’t get me wrong, Alphabet’s technology is well beyond my realm of understanding, too, but I relate to Alphabet in a different way. I grew up using Google Search, Google Maps, Gmail, and so many of their services that I have an intuitive appreciation for what they do.

After having dug more deeply into the company’s financials, I’m not only blown away by the massive amounts of profits they generate but also how they keep finding ways to grow their existing businesses.

They produce so much cash flow to allocate toward building powerful technologies, repurchasing stock, or paying dividends, with such strong brand recognition and trust that it’s a company I don’t want to miss out on owning any longer.

Between the company’s large-language model Gemini, which we haven’t even had time to cover, and its massive repurchases of stock (decreasing the total share count by 2-3% per year), I’ve never seen so many levers that can be pulled to create value for shareholders in a single stock.

I’m not racing into the stock at current prices, but over the next year, any chances I have to buy the stock at a modest discount to my estimate of intrinsic value ($180 or less, or even better, $170 or less), I plan to fully capitalize on them.

Alphabet is the definition of quality, and I want to store my wealth in the highest-quality assets.

There’s been a lot of bluster about ChatGP, regulation, and, more recently, about breakthroughs in Chinese AI tech – all that has played into keeping the stock more modestly valued. I want to use any corrections related to these kinds of headlines as a chance to build a position in the company, so we’ll see if that opportunity comes.

For now, I don’t expect to build more than a 3-5% stake in the Portfolio with Alphabet, but the further it drifts from intrinsic value, the bigger the bet I’ll take on it.

Disagree with my thinking? Listen to my full podcast here first, because I’ve run out of space to say everything I’d like to in this newsletter. In the podcast, I further outline the risks and the case for Alphabet in more detail. And then please leave your feedback in the poll at the bottom of this newsletter or hit reply to this email.

To see my numbers or use your own assumptions, feel free to play around with my valuation model for Alphabet here.

Weekly Update: The Intrinsic Value Portfolio

Alphabet additions pending

Notes

Just one holding in the portfolio so far: Ulta, but I plan to scale into Alphabet over time, buying when the stock is below $170-$180.

Over time, the Alphabet additions will be reflected, assuming there are

chances to opportunistically buy in below intrinsic value. I will keep you updated as I go along with this

Quote of the Day

"The biggest risk is not taking any risk…In a world that’s changing really quickly, the only strategy that is guaranteed to fail is not taking risks.”

— Mark Zuckerberg

What Else I’m Into

📺 WATCH: How China’s AI breakthrough is threatening U.S. tech companies

🎧 LISTEN: The Scuttlebutt Edge — from research to returns

📖 READ: Cullen Roche’s debunking of the biggest myths in investing

Your Thoughts

Here’s what readers had to say about John Deere last week:

“Their ROIC (11%), Magic Formula (7%), and CROIC (5%) are not strong, while ROE appears solid (31%). FCF and Owners’ Earnings are basically flat over 5 years with adding $10B in debt and similarly in CapEx increases. Similar conclusion: too much to figure out, isn't straightforward, and real questions in many areas. Wait for that fat & obvious pitch! In that general industry area, Tractor Supply Co is a bit more interesting, but I haven't pulled the trigger yet there either.”

“They have a monopoly on repair and parts only available from John Deere. They've been fooling the public for years.”

“For me, it is more of a question of value. This will be a stock I buy during the next downturn.”

See you next time!

Enjoy reading this newsletter? Forward it to a friend.

Was this newsletter forwarded to you? Sign up here.

Use the promo code STOCKS15 at checkout for 15% off our popular course “How To Get Started With Stocks.”

Follow us on Twitter.

Keep an eye on your inbox for our newsletters on Sundays. If you have any feedback for us, simply respond to this email or message [email protected].

What did you think of today's newsletter?

All the best,

© The Investor's Podcast Network content is for educational purposes only. The calculators, videos, recommendations, and general investment ideas are not to be actioned with real money. Contact a professional and certified financial advisor before making any financial decisions. No one at The Investor's Podcast Network are professional money managers or financial advisors. The Investor’s Podcast Network and parent companies that own The Investor’s Podcast Network are not responsible for financial decisions made from using the materials provided in this email or on the website.