Some investments are elegant. Compounders with powerful advantages, aka “moats,” that grow their earnings per share consistently over time. Others are opportunistic, not necessarily attractive companies on their own, but which might be trading at prices that do make them attractive.

Anyone considering investing in today’s pick with sober eyes would probably recognize that it falls more squarely in the latter category.

Yet today, we’re departing from the familiar territory of scalable SaaS companies and brand-centric consumer products, like Airbnb, Alphabet, Reddit, Nike, and Mercedes-Benz, and stepping into a realm that many investors will find more distasteful: firearms manufacturing via Smith & Wesson (ticker: SWBI).

As such, we ask that you set your views on the issue aside, as we will try to do so, too, and simply look at the company through an investment lens, as we would with any other. This is a name that, if the thesis plays out, could be a 3-6 bagger(!)

More on that, below.

— Shawn

Q&A With William Green

Our colleague, William Green, author of the best-selling book Richer, Wiser, Happier, and host of a podcast by the same name, is considering doing an Ask Me Anything podcast episode (AMA).

For the episode, we’d love to give readers of The Intrinsic Value Newsletter the chance to directly share questions with him to review and possibly answer in the episode.

If interested, please submit your question below.

Smith & Wesson: Opportunity in Sin Stocks?

Not Winning Any ESG Awards

At first glance, Smith & Wesson feels like a relic. A brand synonymous with the Wild West, with roots dating back to 1852, before going mainstream during the Civil War as its revolvers took off in popularity. (Side note: how often do we get to invoke the Civil War when discussing publicly-traded stocks today? Objectively, kinda cool.)

Since then, it has remained iconic, enduring through generations, wars, political movements, and evolving social attitudes. And yet, despite being a household name and still churning out products as relevant today as they were decades ago, Smith & Wesson’s market capitalization hovers at just $400 million. To say the stock hasn’t compounded would be an understatement.

Yet, that hasn’t prevented it from catching the attention of legendary investors like Norbert Lou of Punch Card Management, who, despite trimming Smith & Wesson recently, holds it as one of his four portfolio positions, as disclosed in 13F filings (which may not fully capture the picture of everything he may or may not own, but the point remains.)

Lou is famous for, well, doing exactly what it looks like: running an ultra-concentrated portfolio and sitting on cash or stable bets like Berkshire, until swinging on particularly “fat pitches,” as the expression goes.

Going back to Smith & Wesson, firearms are inherently divisive. That, in theory, creates room for some market inefficiency, as some fund managers are banned from owning the stock, and others simply prefer not to, leaving the market less able to efficiently price its shares. This alone isn’t the thesis (which we’ll get into in a moment), but it’s a factor for consideration.

The idea being: stocks shunned by large portions of the market for non-economic reasons can, and often do, trade at substantial discounts to intrinsic value.

So, is Smith & Wesson a misunderstood deep value gem? Or a classic value trap, cheap for very good reasons? Not necessarily a wonderful business, nor, frankly, even a good one.

On that note, some of the best investment advice I (Shawn) have received is to consider not only why the market is failing to price a company efficiently, which it sometimes does, but also why I am uniquely positioned to capitalize on this inefficiency.

With the short answer to this point being, as free-wheeling individual investors, not bound by ESG mandates or the pressure to produce quarterly results for those that we manage money for, Daniel and I can afford to wait for intermediate-to-longer-term theses to play out, especially around a small and controversial company like Smith & Wesson.

But let’s actually talk about what this thesis is all about, and for that, we should know a little more about the company.

Classic American Brand + Straightforward Business Model

From Smith & Wesson’s Financial Filings

Smith & Wesson is not hiding behind fancy terminology or financial engineering. They’re what they appear to be: a pure-play firearms manufacturer. Pistols, revolvers, sporting rifles, lever-action rifles, silencers, and handcuffs. This is a simple business in structure, albeit complex in societal positioning.

And after spinning off American Outdoor Brands in 2020, Smith & Wesson leaned even more deeply into being essentially nothing more than a gun producer.

Despite its international renown, the company generates approximately 95% of its revenue domestically. As such, their primary market is North America, where a loyal base of enthusiasts, sportsmen, hunters, law enforcement, and even the military, use their products.

Pistols are the crown jewel of its product portfolio, accounting for as much as 75% of total revenues during certain years. Consequently, the company owns an estimated 20% share of the pistol market.

An incredible feat when you consider that, for 160 years, Smith & Wesson has consistently been one of the biggest players, if not the biggest, in this subset of firearms sales. It’s a good niche to dominate, too, given that pistols are the most popular type of firearm in the U.S.

But their leadership extends beyond handguns. Smith & Wesson is also one of the leading manufacturers of silencers — sold under the Gemtech brand — and, as I was surprised to learn, handcuffs, which are standard issue for law enforcement agencies nationwide. These products provide some diversification, though the business remains fundamentally tethered to the volatile dynamics of firearms demand.

Up-and-down sales

In many ways, Smith & Wesson is the quintessential American manufacturer: metal goes in, guns come out. They produce inventory, warehouse it in Missouri, and distribute primarily through wholesalers and retailers. Five large commercial distributors represent nearly 50% of their sales(!)

Simple. Durable. But it’s a business that is not without serious challenges.

Not Built to Compound

In the investing world, compounding is king. Businesses that can reinvest earnings at high rates of return and steadily grow intrinsic value over time are the true darlings of the market. Just to reiterate it again, Smith & Wesson does not belong in that camp.

In fact, this is not a business that has gone anywhere for investors in almost two decades. Shares today trade roughly where they did in 2007, without any notable dividends until 2020, either. Along the way, however, they’ve staged dramatic rallies, often doubling, tripling, and even sextupling from peak to trough during gun-buying frenzies, only to give it all back when demand normalized.

This is a stock, and a business, defined by waves. The story here is not about steady progress. It’s about playing the cycle.

During periods of heightened demand, revenues surge and profitability spikes. Sentiment improves and investors pile in. And then, inevitably, demand fades. Revenue craters. Sentiment evaporates. The stock sells off.

The Stock Has Underperformed Market Indexes for Two Decades With Lots of Volatility

It’s this pattern, and the knowledge that firearm demand is unlikely to permanently disappear, that forms the core of the investment thesis. You aren’t buying Smith & Wesson to hold forever; you’re buying into the next cycle, hoping to snag shares at a discount to normalized earnings and sell at some higher price when the shares (almost inevitably) rocket higher again.

The Anatomy of Firearm Cycles

So what exactly drives these dramatic surges and pullbacks in demand?

Unlike many consumer products, gun sales aren’t particularly sensitive to the usual factors like economic growth, interest rates, or consumer sentiment. Instead, they’re politically and socially driven. Fear, uncertainty, and perceived threats to gun ownership rights are what move the needle.

Political cycles are key. When Democrats gain power and talk of potential firearm restrictions, gun sales often spike, as people rush to buy before regulations tighten. Conversely, when Republicans control Washington and regulatory fears subside, demand usually softens.

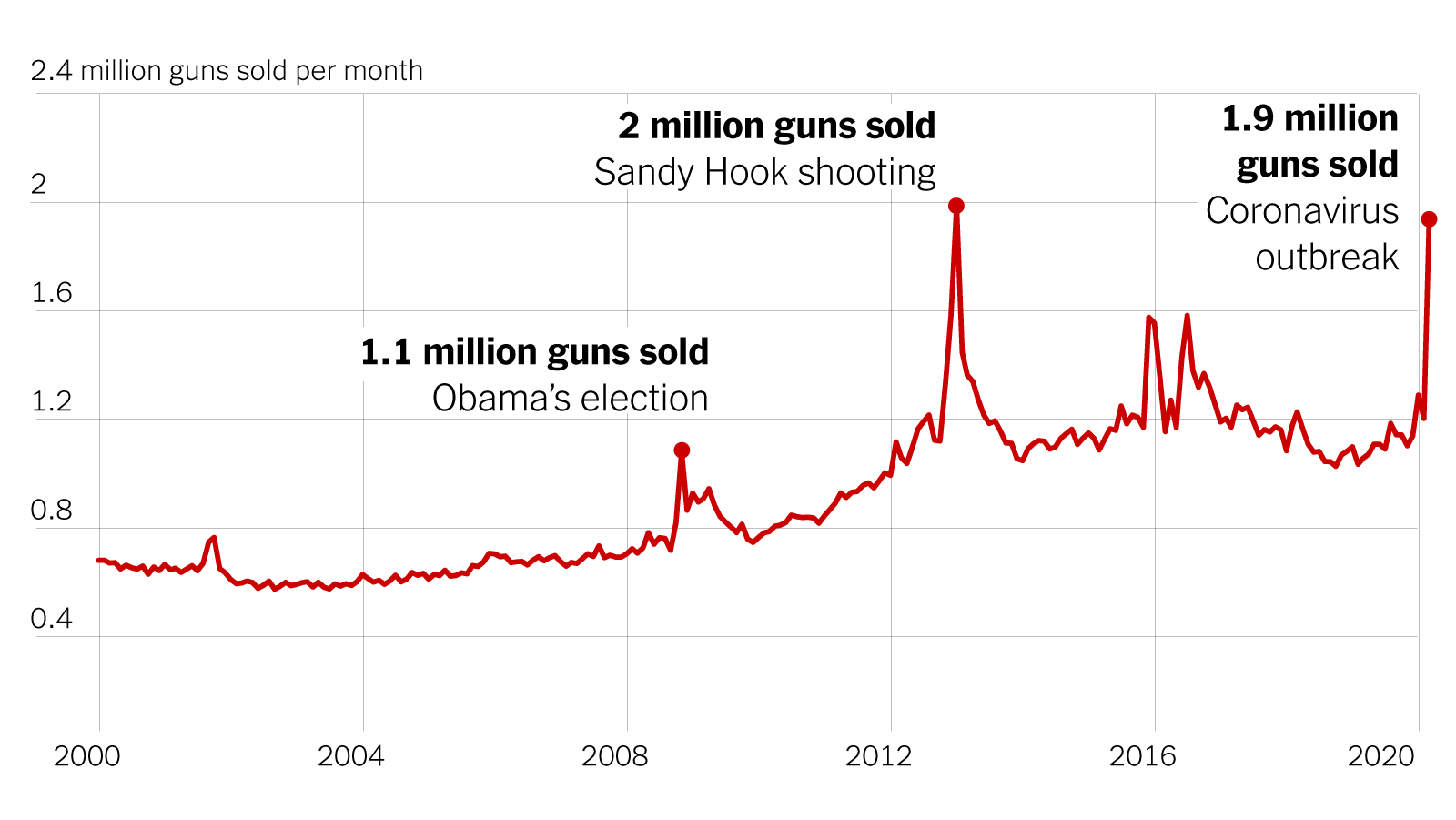

But politics is only part of the story. Broader societal fears, like pandemics, civil unrest, and natural disasters, also play a role. During COVID-19, for example, firearm sales exploded as Americans prepared for worst-case scenarios. Guns, like canned food and generators, became a form of disaster insurance, and a similar trend can be observed in response to mass shooting events:

Trends in firearm sales over time

This makes Smith & Wesson a fascinating investment candidate. At its core, it’s a pure-play on social and political volatility, perhaps even a portfolio hedge against the effects of events that are otherwise damaging to most businesses (i.e, social unrest, pandemics).

The challenge? Timing is impossible to predict with precision. That unpredictability is the risk and the opportunity. There’s no specific catalyst beyond knowing that, if history is any guide, something will once again occur that drives Americans to buy a lot of guns in a short period of time, as has happened every few years.

Yet, while you wait for the next upcycle, the underlying business can decline dramatically, as will the stock.

Given that the company is now trading at the lows it hit before the Pandemic, though, and now that we’re several years out from the last major upswing in firearms sales, the idea here for investors with high risk tolerances is to simply wait for an unknown amount of time, maybe 3 months, 6 months, 18 months, 3 years, or even longer, knowing that unlike other volatile stocks, this company’s business will, with a relatively high degree of confidence, return (and it’s stock will likely surge when it does).

Again, this is a company that has weathered the ups and downs of firearms sales for over 160 years, so betting that there’ll continue to be high highs and low lows in its business isn’t all that speculative, especially given the pedigree of their brand. Smith & Wesson, at this point, isn’t likely to be imminently displaced (as in, competition isn’t a primary concern for disrupting this thesis).

Even better is that, as you wait for the next firearms sales boom, you can pick up a 5%+ dividend yield at current prices, with periodic but aggressive share repurchases, too (shrinking the share base by almost 9% in 2021, for example).

Management and Capital Allocation: Where the Story Gets Messy

If the idea of buying Smith & Wesson was straightforward so far — buy cheap and wait for the cycle to pick up again, while earning a satisfactory dividend in the meantime — here is where things become more complicated. Management’s capital allocation choices have been, frankly, uninspiring.

At a glance, a robust dividend and aggressive buybacks signal confidence and can meaningfully contribute to total returns. However, a deeper look reveals some cracks beneath the surface.

The company’s dividend track record isn’t exactly long dated, going back only to 2020, and the company hasn’t managed capital returns well recently, seemingly over-committing funds to buybacks and dividends while business was booming, only to leave the balance sheet stretched now as the post-Pandemic downcycle has continued.

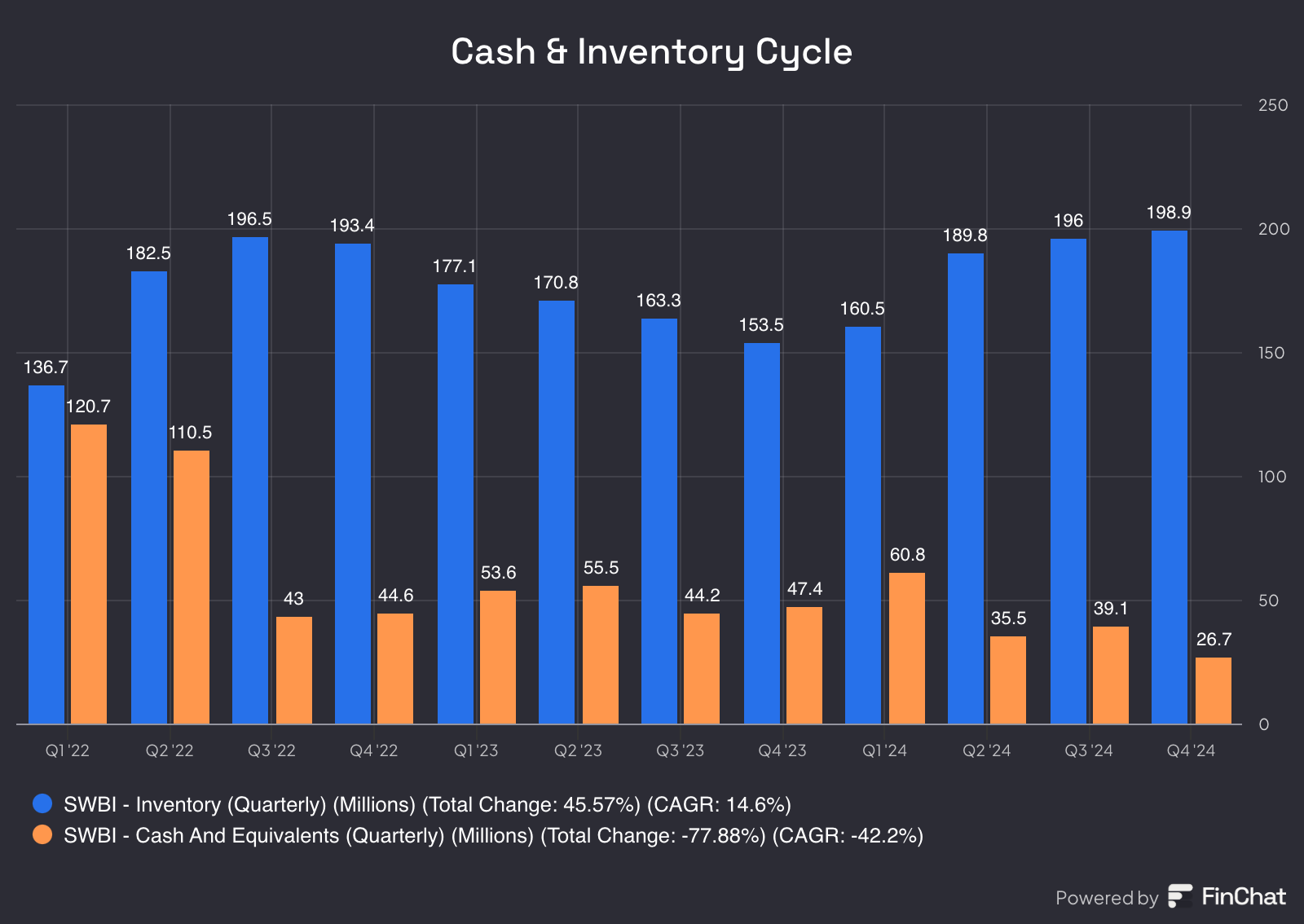

Sales have likely been even weaker than expected following a significant surge in 2020/21, leaving the company with depleted cash reserves. Rather than build up ample cash in the good times to ensure the business’s survival in the bad times, there was, arguably, too much capital returned, particularly via buybacks.

The result? As sales felloff and relocation costs from moving their headquarters from Massachusetts to Tennessee kicked in (they spent almost half the market cap on capex to relocate!), after having already paying out growing dividends and doing massive buybacks, a perfect storm has left the company with just $26 million in cash, far below the $100 million buffer management had said they never wanted to dip below at their 2021 Investor Day.

Cash has fallen very low, as inventories stack up

Now, they do have excess inventory, and the firearms business doesn’t have the type of discounting for old supplies as you might expect in, say, clothing manufacturing, meaning they’ll probably be able to sell much of that inventory at full prices and replenish cash. Still, this is a company that could be a few painful quarters, expensive lawsuits, and other adverse developments away from bankruptcy.

And given the negative externalities of its products, one has to expect that further adverse developments, like local regulatory action driving them out of Massachusetts, for example, can arise at any time for Smith & Wesson, as they already have.

All the more reason to have a judicious cash pile.

Management’s incentive structures do little to inspire confidence, either. Compensation is tied to adjusted operating earnings (“EBITDAS”, as they call it), which strip out many real expenses to smooth the benchmark that management is paid against for a business that is otherwise incredibly volatile. This, combined with the lack of focus on per-share metrics, suggests management’s incentives are not well-aligned with long-term shareholders.

While none of this is fatal to the thesis, it adds nuance. Smith & Wesson could be a 3-bagger when the next upcycle comes, and you might earn a healthy dividend yield in the meantime, but the company could also cancel/cut its dividend and even fail, given their weak cash position.

Owning a cyclical business that is so poorly managed, and that has so many things that can go wrong for it or are beyond its control (again: regulation, lawsuits, boycotts, little to no influence over demand cycles) doesn’t inspire a ton of confidence when discussing waiting indefinitely for the next firearms sales cycle. In a word, it’s speculative.

The Tennessee Relocation: A Non-Trivial Event

Celebrating the new headquarters in a more gun-friendly state

To quickly pull the thread further on Smith & Wesson’s exodus from Massachusetts, amidst all the cyclicality and management missteps, I should mention that this has been a $180 million move from Massachusetts to Tennessee. For context, that figure, as mentioned a moment ago, is almost half of the company’s market value.

While expensive and disruptive in the short term, this relocation was done for strategic reasons. Tennessee offers a much friendlier regulatory environment for firearms manufacturing, reducing future political and legal risk. But the cost was steep, and I see it as one sign, of many, of the costs and headwinds that face a company that large chunks of the population dislike and government cohorts are actively working to sanction.

Sometimes, probably most times, unloved stocks are rightly unloved.

Now, if we were to continue with the bull thesis, I might argue that, for two years, this relocation inflated capex and obscured the company’s true free cash flow generation. In a normalized year, Smith & Wesson’s maintenance capex (the amount it needs to reinvest to maintain the scope of its current business, but not necessarily to grow) is closer to $30 million, far below what’s been recorded recently.

Normalizing capex, in addition to trying to normalize the company’s sales fluctuations, is critical to getting a clearer picture of the company’s ongoing earnings power and potential return profile.

Valuation: Understanding Owner’s Earnings and Yield

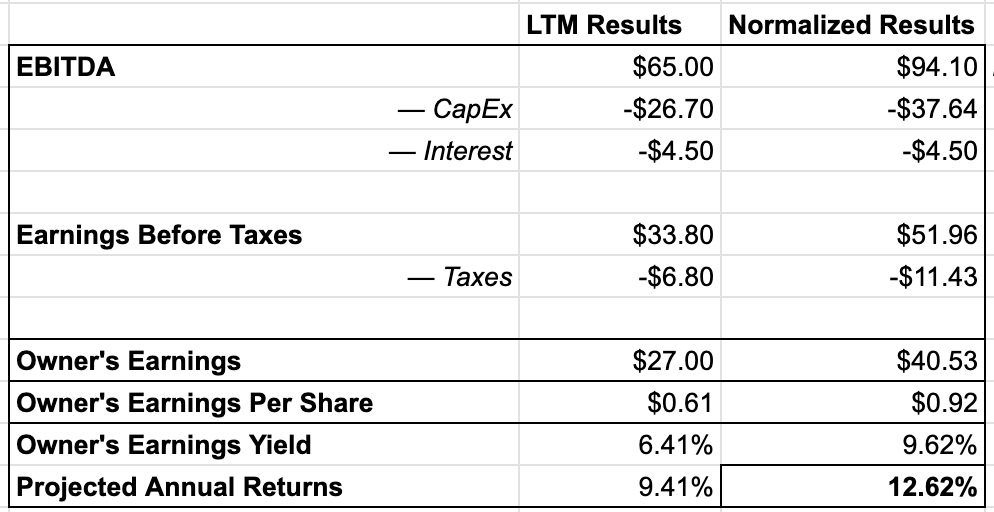

At today’s prices, Smith & Wesson trades at ~15-16x depressed earnings. That’s hardly screaming cheap. But as with all cyclical companies, trailing earnings can be misleading.

When adjusting for normalized production levels and stripping out one-time relocation costs, Smith & Wesson’s earnings power looks better. On this adjusted basis, the P/E multiple drops closer to 10x. That, combined with growth that just matches inflation, suggests a potential double-digit annual return at current levels in owner’s earnings terms.

Backdoor Owner’s Earnings Calculation — Assumes Growth in Line With Inflation (~2-3%)

Smith & Wesson isn’t reinvesting heavily to grow its earnings power, as maintenance capex largely matches depreciation. Therefore, normalized free cash flow is mostly distributable — it can be used for dividends and buybacks, as we’ve seen.

Where things get interesting, and where the true upside lies, is in timing the next firearm sales surge, whenever it comes.

To recap quickly, though: The bull case is betting that A) Smith & Wesson is cheap when you average out its earnings (normalizing them) across time, B) the dividend yield is attractive in compensating you while waiting for the next cyclical spike and C) history shows that there’s serious optionality embedded in the stock/business and that might be underpriced for different reasons (uncertainty around cycle timing, dislike of firearms companies, ESG mandates on who can invest in what, etc.).

This optionality means that you’re being paid to wait via dividends and buybacks, and if history repeats, the stock could see significant upside during the next boom in gun sales. That’s it, that’s the whole idea. It’s simple, but we also went through why it’s more nuanced, too.

So, is it a bet that Daniel and I want to make?

Portfolio Decision & Risks: Why the Discount Exists (and Should)

For starters, we can normalize as much as we’d like in Excel, but that doesn’t mean anything for the business if things don’t pick up again, and its cash position continues to deteriorate. Remember Yogi Berra’s wise words: "In theory, there is no difference between theory and practice - in practice, there is.”

I can sit here and explain why Smith & Wesson may be cheap, if you spread out its sales surges over time, but what scares me here is not having a catalyst. If I had advanced insight that another pandemic was coming, or that Congress was about to pass some law that would try to restrict firearms sales (causing everyone to go out and buy them while they can), it would be a no-brainer to buy Smith & Wesson.

If I even had just a little more confidence in management or in the company’s financial position, I could probably convince myself to take the risk and try to hold on until this thing catches fire again.

But I don’t. I don’t feel confident that the dividend can persist at its current size (70% of last year’s depressed free cash flow), and I don’t think $26 million in cash is enough to comfortably run a manufacturing business, at least not without taking on more debt.

There’s truly very little margin of safety here. A negative result in one of the many lawsuits they’re a plaintiff in could add even further strain on their cash, at a time when there are no major catalysts on the horizon to reignite gun sales, though the recent protests in LA will likely contribute to a modest uptick in sales, which is presumably why $SWBI has rallied over the last month.

As I dug deeper into this idea, what first seemed very promising (iconic brand, big dividend, buybacks, and the optionality for explosive growth) made me realize just how difficult this business is to run and how much of a gamble it is to bet on them.

After some initial excitement about the idea, I advised Daniel that we pass, and he’s in full agreement. It’s a good reminder to me that looking for hidden value is a tough game to play, and generally, I’d rather try to own shares in the best businesses in the world (perhaps even in the history of capitalism?) with tech-platform giants like Alphabet, Airbnb, Adobe, and Uber, or at least companies with excellent operating track records in otherwise mediocre industries like Ulta.

Final Thoughts

To wrap things up, I’ll say that gun sales, for better or worse, remain a recurring feature of American life. Waves of panic buying are as inevitable as they are unpredictable. And Smith & Wesson, as the country’s leading firearms manufacturer, is poised to benefit when those waves arrive.

In the meantime, shareholders are compensated with a substantial dividend and periodic buybacks, albeit funded somewhat precariously. While the balance sheet leaves little margin for error, normalized earnings power suggests a path to double-digit returns, and maybe much better with a well-timed sale during a period of elevated volatility in the stock, for those willing to roll the dice.

This isn’t appropriate for a core portfolio holding, though, and that’s what we’re really looking for. Anyone thinking about Smith & Wesson, please tread carefully and do further research yourself; there’s a good chance this is a value trap.

Weekly Update: The Intrinsic Value Portfolio

Notes

Obviously, no changes to the portfolio this week, and next week, we’ll be doing a special portfolio review newsletter, reflecting on Daniel and I’s picks, our criteria for adding new investments, sharing extended updates on our portfolio companies, and discussing how we think about position sizing. It’s our “mid-year recap”!

Adobe, a 5% holding for us, reported earnings last Thursday. Despite a mixed reaction from the market, by all fundamental measures, it was a great quarter, and Adobe just keeps chugging along. We believe Adobe is uniquely positioned to leverage AI in its product ecosystem to drive further subscription growth and renewal from professional clients, as opposed to being massively negatively disrupted by AI, as many currently fear.

Between continued double-digit earnings growth and multi-billion-dollar buybacks, we see a lot to like about Adobe below $400 per share.

Quote of the Day

"Patience is not just about waiting. It’s about keeping a good attitude while waiting."

— Joyce Meyer

What Else We’re Into

📺 WATCH: Bill Ackman’s keys to long-term investment success, an interview with Forbes

🎧 LISTEN: Richer, Wiser, Happier Q2 2025, with Stig Brodersen

📖 READ: How Meta will monetize WhatsApp with ads

You can also read our archive of past Intrinsic Value breakdowns, in case you’ve missed any, here — we’ve covered companies ranging from Alphabet to Airbnb, AutoZone, Nintendo, John Deere, Coupang, and more!

Your Thoughts

See you next time!

Enjoy reading this newsletter? Forward it to a friend.

Was this newsletter forwarded to you? Sign up here.

Use the promo code STOCKS15 at checkout for 15% off our popular course “How To Get Started With Stocks.”

Follow us on Twitter.

Read our full archive of Intrinsic Value Breakdowns here

Keep an eye on your inbox for our newsletters on Sundays. If you have any feedback for us, simply respond to this email or message [email protected].

What did you think of today's newsletter?

All the best,

© The Investor's Podcast Network content is for educational purposes only. The calculators, videos, recommendations, and general investment ideas are not to be actioned with real money. Contact a professional and certified financial advisor before making any financial decisions. No one at The Investor's Podcast Network are professional money managers or financial advisors. The Investor’s Podcast Network and parent companies that own The Investor’s Podcast Network are not responsible for financial decisions made from using the materials provided in this email or on the website.