I’ve got a fun one for ya today, folks: Silicon Valley meets hospitality, the hotel industry’s worst nightmare — Airbnb 🏡

If you contributed to any of the nearly 500 million nights booked on Airbnb in 2024, you’ll know the platform well. Airbnb is a pillar of the “sharing economy” and has changed the world enough to have its name become an all-encapsulating word like Google or Kleenex.

Uber convinced the world to ride in strangers’ cars, and Airbnb convinced them to sleep in strangers’ homes, and that has been worth tens of billions of dollars ($80 billion, actually, looking at Airbnb’s market cap.)

A few pillars of the thesis for Airbnb: The company has the potential to penetrate more deeply into countries around the world, it’ll continue to enjoy economies of scale as the business grows, it can further expand its margins with advertising (sponsored listings from hosts), all the while continuing to earn a ton of interest — $800 million in the last 12 months — from the pile of cash it both owns and holds on behalf of hosts from customer pre-payments for bookings (aka “float.”)

Without further ado, here’s the story of Airbnb, its business model, valuation, and my decision on whether to add it to The Intrinsic Value Portfolio.

(And at the bottom of this newsletter, I share some reflections on the recent turbulence in markets and how it affects the Portfolio.)

— Shawn

Airbnb: The Growth Story Isn’t Over Yet

The Story of Airbnb

Airbnb began as “Air Bed & Breakfast,” literally referring to co-founder Brian Chesky’s hope of renting out an extra bedroom with an air mattress to help pay the rent for his San Francisco apartment.

As with many great innovations, Airbnb was born out of necessity: A broke art school grad looking for ways to pay the bills who happened to notice that large influxes of travelers for conferences often overwhelmed local hotels.

Airbnb, then, was envisaged less as a new paradigm in hospitality and more as a practical way to A) help Chesky pay his bills and to B) soak up surplus demand for temporary housing during large events.

The original idea had some kinks. For starters, it wasn’t until later that the early founders realized they didn’t need to require hosts to literally run a bed and breakfast — in the beginning, hosts had to be on the premises and prepare breakfast for guests.

In part, I think that was because, if I can transport you back to 2009, people thought it was absolutely crazy that homeowners, at scale, would let travelers stay in their homes alone and that travelers would want to.

Creating a platform to basically turn any home with an extra bed into a bed and breakfast seemed far more plausible than “Hey, I’m going to leave for the weekend and let this stranger pay me $200 to sleep in my bed,” which now we broadly see as not that weird at all. Times change.

But there was a network effect problem. No one wants to list their home on a site with no guests, and no guests want to visit a site with no listings.

At the same time, just about anyone Chesky pitched Airbnb to thought the idea was terrible. Yet, he continued to hustle, personally taking professional pictures of properties to improve listing quality and even selling “limited edition” election-themed cereal boxes for $40 a pop to raise funding for the company.

The 2008 cereal boxes Airbnb’s founders sold to raise money

It wasn’t until Airbnb caught a lucky break with Y Combinator after impressing venture capitalist Paul Graham that the company finally began gaining momentum and later received an investment from Sequoia Capital.

To be clear, though, it wasn’t that Graham liked the idea — he also thought Airbnb was a lousy idea, but he admired the work ethic and will to succeed of Airbnb’s early founders (I focus on Brian Chesky since he’s still the CEO but this also includes Joe Gebbia and Nathan Blecharczyk.)

With some savvy programming, Airbnb was able to tap into cross-posting on Craigslist, solving its early network effect problem by tapping into listings there, and with some money in the bank, it could finally grow seriously.

Airbnb’s CEO and co-founder Brian Chesky

And, as mentioned, Brian Chesky is still running the company to this day while not taking a salary and promising to donate most of his wealth to charity. He’s an impressive guy, not your typical Silicon Valley boy genius with a mastery of computer programming. Instead, given his design background, he’s more often compared with Steve Jobs — a visionary who has the courage to change the world.

The Business

It’s fun to talk about origin stories and world-changing founders, but let’s look at the actual business.

Airbnb is an online booking platform for short- and long-term rentals and “experiences,” such as wine tastings, hot air balloon rides, jet skiing lessons, and other unique activities that pair with certain listings.

Typically, Airbnb takes a fee from both hosts and guests as a percentage of the Gross Booking Value, aka GBV (referring to the total amount paid for a trip.)

For most hosts, the fee is about 3% of GBV, whereas guests pay a roughly 12% service fee, but some hosts opt to pay both sets of fees entirely themselves, reducing the costs for guests and making their listings more competitive. Either way, if a booking is made for $100 a night, Airbnb collects $14-15 in fees.

Airbnb takes its cut for enabling bookings, providing customer service, processing payments, etc., and hosts have the ability to tack on optional fees related to cleaning, down payments, and late cancellations in addition to Airbnb’s service charges.

Sample of charges for an Airbnb

Some hosts have notoriously abused this, stacking up fees and a laundry list of to-do lists for guests to complete before leaving, which has stained Airbnb’s reputation.

I’m sure many readers have experienced this, and some have probably swarn off Airbnb for this exact reason. In contrast, hotels offer far more consistent experiences. For the most part, when you book a hotel, you know exactly what you’re going to get, from standardized room accommodations to room service, a concierge desk, free breakfast and free wifi, and almost no risk of the hotel canceling on you last minute (as Airbnb hosts periodically do to guests.)

Airbnb’s Value

Why would anyone ever book an Airbnb then? While some would have you believe Airbnb is a terrible product compared to hotels, the reality is that it’s not an apples-to-apples comparison.

Yes, business travelers will continue to rely on the consistent service of hotels, their convention centers, and their proximity to airports or downtown areas. Leisure travelers, however, have discovered that they can get much more out of trips than staying in a stuffy hotel room with a cheap breakfast in the commercial area of a city, separating you from being integrated with the city or community they’re visiting.

Airbnbs can be anywhere in the world, allowing travelers to stay in places that were otherwise inaccessible. A cabin in the woods overlooking the Rocky Mountains? No problem. A villa in a medieval town in the south of France? Not an issue. A literal recreation of the house from the Pixar movie Up (equipped with 8,000 balloons)? Sure, why not.

Practically speaking, Airbnb helps cities absorb excess tourism that hotels can’t accommodate, as happened with the 2024 Paris Olympics, where the French government worked with Airbnb to drive hundreds of thousands of people to stay in Airbnbs during the games.

More compelling, though, is the chance to feel like a part of the place you’re visiting by, for example, staying in someone’s real house in a quiet neighborhood with a garden and a rooftop that looks out on the city, rather than being in a hotel in the most commercialized area of the city.

Brian Chesky realized this early, and his mission for Airbnb for years now has been to ensure “belonging.” Whether that’s with a host leaving freshly made cookies for guests, being welcomed with a warm note, and otherwise feeling comfortable in someone else’s home, the focus has been on making guests feel like they belong, not like they’re generic tourists transactionally checking in and out of a hotel.

Airbnbs also excel in rural and remote areas, where there isn’t enough population density to support hotels (even though these may be some of the best places to visit!) and with large groups — having all your friends stay in the same house for a bachelor or bachelorette party is far more preferable and affordable than 12 different hotel rooms. Same for family vacations.

Can Airbnb Continue to Grow?

The short answer is yes, with some wrinkles depending on how optimistic you are.

While Airbnb operates in 220 countries, it has only deeply penetrated 5: The U.S., Canada, Australia, the U.K., and France. Penetrating more deeply into places like Japan, Brazil, and Germany is easier said than done, given local competitors and regulations, but deeper penetration in these places is plausible and also potentially worth billions of dollars.

On top of this, Airbnb has other ways to grow earnings. As Airbnb has grown, marketing, R&D, and other overhead expenses have made up a smaller and smaller share of revenue, and correspondingly, the company converts a growing chunk of revenue into profits and likely has more room to benefit from this (potentially expanding operating margins from 15% to 20% or even 25% by some estimates.)

They can also boost profitability and revenue by expanding into advertising, similar to how Amazon has built a massive advertising business by allowing brands to promote their products higher up in search results. Artists on Spotify have done something comparable, agreeing to promote their music to a wider audience through Spotify’s algorithm in exchange for lower royalty rates.

Airbnb’s competitors, Expedia and Booking.com, already rely on this hugely, though their sponsored listings are primarily from hotels, which are more formidable advertising partners.

Airbnb’s challenge is that it works with a more decentralized network of less well-capitalized hosts operating on slimmer margins, but still, Brian Chesky has called it a massive opportunity for the company to offer sponsored listings, and I think it will come at some point in the next few years.

Hosts might agree to pay higher service fees to Airbnb in exchange for promotions that help them increase their occupancy rates, and if occupancy rates rise enough, the economics could certainly workout, depending on what the fees are.

This could conservatively be worth a few hundred million dollars (with very little variable costs, adding directly to profit margins) or much more over time.

Airbnb is also focused on attracting more hosts who oversee luxury listings since they command much higher gross booking values, translating to bigger payouts for Airbnb with each booking.

And, last but not least, one of the most overlooked factors supporting Airbnb’s business is the float from the cash it holds from customer prepayments. Basically, Airbnb enjoys negative working capital from getting paid upfront by guests, but it doesn’t have to pay hosts until two days after the initial booking date. As a result, Airbnb has held an average cash balance of $6.5 billion on behalf of hosts over the last 12 months, which, by my estimate, has generated roughly $300 million in extra cashflow that they get to keep.

Airbnb earns interest on billions of dollars held on behalf of customers

It’s a similar dynamic in insurance and part of Warren Buffett’s success with Berkshire, investing premiums and capturing that income before having to later pay insurance claims.

For context, those earnings from float are worth around a fourth to a third of the company’s operating profits, so they’re a substantial addition to free cash flow that can be used for reinvestment, dividends, or share repurchases. And as Airbnb’s business grows, so will the value of its gross bookings, which means this float will only increase over time and compound, adding more and more incremental interest income.

The one stipulation being that interest rates must remain where they are or higher. Otherwise, falling interest rates would offset any float expansion, and if interest rates fall to zero again, they’ll effectively lose this income source entirely. So, it’s not something I rely on heavily when valuing the business, but it does help to provide a margin of safety and enable me to be a bit more aggressive with my assumptions elsewhere (i.e., revenue growth rates, profitability improvements.)

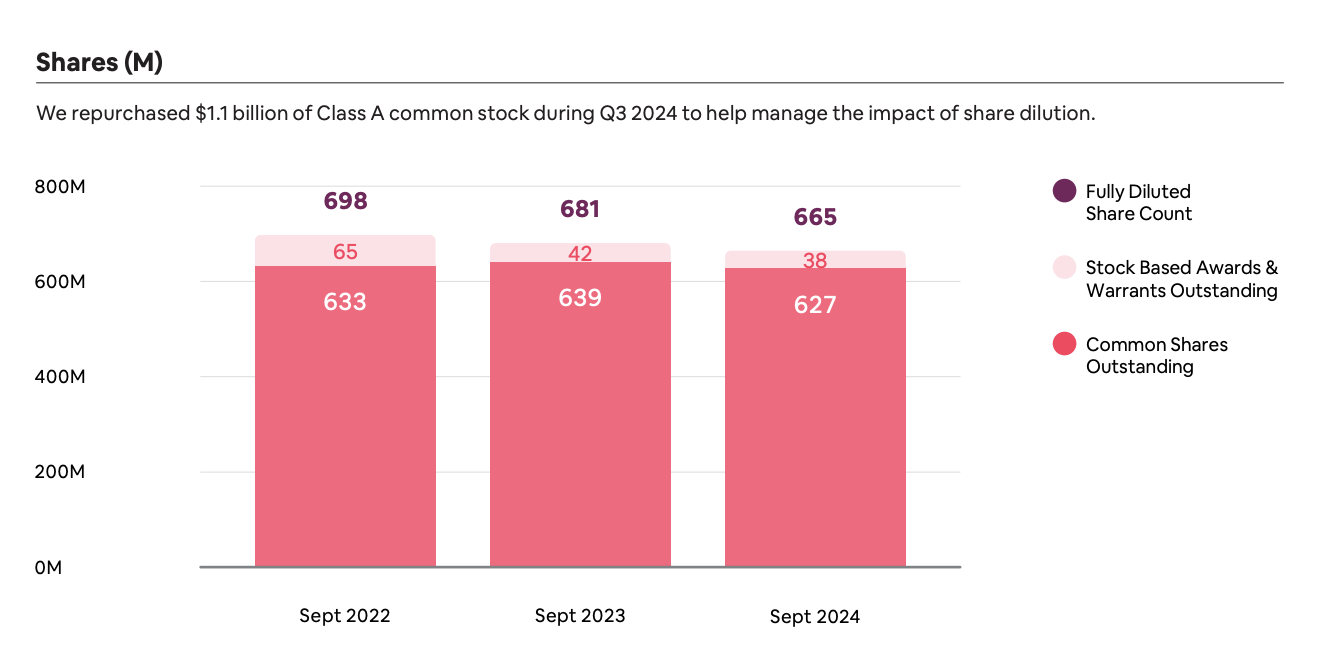

Between the float described here and the company’s $11 billion+ stockpile of its own cash (net cash of $9 billion after stripping out debt), Airbnb remains extremely well capitalized and comfortably positioned to aggressively repurchase stock. Since 2022, Airbnb has spent billions of dollars on repurchases — sometimes as much as their entire annual free cash flow.

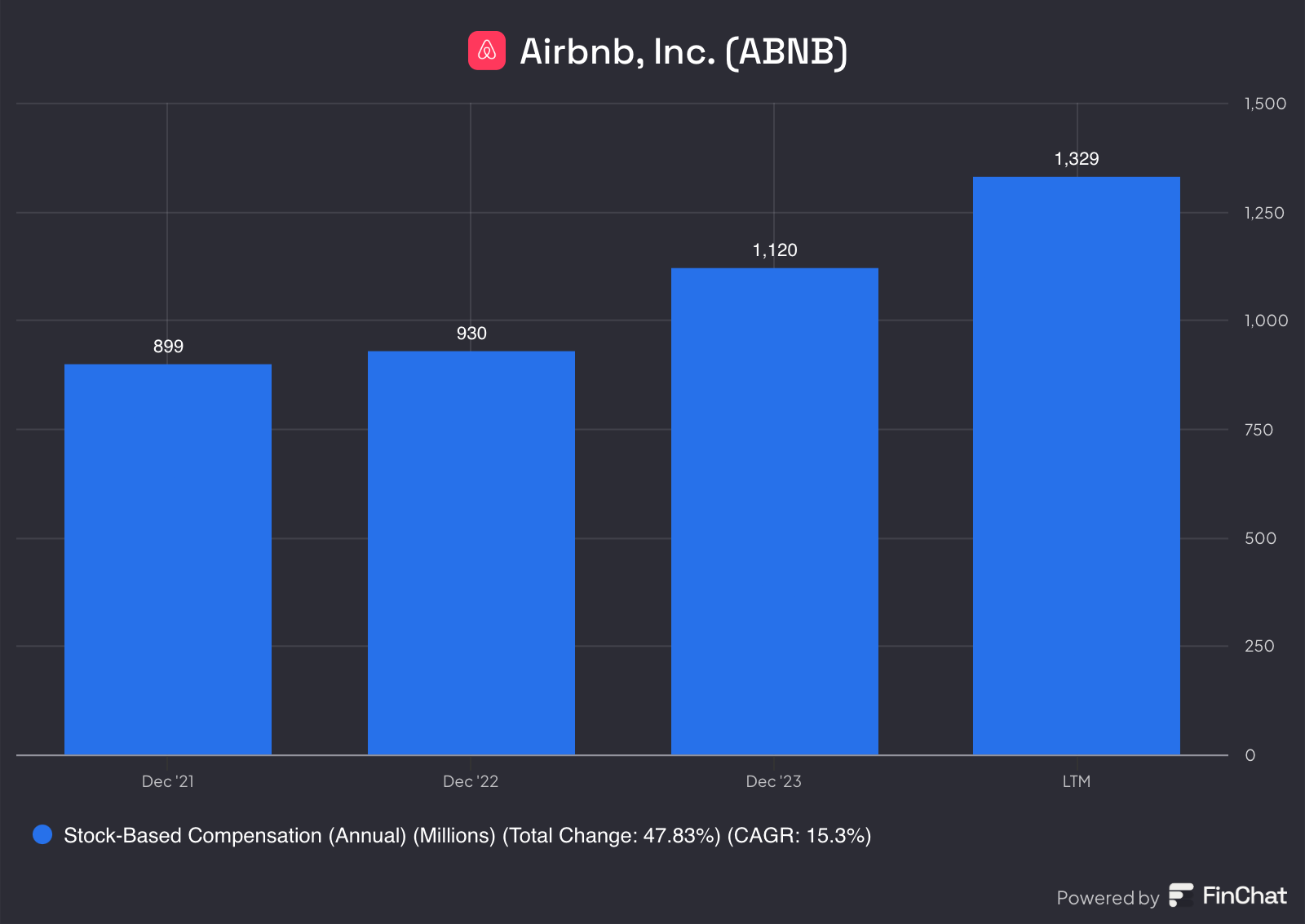

You will notice, however, that Airbnb’s share count hasn’t really declined at all in recent years, bringing us to the elephant in the room: Airbnb, like many Silicon Valley companies, has been stupendously aggressive about using stock-based compensation.

That expensive and dilutive share issuance hasn’t done existing shareholders any favors, though much of it is tied to restricted stock units (RSUs) from the company’s 2020 IPO that have vested over the last four years. In other words, Airbnb gave employees massive stock grants that they couldn’t access for years down the road, and as those shares have been granted over time, Airbnb has had to recognize those costs and has seen its share count grow.

You might recall that I passed on Vital Farms for this exact reason. But with Airbnb, the picture is different because Airbnb is a much more robust and profitable company with better prospects for growth, has a sizable repurchase program to offset this dilution, and, most importantly, has signaled that stock-based compensation will wain this year now that IPO-related RSUs should mostly be fully vested.

As a result, stock-based comp isn’t expected to grow faster than employee headcount going forward, and with the same amounts or more going toward repurchases, the share count should decline in the coming years (increasing shareholders’ slice of the pie.)

More Downsides to Consider

Okay, so declining interest rates and stock-based comp concerns aren’t the only things to consider here.

As mentioned, a number of folks despise Airbnb for what they see as hidden fees and chores from hosts, and communities at large have complained that Airbnb is immensely disruptive. What contributes to a sense of belonging for guests, by staying in an intimate neighborhood, is a hassle for locals — who wants to live next to an Airbnb and have different neighbors every week?

Others claim short-term rentals come at the expense of longer-term rentals and homeownership, driving up rates for regular renters and creating a shortfall of housing as properties are instead used to accommodate tourists.

Cities worldwide have responded with a range of crackdowns, requiring hosts to register their properties and limiting the number of short-term rentals a single landlord can have, restricting how many guests can stay in a short-term rental, and even outright banning short-term rentals, as Barcelona plans to do by 2029.

New York’s crackdown last fall has seen an 80% decline in Airbnb listings in the city, something Airbnb is pouring millions of dollars into fighting to reverse.

Fortunately, no single city makes up more than 2% of the company’s revenues, so it doesn’t have a single point of vulnerability, and there’s a pretty wide spectrum globally for how cities view Airbnb. For some places, it’s seen as a nuisance and maybe even a cause of permanent housing shortages, while others see it as a lynchpin of their tourism industries and an important source of tax revenues.

The regulatory picture, for the most part, isn’t one I’m overly concerned with, as millions of people love the service, limiting how harsh governments want to be in regulating Airbnb. Additionally, Airbnb has so much room for growth it’ll be a while before specific cities’ regulations are consequential.

What does concern me, though, is consumers’ trust in Airbnb. Unique experiences contribute to Airbnb’s value, but there are limits to this. Airbnb still must be reliable. As in, nobody wants to book a trip to find a property that doesn’t live up to expectations or, worse, have a host cancel on you late, leaving you to scrape together alternative accommodations at the last minute (an all too frequent issue.)

Airbnb’s unique set of listings

For what it’s worth, Airbnb has delisted over 300,000 low-quality properties in the last year, reducing some of these issues while also promoting “Superhosts” in the algorithm, driving more bookings to high-quality hosts who are less likely to cancel on guests.

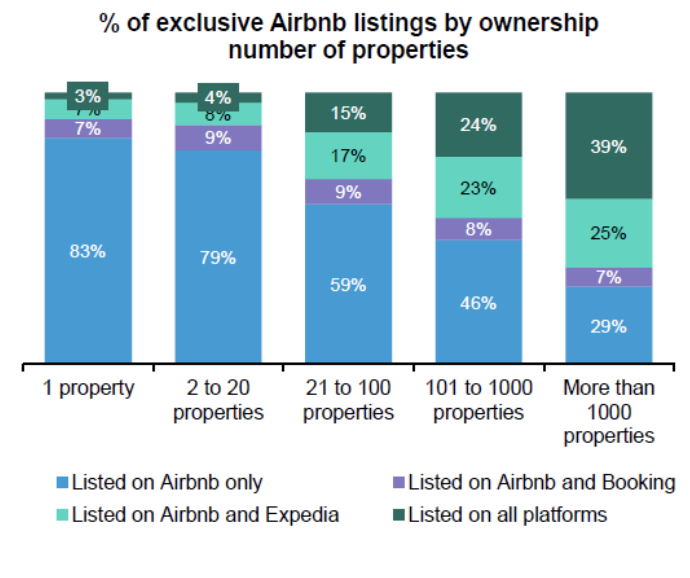

On the supply side, Airbnb needs to ensure that hosts want to continue listing their properties on Airbnb and, preferably, exclusively so. In theory, nothing is stopping hosts from listing their properties on VRBO, Booking.com, or other sites, yet most Airbnb hosts with five properties or fewer remain strictly loyal to exclusively listing on Airbnb — larger, more professional property owners have fewer qualms about listing elsewhere, though. Perhaps smaller part-time hosts, out of complacency or simplicity, choose to list exclusively on Airbnb; whatever the reason is, the trend is clear.

Airbnb may need to eventually reward hosts for being loyal at the expense of its own revenues and profit margins. The more that unique Airbnb listings are available on other sites or available for direct booking, the more Airbnb’s inventory becomes a commodity, also eating into its business. And I’d hate to see a race to the bottom where Airbnb has to slash service fees to undercut competitors and attract more hosts or unique listings.

This seems like the weakest part of their moat to me, which I’m trying to understand better: What’s keeping Airbnb hosts from cross-listing on other booking sites?

From what I can tell, Airbnb helps hosts out a lot, from providing the booking traffic to customer service, pricing data, and offering algorithmic pricing that automatically adjusts a listing’s rates based on demand in the area.

Yet, that still doesn’t explain why hosts exclusively use Airbnb. This could relate to that, from what I’ve seen, VRBO’s host fees can be more than twice as high as Airbnb’s, making it less profitable to get a booking from VRBO if you could have otherwise gotten it through Airbnb. Same for Booking.com, which actually charges 5x higher host fees than Airbnb for hosts, so again, Airbnb seems to be more economical for hosts (Airbnb shifts these costs primarily onto customers.)

I’ve also heard that Airbnb has superior customer service, a simpler yet more powerful interface for hosts, and better insurance coverage for things like property damage, which could all contribute to why Airbnb remains the preferred listing platform.

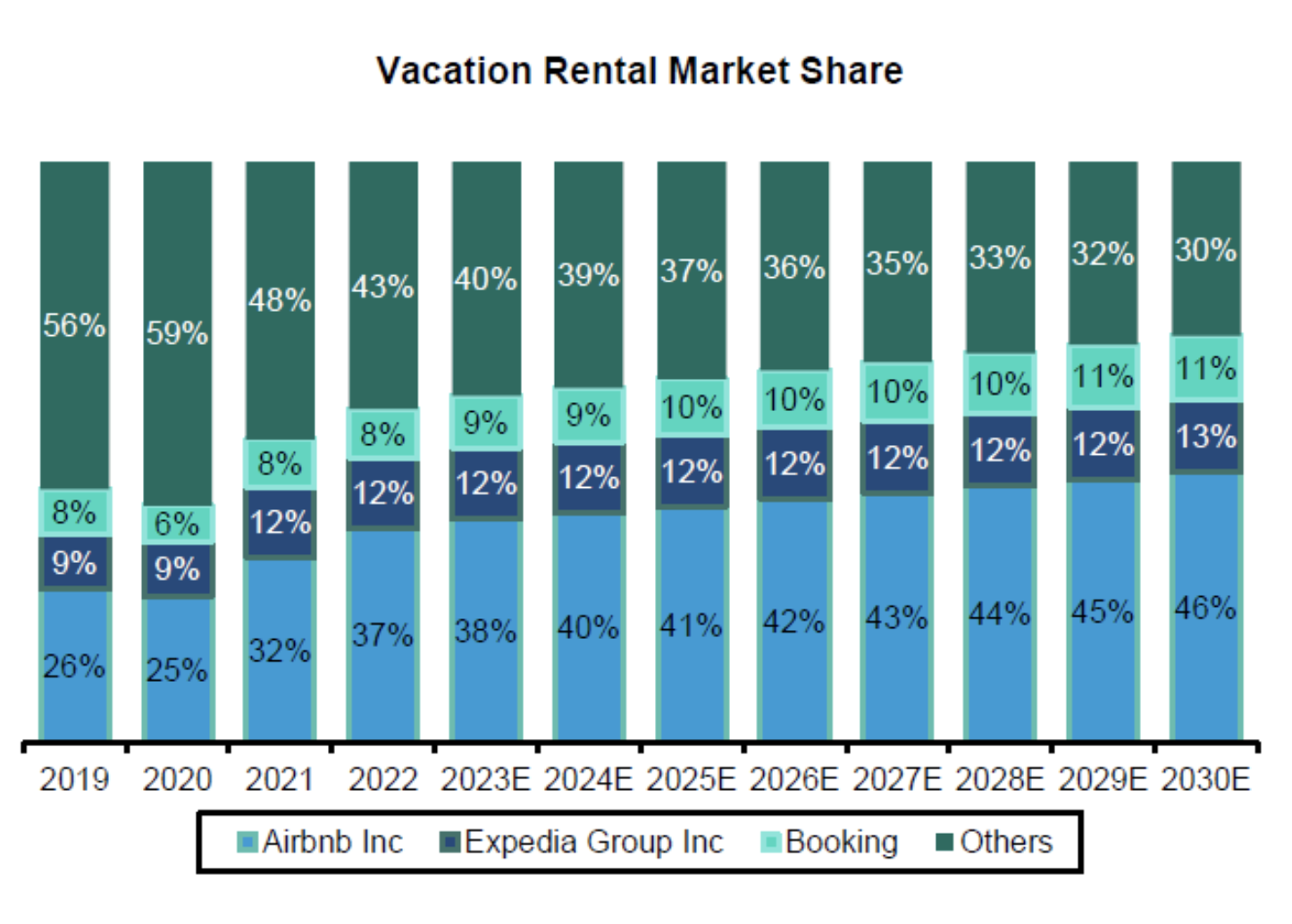

While I don’t have a perfect explanation for Airbnb’s advantages here, the data continues to paint a favorable picture for Airbnb as its market share expands, suggesting there’s some sort of hidden moat and stickiness for its service (for both hosts and guests.)

Airbnb’s market share is growing and expected to continue growing

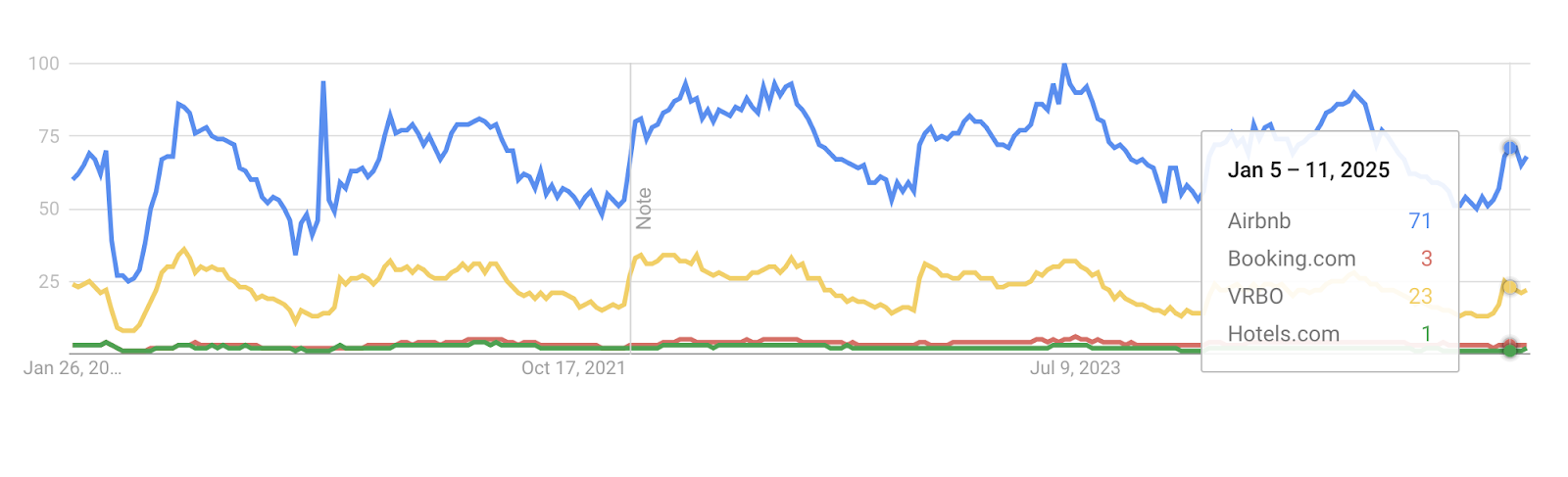

Relatedly, Airbnb’s network effects and brand recognition are by far the strongest of its peers (and are also real sources of moats). For example, the company relies far less on sponsored ads to drive traffic to its website and earns a much higher share of web traffic from people directly searching for Airbnb by name.

Google Trends shows Airbnb’s dominance

Valuation

We’re beginning to run a bit long here, so I will keep this short and sweet. For more, you can always listen to my podcast on Airbnb. You can also download and play around with my model for yourself here.

You will see two valuation approaches in the model based on price-to-free-cash-flow and enterprise value-to-EBIT (earnings before interest and taxes, a measure of operating profits.)

I’ll focus on the latter for brevity. My assumptions will align with what you’ve read already, but here they are again:

Stock-based compensation will slow dramatically in line with employee headcount growth (but not decline, though that would be great.) The company will also continue to spend billions on share buybacks, with enough firepower to even scale this up further

Operating margins will rise, thanks to economies of scale, from 15% to over 20% within five years

Airbnb will grow gross booking value in its core markets (U.S., U.K., Australia, Canada, France) and will grow faster in other markets, boosting revenues and float

Airbnb will earn even higher fees, supporting profit margins, from unveiling sponsored listings within the next five years

Sounds good, right? My model projects out operating profits per share over the next five years and then, importantly and arbitrarily, relies on a range of exit multiples (the valuation the stock will have when selling out five years from now.)

Shawn’s model of operating profits

To reduce the arbitrariness, I calculated a range of current values for the stock, depending on the EV/EBIT exit multiple in 2029. Today, the stock trades at an enterprise value of 45x operating profits, and this will decline as the business matures. Between 20 and 25 is fairly normal for a high-quality business, and so my range varies from 16x EV/EBIT to as much as 34x (assuming the company is still growing quickly in five years), with the most weight on values in the low-to-mid 20s.

Stock price target: $150

My weighted average value for the stock, given a range of possible valuation multiples reflecting the company’s prospects looking forward in 2029, comes out to $150 per share, a modest premium to the current share price.

Portfolio Decision

So what’s the final word?

With a little hesitation, I’m adding Airbnb to the portfolio. I’m biased, but as a customer, I love Airbnb. I have never had a bad experience, and I have, in fact, had experiences I would never have otherwise imagined in a world of hospitality dominated solely by hotel chains. They say to buy what you know, and to an extent, that’s what I’m doing (after validating my customer perspective with research on its fundamentals and valuation.)

I see a business with a ton of levers to pull to fuel growth, from advertising to deeper penetration of existing markets to offering more paid experiences with booking (something we’ve run out of time to discuss in more detail) and increasing the percentage of luxury bookings.

Whenever you oversee a network as beloved and powerful as Airbnb’s, I think that creates a ton of optionality for the business, and with the stock well below its IPO price and declining nearly 10% in 2024, I don’t think its valuation is eye-popping nor are investors excessively optimistic about its prospects.

I suspect the business can continue to grow at double-digit rates while using its massive cash balance to reduce the share count, which is a very attractive formula for me.

At current prices, there seems to be a modest margin of safety, with a ton of potential upside if the business can grow like I think it can.

Airbnb will add a growth element to our portfolio, and I’m excited about that, but I’m not without concern. If stock-based compensation or share repurchases don’t align with my expectations, that would be a significant red flag. And if I see evidence that Airbnb is losing its market share, that its host network is weakening and declining, or that the company has to dramatically reduce fees to remain competitive, I would have to seriously re-evaluate the position.

As such, I don’t have the conviction to make this a more than 10% weighting and will add it to the portfolio with a weighting of between 5-10%.

As always, you can see The Intrinsic Value Portfolio below, some interesting links to read, watch, and listen to, my quote of the day, portfolio construction updates, and readers’ feedback from last week. You can also answer the poll below, leaving your feedback on my decision (which might get highlighted in this newsletter next week!)

Weekly Update: The Intrinsic Value Portfolio

Values shown at cost, total portfolio is down 1.3% since inception this year

Notes: Political Turbulence Weighs On Markets

General Thoughts: Things in markets are moving fast, and the outlook has swung dramatically in just a few weeks. Two months ago, the optimists were firmly in control, betting that strong economic growth and corporate profit growth could continue indefinitely as many viewed the U.S. as the best place to allocate capital. Now, pessimism and fear are taking hold.

Politics aside, picking fights with key trade partners, imposing blanket tariffs, and related measures all inject frictional costs and uncertainties that markets dislike, as they come at a cost to both consumers and companies.

It doesn’t surprise me at all, then, that equity markets have entirely erased their gains since November, especially since U.S. equities have been richly priced — priced to perfection you might say, and current circumstances lend themselves to anything but corporate earnings’ perfection going forward.

Opportunity? I don’t think the pain is over by any means, but selloffs are generally a gift to longer-term investors, especially those with cash on hand to exploit opportunities. Alphabet and Ulta have certainly felt the pain from this shift in market sentiment, as has Airbnb, but we also still have a portfolio that is mostly in cash here with The Intrinsic Value Portfolio, so I’m excited to take advantage of continued sale prices on these wonderful companies.

For what it’s worth, Alphabet’s business shouldn’t be heavily impacted by tariffs, nor should Airbnb’s, so I continue to think that these stocks are compelling, though they’re certainly vulnerable to recession risk should one manifest this year (the Atlanta Fed has dramatically revised growth expectations, suggesting a contraction in Q1.)

With many of its products coming from China, and with beauty spending having a non-trivial component of embedded discretionary spending, Ulta’s business is likely the most vulnerable of the three.

With its stock down around 20% year-to-date and 40% in the last 12 months, I think these concerns are priced into Ulta already, and I continue to view it as a wonderful business to own long-term, even if there may be some more pain in the coming months.

Additions: I’ve gone ahead and added a starter position in Airbnb this past week at an average price for the portfolio of $135.15, amounting to a 4% position, and I will likely scale this up further in the coming weeks.

Quote of the Day

"Maybe you’re right 5 or 6 times out of 10. But if your winners go up 4- or 10- or 20-fold, it makes up for the ones where you lost 50%, 75%, or 100%.”

— Peter Lynch

What Else I’m Into

📺 WATCH: The business strategies behind McDonald’s, Aldi, 7-Eleven, and more

🎧 LISTEN: Richer, Wiser, Happier — Q1 2025, with Stig Brodersen and William Green

📖 READ: Why it’s premature to bet against Google Search; unlocking shareholder value in Japanese balance sheets

Your Thoughts

Do you agree with the portfolio decision for Airbnb?

Here’s what readers had to say about Blue Owl last week:

“Thanks, Shawn. As was said by Charlie Munger, I believe…"If it is too hard when looking at an investment/company, throw it over your shoulder."

“As has often been quoted as being said by Buffet &/or Munger, “don’t buy companies you don’t understand “. No need to go further than that when you get a glimpse of the complicated spider web of a business that Blue Owl is.”

“I agree on this; as you pointed out, I see two big risks. Macro - as public credit through banks increases, private credit requirements will be lower. Second - the risks of not knowing how big the bad assets are.”

See you next time!

Enjoy reading this newsletter? Forward it to a friend.

Was this newsletter forwarded to you? Sign up here.

Use the promo code STOCKS15 at checkout for 15% off our popular course “How To Get Started With Stocks.”

Follow us on Twitter.

Keep an eye on your inbox for our newsletters on Sundays. If you have any feedback for us, simply respond to this email or message [email protected].

What did you think of today's newsletter?

All the best,

© The Investor's Podcast Network content is for educational purposes only. The calculators, videos, recommendations, and general investment ideas are not to be actioned with real money. Contact a professional and certified financial advisor before making any financial decisions. No one at The Investor's Podcast Network are professional money managers or financial advisors. The Investor’s Podcast Network and parent companies that own The Investor’s Podcast Network are not responsible for financial decisions made from using the materials provided in this email or on the website.