They say fashion trends come and go, but true luxury never goes out of style. In a world where technology dominates headlines and consumer fads flare up and fizzle out, LVMH (Moët Hennessy Louis Vuitton) stands as a testament to the enduring appeal of high-end goods and experiences.

If you’ve ever walked down Fifth Avenue in New York or Avenue Montaigne in Paris, you’ve probably seen a long line of people outside a Louis Vuitton store.

And if you’re like us, your first thought might be: why is anyone willing to wait 45 minutes just to spend $5,000 on a handbag?

It’s a business that’s stitched together a tapestry of brands so valuable and so desirable that people not only line up to hand over their money, they walk away thrilled for the privilege.

Today, we’ll explore how Bernard Arnault pulled off one of the most impressive business transformations of the last century, how LVMH’s conglomerate model compares to Berkshire Hathaway’s, and whether this luxury titan is undervalued after falling more than 30% in the last year.

Let’s dig in.

— Shawn

Want to go to Montana With Us?

The Investors Podcast Network is hosting our Summit Event in the mountains of Big Sky, Montana!

Attendees will have the opportunity to meet like-minded value investors and enjoy delicious food in a wonderful setting. We have no doubt that this will make for an unforgettable experience.

Rather than hosting yet another conference in a room full of suits, we decided that there was no better place to meet kindred spirits than in the serenity of the mountains, away from all of the noise.

Sounds fun, right? You can apply to join below (spots are limited).

P.S. Members of our Intrinsic Value Community get a special discount to attend.

LVMH: The Power of Scale Behind a Luxury Conglomerate

LVMH: The Great Luxury Empire

Louis Vuitton, Christian Dior, Moët & Chandon, Hennessy, Sephora, Tiffany & Co., and the list goes on. These are just a few of the 75 distinguished “houses” that make up LVMH’s empire of luxury. The Paris-based conglomerate has built an unparalleled portfolio of brands spanning haute couture fashion, fine wines and spirits, perfumes and cosmetics, jewelry and watches, as well as boutique retail.

If you’ve ever sipped a glass of Veuve Clicquot champagne at a celebration, sprayed a bit of Guerlain perfume, or admired someone’s TAG Heuer watch, you’ve interacted with LVMH’s products. It’s the company behind life’s little (and not-so-little) luxuries, the kind that carry premium price tags and storied histories.

Veuve Clicquot champagne

Despite its vast scale today, LVMH’s reach can be easy to underestimate. Each of its brands retains a unique identity, often operating with a high degree of autonomy.

Consumers might love a Fendi handbag or a Bulgari necklace without necessarily thinking about LVMH at all. LVMH provides the financial backing, global distribution, and managerial expertise, while letting each maison (or house) preserve its own mystique and heritage.

This has made LVMH into a giant. In 2024, the group generated roughly €80+ billion in revenue, an astonishing figure for a business built largely on discretionary consumer purchases. Its flagship Fashion & Leather Goods division (powered namely by Louis Vuitton) makes up LVMH’s financial backbone, with ~40% operating margins that rival some of the great software businesses out there.

Not all of its units enjoy the same margins, but still, LVMH’s profitability stems from the pricing power of its brands. When your product is a must-have item for the affluent, you can charge accordingly and rarely need to discount.

Global Reach

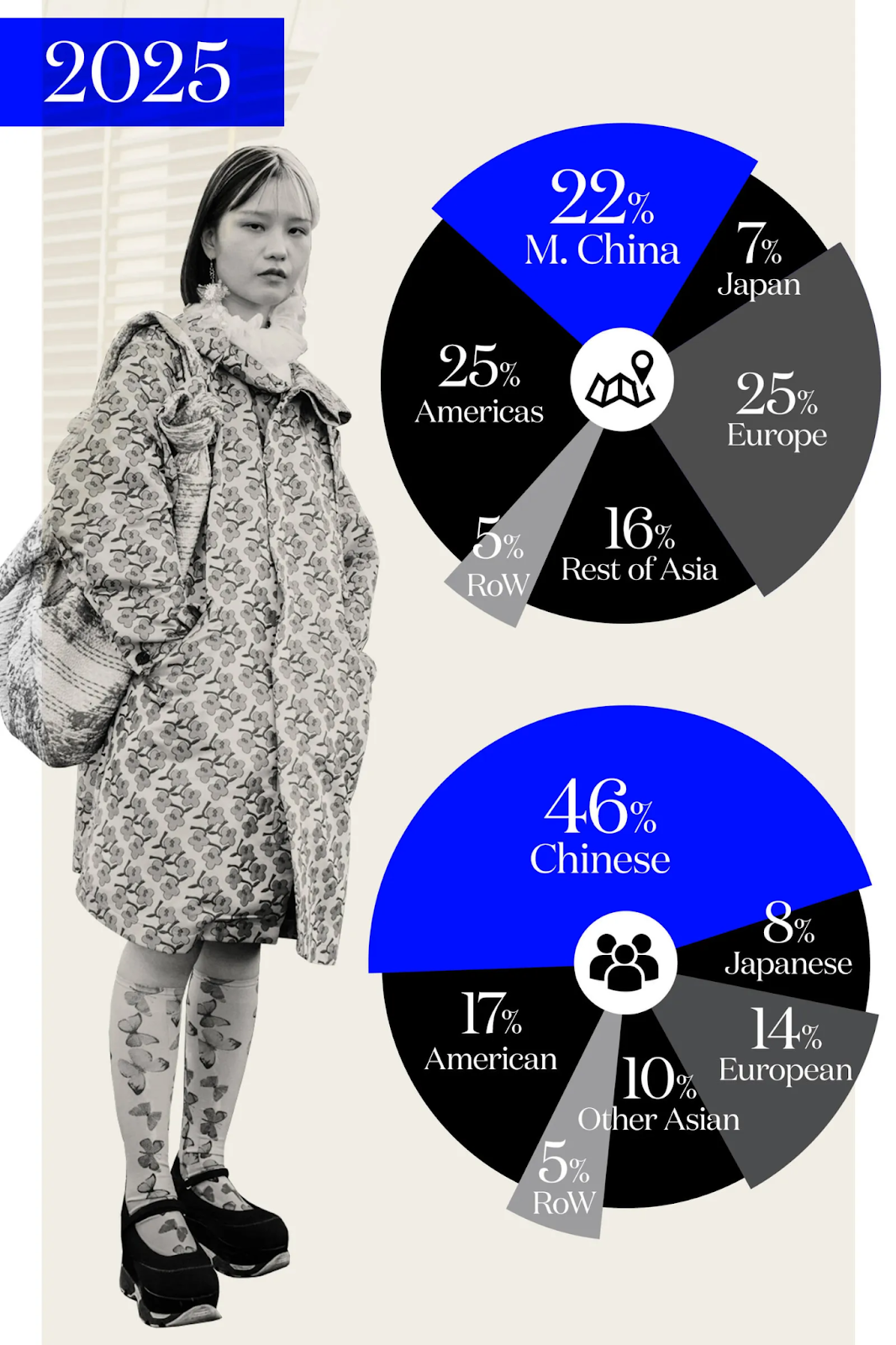

It’s also telling where those sales come from. LVMH is a global business with a footprint in over 70 countries, but a huge portion of revenue is driven by one key demographic: the growing ranks of the affluent, especially in Asia (notably China) and the United States.

Estimate of Chinese shoppers’ share of luxury goods sales in 2025

The aspirational appeal of these brands transcends cultures and generations.

For the emerging middle and upper classes in developing markets, a luxury purchase from an LVMH brand is often a milestone, a symbol of having “made it.” For the ultra-wealthy globally, LVMH’s highest-end offerings (say a custom Louis Vuitton trunk or a rare vintage from Château d’Yquem) are simply part of living the good life. This broad and deep demand pool has helped LVMH continue growing year after year.

Arnault’s First Move Into Luxury

Every empire has an origin story, and LVMH’s begins with an audacious deal by Bernard Arnault.

In fact, you may recognize some parallels with Warren Buffett’s.

The year was 1984. Arnault, a young French real estate developer, set his sights on a bankrupt textile conglomerate named Boussac Saint-Frères. Boussac was no prize on the surface: it was bleeding cash and came with a bloated mix of businesses, including textile factories and even a diaper brand.

Arnault acquired this nearly bankrupt textile company (like early Berkshire), and slowly reshaped it into a compounding machine.

But unlike Buffett, who built Berkshire Hathaway into a financial empire, Arnault’s path was rooted in something a bit more intangible: taste. Rather than accumulating wonderful, simple businesses at fair prices like Buffett, Arnault focused on accumulating the most powerful aspirational lifestyle brands in the world, amplifying their power with economies of scale (more on that later).

Going back to the story, Boussac was failing when Arnault stepped in, but it had one hidden jewel in Christian Dior, the famed Parisian couture house founded in 1946, which Boussac owned. Dior still had global prestige and untapped potential, and Arnault recognized it.

So Arnault stripped out the rest—the diapers, the department stores, the clothing factories—and kept Dior, even after promising the French government, which had previously nationalized Boussac, that he wouldn’t break the company apart or do layoffs.

While hailing from an industrial family, not a lineage of fashion and craftsmanship, Arnault has famously recounted how when, while living in the U.S. briefly, a taxi driver in NYC told him he didn’t know who the President of France was, but he did know one thing about France: it was the home of Dior.

It was supposedly a light bulb moment for him, where he realized how powerful an undermonetized (at that time) but global brand like Dior could be.

Dior —> Luxury Conglomerate

Dior would be the cornerstone of Arnault’s luxury ambitions, but the real scale came a few years later with the formation of LVMH itself. In 1987, a merger brought together Louis Vuitton (the famed luxury trunk and handbag maker, established in 1854) with Moët Chandon and Hennessy, two iconic alcohol brands that had merged in 1971 to form Moët Hennessy.

Thus, LVMH was born as a multi-sector luxury group. However, the merger didn’t automatically put Arnault in charge; at first, he was a minority stakeholder invited in as part of a delicate alliance between the Vuitton family and the Moët Hennessy executives.

Bernard Arnault

The Vuitton side had invited Arnault to acquire a stake in LVMH, hoping he would increase their collective voting power and influence over the company, after rumors emerged that Guiness was considering investing in LVMH, which they worried would tilt LVMH into being more of an alcohol-focused conglomerate, favoring the Moët Hennessy side.

What followed is the stuff of corporate legend and perhaps what earned Arnault nicknames like “the Wolf in Cashmere.” Sensing an opportunity to take control, and realizing that the Vuitton side didn’t have the financial firepower to win, Arnault methodically increased his ownership stake in LVMH to support his aims and betrayed the Vuitton side.

Through a series of tactical stock purchases and deft navigation of a power struggle between the Moët Hennessy and Vuitton camps, Arnault eventually gained majority voting power and ousted the other leaders by 1990. And by the early 1990s, Bernard Arnault was the unquestioned chairman and CEO of LVMH, with a controlling stake in the company.

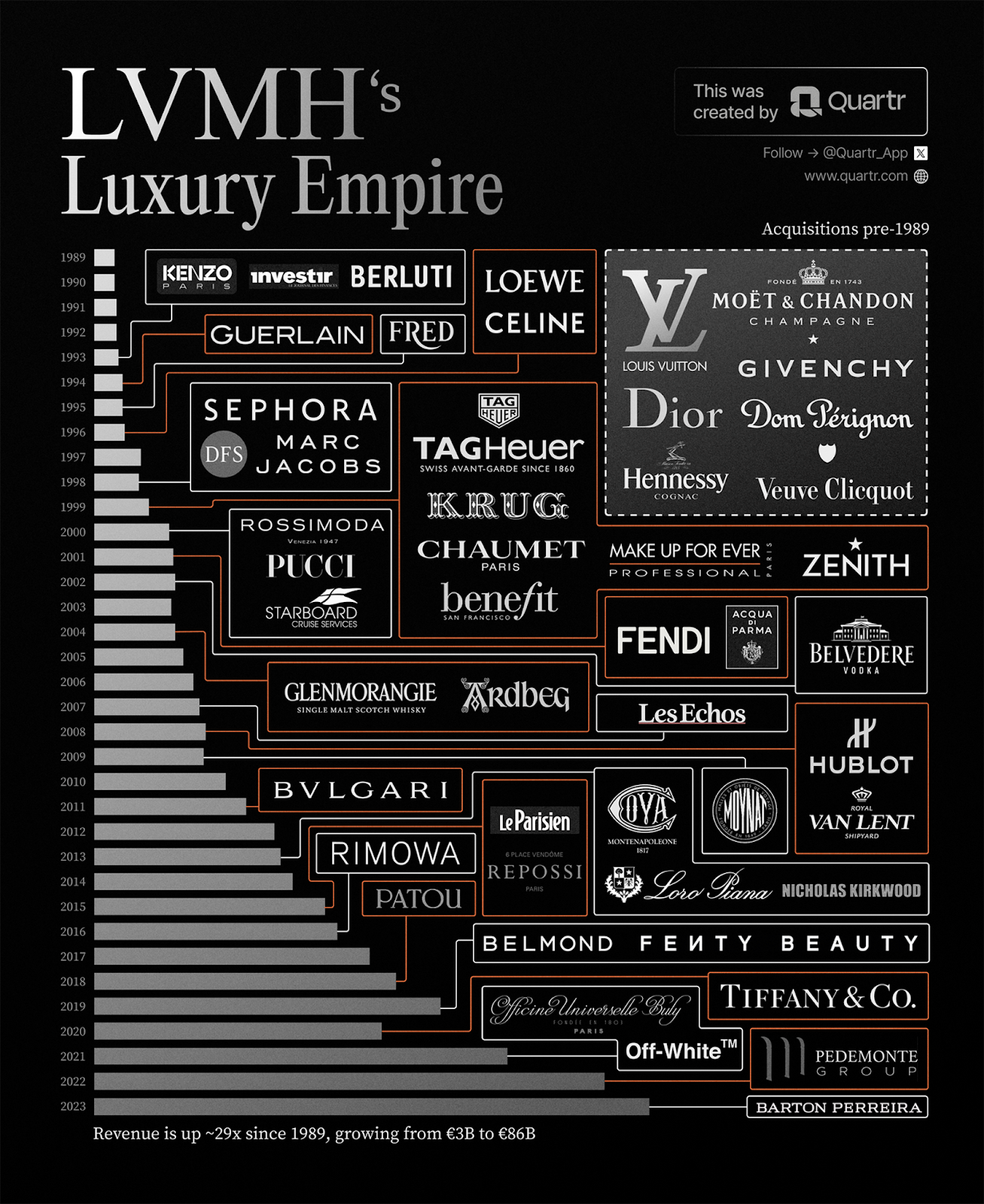

Then the fun really began. The 1990s and 2000s were a shopping spree for LVMH: From Guerlain to Sephora, Tag Heuer, and Fendi, to name just a few. More recently, LVMH made headlines with its largest takeover ever in purchasing the iconic jeweler Tiffany & Co. for approximately $16 billion in 2021.

Arnault showed a knack for revitalizing prestigious brands with lagging businesses by plugging them into the conglomerate, which could offer more financial resources for marketing and could attract deeper talent pools, since the best designers are drawn to LVMH and retained, in part, for the opportunity to move across its portfolio of brands, as opposed to working for a single standalone brand/company like Chanel or Hérmes.

So there has been an economies of scale benefit, but not in the way that’s taught in Econ 101, with low-cost production advantages stemming from size. LVMH was the first global luxury goods conglomerate, and instead, as mentioned, has used its scale to consolidate the best creative talent in the world and secure the most valuable partnerships, from Rihanna’s Fenty to working with Jay-Z on his Ace of Spades champagne or pairing Louis Vuitton with the popular streetwear brand Supreme.

LV + Supreme Collab

Arnault ultimately has tried to empower creative directors (designers, winemakers, etc.) to have the freedom to innovate and maintain a brand’s soul, but within a framework that ensures profitability and consistency with luxury positioning.

As such, LVMH’s business model is remarkably decentralized. Its brands operate with an incredible amount of autonomy, each with its own CEO, creative director, and manufacturing footprint.

There is no central "LVMH factory" pumping out Louis Vuitton and Dior handbags. Each maison controls its own production. There’s also no centralized P&L, at least not in the way most businesses operate. Each house is expected to stand on its own two feet.

But like Berkshire, all of the excess capital flows up to headquarters, where Arnault decides where to deploy it next.

Luxury, Not Premium

At this point, I should clarify a subtle difference in language and define what “true luxury” means.

This isn’t like the fast fashion we see with a lot of Italian bands. Brands like Hermes, Louis Vuitton, and Burberry are timeless, and they’re also crafted in Western Europe, as opposed to being sent to China or Vietnam for production, where costs are the lowest, which is the opposite of what we’re taught in business school to do.

So there is something unique and contradictory about true luxury compared to what we’d expect from almost all other types of businesses. For starters, production isn’t and shouldn’t be outsourced to the place with the lowest cost of production. That would damage brand perception. An LV bag with a Made in India/Vietnam/Thailand/China label would, rightly or wrongly, be perceived as less valuable than one “Forged in Italy.”

Cristian Bilinger, a recurring guest on our sister We Study Billionaires podcast, is so strict with the definition of true luxury that he has even said he doesn’t consider Mercedes to be true luxury, because there’s too much of a focus on performance and sales volumes.

Mercedes, then, is a premium product, where you’re paying a price for something that is functionally better and more useful than a lower-end vehicle model, but not a true luxury product.

With true luxury, the purchase is meant to transcend functionality. A Luis Vuitton purse isn’t any more functionally useful than any other purse, and everyone knows that, so instead it’s a purchase that signals someone is paying this price not because they want a more useful product, which is what we all do in most cases when we’re shopping, but instead they’re paying a higher price to show that they have good taste and can afford to pay more for the sake of doing so.

As Coco Chanel has put it, “Luxury is a necessity that begins where necessity ends.”

Where Mercedes is more of a premium product, competing on functionality, Ferrari and Lamborghini are more like true luxury brands. They perform very well, but that’s not really the reason people buy them. As a true luxury brand, people want a best of the best product, yet they’re willing to pay a price that goes well beyond that for the status of it, much more so than is the case with Mercedes or BMW.

The thing with true luxury is that, in some cases, the more you raise prices, the more attractive the products actually become. It’s as if paying for functionality and practicality is too pedestrian; it’s almost beneath these people to think about something as menial as whether an item is overpriced relative to its usefulness.

Here’s a quote from a great book on the topic, The Luxury Strategy, that shows the point well:

“Here lies the difference between luxury and premium. People buying premium or even super-premium cars like to justify every dollar by a return on investment.

Premium means pay more, get more in functional benefits. Luxury is elsewhere: it signals the capacity of the buyer to transcend needs, functions, or objective benefits. This is how luxury brands are different from premium or super-premium brands: beyond the experience, they bring creative power, heritage, and social distinction.”

Empire of 75 Houses: All Sectors, All Stars

Today, LVMH oversees 75 distinct brands, an empire so vast that it’s the only luxury group present in every major luxury category. In that sense, LVMH is in a category of its own, size-wise, trailed by smaller rivaling luxury conglomerates like Richemont (owner of Cartier) and Kering (owner of Gucci) and pureplay brands, like Hérmes, that sell nothing other than Hérmes-branded products.

With the company’s diversification across different units, when one part of the luxury market faces headwinds, another might be booming – a form of hedging that smaller rivals can’t easily replicate.

LVMH’s Segment Breakdown

Here’s the breakdown of LVMH’s empire by segment:

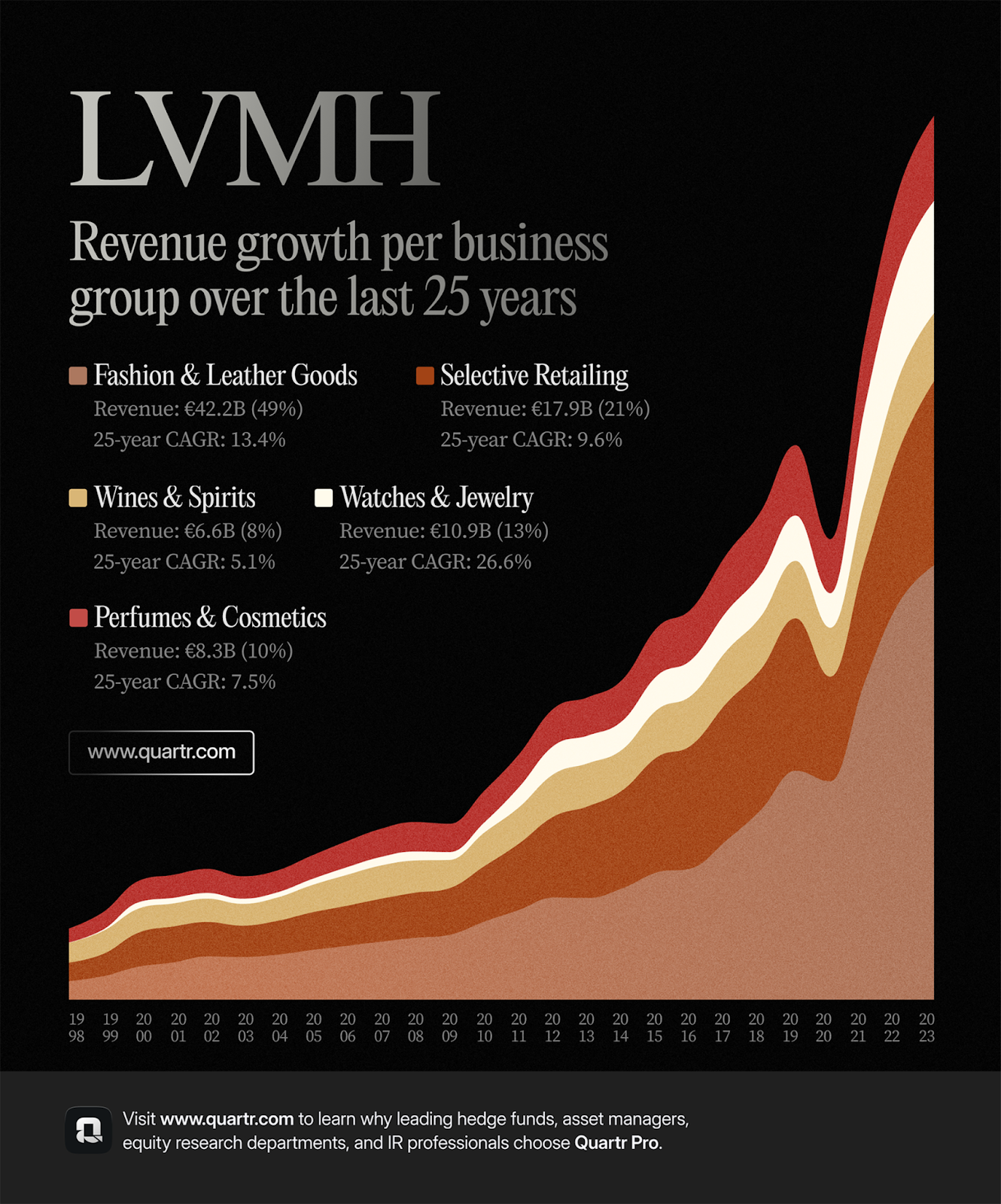

Fashion & Leather Goods: This is the powerhouse segment, contributing the lion’s share of revenue and profit. Brands like Louis Vuitton, Dior, Fendi, Celine, Loewe, and Marc Jacobs fall under this umbrella. Louis Vuitton in particular is the crown jewel – it’s often cited as the world’s most valuable luxury fashion brand. Increasingly, many customers see these products as investments that may gain value over time, and because a good handbag can go with just about any outfit, the expense can be more easily justified for many shoppers than spending the same on a dress that might only be worn once.

Wines & Spirits: Think Moët & Chandon, Veuve Clicquot, Dom Pérignon, and Krug for champagnes, as well as Hennessy cognac, and Scotch whiskies like Glenmorangie and Ardbeg. A vintage bottle of Dom Pérignon or a rare Cognac can cost thousands. What’s interesting is that the dynamics of luxury alcohol are different; vineyards and aging processes constrain production, so volume growth is modest, but pricing power is immense for the top marques. I should note, though, that LVMH has a strategic partnership with Diageo, so some of the profits from this unit belong to Diageo.

Perfumes & Cosmetics: Think Parfums Christian Dior, Guerlain, and Givenchy perfumes. It’s a highly competitive space (the beauty industry is full of giant players like Estée Lauder, L’Oréal, etc.), but LVMH leverages the desirability of its fashion names to sell fragrances, like J’adore by Dior, and makeup. Sephora, acquired in the late 90s, has become a global chain and one of the largest beauty retailers, giving LVMH a strong distribution arm and insight into beauty trends. While this segment has lower margins than handbags or cognac, it serves as an entry-level luxury product that can recruit younger or less affluent customers into the LVMH ecosystem.

Watches & Jewelry: A segment that has grown dramatically in recent years, especially after the Tiffany & Co. acquisition. Key brands here are TAG Heuer, Hublot, Zenith, and Bulgari watches, plus Chaumet and now Tiffany in jewelry. LVMH’s strategy has been to beef up its presence aggressively – Bulgari and Tiffany give it two world-class jewelry pillars, one rooted in Rome, one in New York. The watch business, led by TAG Heuer and Hublot, positions LVMH in the high-end sports and fashion watch segments, although not yet in the ultra-high-end segment dominated by Rolex and Patek Philippe.

Selective Retailing & Other: This includes Sephora, DFS (Duty Free Shops in airports), and other boutique operations like Le Bon Marché, a prestigious department store in Paris, as well as LVMH’s hospitality ventures, including high-end hotels like Cheval Blanc and the Belmond chain. The retail segment is generally lower margin, given the costs of running stores, but it provides strategic channels to reach customers.

The Luxury Moat: Branding, Heritage, and Pricing Power

Warren Buffett often talks about companies having economic moats. These are durable competitive advantages that protect their profits, and it’s something we look for in every company we cover. In LVMH’s case, the moat isn’t a single thing but a combination of intangibles and practical advantages that together make it incredibly hard to disrupt.

The most obvious moat is the strength of LVMH’s brand portfolio. These brands have been cultivated over decades, some over a century. Louis Vuitton’s LV monogram, for example, has been a status symbol since the late 19th century, initially adorning the travel trunks of European elites and now adorning handbags and sneakers for a global middle class. New competitors can’t easily replicate that history or emotional connection.

When consumers buy luxury, they’re not just buying a product; they’re buying a story, an identity, a piece of heritage. LVMH’s brands have authentic stories in spades: the glamour of Dior’s post-war New Look, the craftsmanship of a Bulgari artisan in Rome, or the legacy of Champagne houses that have toasted royal weddings and celebrity Oscar wins. These narratives create aspiration, as people dream of owning a piece of that history. That dream can’t be engineered overnight by a startup.

One hallmark of LVMH’s moat is its ability to raise prices with minimal pushback. Each year, that pricing power enables most of its brands to quietly increase prices on key products without significant declines in sales volumes. A handbag that cost $3,000 a few years ago might be $4,000 now. In fact, sometimes higher prices increase desirability in luxury, as I mentioned earlier — in economics, this is known as the “Veblen Effect,” where a product is coveted because it is expensive. It goes without saying that this makes for great business economics for those who produce Veblen goods.

As such, many luxury items are produced in limited quantities or have waitlists, creating an aura of scarcity. Even in more mass-market segments like cosmetics, they use scarcity via special editions or limited-run collaborations to spur excitement.

LVMH Without Arnault?

The Arnault Family

With Bernard Arnault now in his mid-70s, the topic of succession comes up frequently.

However, he has placed his children in key roles across the group’s brands, signaling a plan to keep the company family-controlled and philosophically consistent even after he eventually steps down. That continuity could be considered part of the moat, unlike some public companies that suffer from short CEO tenures or strategy shifts, LVMH’s management approach has been remarkably consistent for decades.

Perhaps Arnault will take the Buffett route, once again, and manage the business until his 90s. While you’d expect a drama like HBO’s Succession brewing over who will replace him, the whole thing has been remarkably cordial thus far. The politics of it all, at least, haven’t leaked into the public eye yet.

Bernard Arnault is famously private, and so, it’s little surprise that he’s kept his succession plans under such tight wraps. My impression, though, is that each of his children, despite benefiting from some nepotism, has in many ways genuinely earned their positions. By all accounts, they’re each brilliant and incredibly hardworking, so it’s not what you’d expect, where the next generation is spoiled and less driven.

Point being, I (Shawn) wouldn’t see Bernard’s departure as an imminent concern. Mostly because it may not be imminent, but also because the succession tree seems quite capable and, like Berkshire, the conglomerate has such a powerful portfolio of brands/businesses that will power its enduring success.

Valuing True Luxury

So, we’ve gotten the lay of the land. We know what true luxury means, we understand the pedigree of LVMH’s brands, we appreciate how Bernard Arnault transformed LVMH and the broader luxury industry, and now, we need to bring it all together and try to value the stock.

Since there are a number of publicly-traded luxury companies, we have some good peer comps to compare LVMH against, so let’s start there.

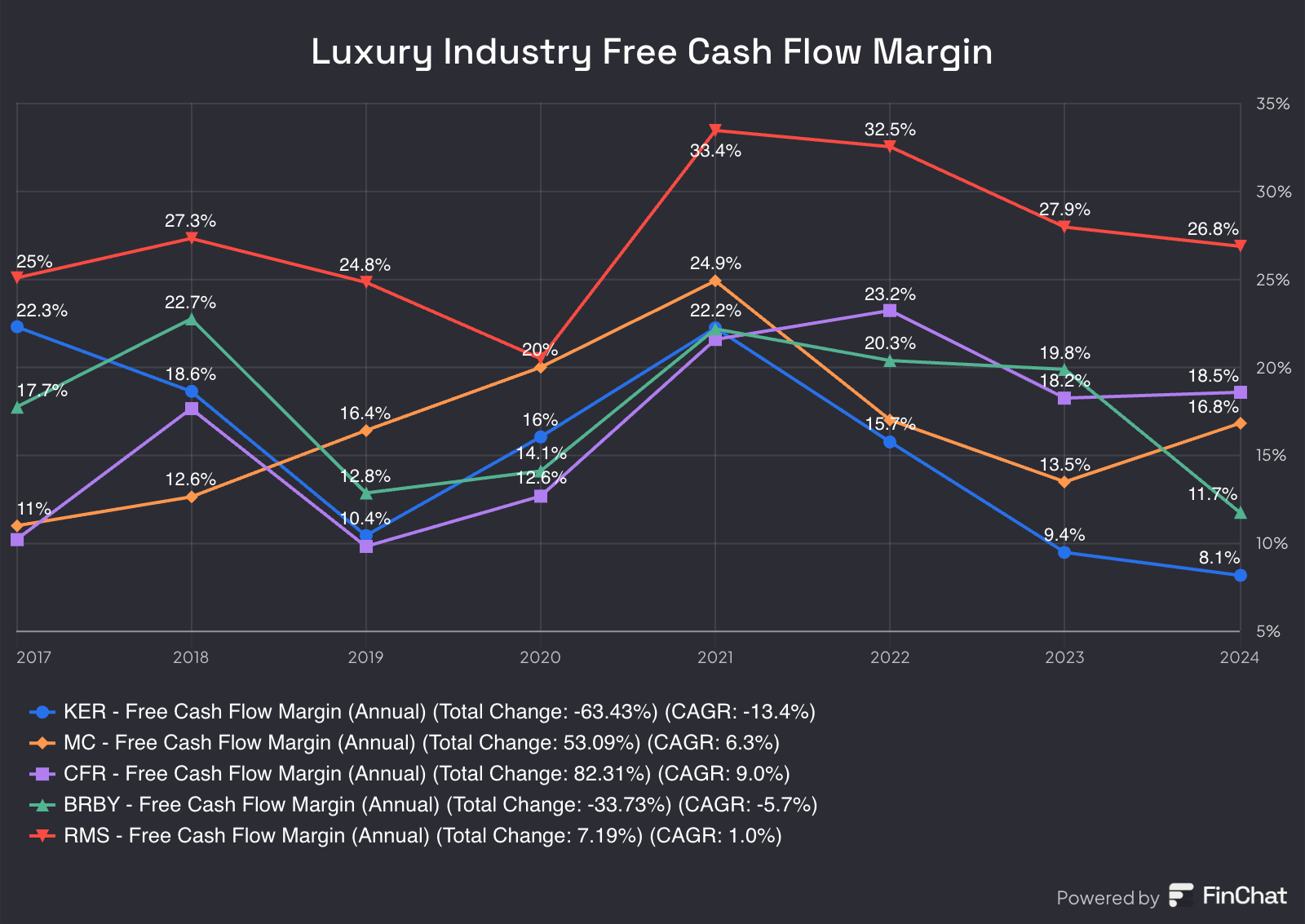

If you chart it out, you’ll see that for LVMH, compared to companies like Kering, Hermes, Burberry, and Richemont, Hermes has by far the best numbers.

It has had higher sales growth than LVMH, 40%+ returns on capital on average over the last 5 years, and a free cash flow margin that is 8 to 18 percentage points higher than these other luxury companies. But at the same time, it trades at more than 60x free cash flow, so you’re paying a massive, massive premium to own this incredibly high-quality company.

MC = LVMH, RMS = Hérmes, CFR = Richemont

And with LVMH, it’s a much more diversified conglomerate, meaning it doesn’t grow as fast and its returns are lower, both in profit margin terms and returns on capital terms, probably because they have had to make a number of costly acquisitions to keep growing outside of their core leather goods business.

So, in an industry defined, literally, by quality, LVMH is probably not the highest quality based on just the financial metrics, but in valuation terms, it is right there in line with Kering and Burberry at 17x free cash flow (see below), yet I do think there’s a good argument for LVMH being a significantly better business than either of these companies. Kering, for example, hasn’t really grown sales at all in the last few years, and its free cash flow margin is half that of LVMH, so I don’t think it has any business trading at the same valuation as LVMH.

And it’s the same story, and actually worse, at Burberry. It blows my mind that LVMH is valued similarly to these clearly inferior businesses.

MC = LVMH, RMS = Hérmes, CFR = Richemont

Betting on normalization in multiples isn’t something I like to make a driving factor in my investments, but this relative pricing of LVMH, combined with everything else we’ve covered today, could certainly get me bullish.

Not to say LVMH should trade at 60x free cash flow like Hermes, but it should be somewhere in between these two extremes, in my opinion. As recently as March 2024, that’s exactly where LVMH was valued at, too, at 37x free cash flow, so it’s pretty incredible how much the valuation multiple on it has contracted.

Over the last decade, its median price-to-free cash flow valuation has been 25x, so again, relative to its own valuation history and some lower quality peers, LMVH just seems way too cheap at the moment.

In relative pricing terms, you could argue that it’s maybe 20-30% underpriced, but again, Daniel and I don’t use that as a driving factor alone for an investment.

How Does the Stock Look Through a More Traditional Earnings Valuation?

I made three different models: a bull case, a base case, and a bear case.

In my base case, I try not to make any assumptions that are too optimistic, so even though LVMH’s P/E ratio is at historically low levels, I didn’t bet on that multiple increasing significantly over the next few years. Doing so is ultimately speculative. A company can, to some extent, control the earnings it produces, but not the price the market is willing to pay for them.

In my bull case model, I give myself a little more space to indulge my optimistic side. And so, for a bullish outlook, I bet that its valuation can converge toward more historically average levels, and if that proves true, that would, of course, be, well, very bullish, since it is, after all, the bull scenario.

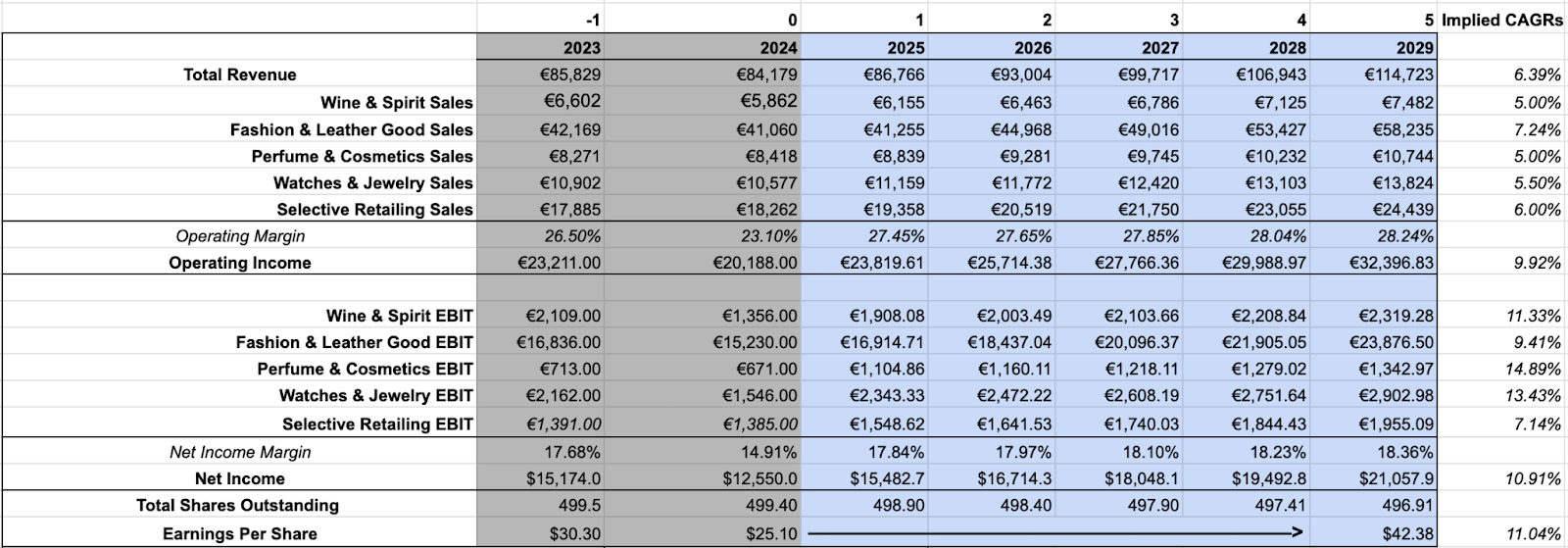

In that bull case, I also anticipate some moderation in sales growth, but it’s definitely higher than the base case and anticipates a total revenue CAGR of over 6% per year, which doesn’t sound crazy but is a good bit for a company of LVMH’s size. I also model out some more improvement in their operating profit margins for each segment, matching more closely what the average of the past 5 years has looked like.

Global luxury sales are somewhat cyclical, and 2024 was a low point coming out of a booming Pandemic period, so I imagine that their margins might, in the bull case, rise five percentage points from 23% in 2024 to 28% or so by 2029.

Bull Case Financials

There’s a lot of looking at what type of growth is precedented and what normalized profitability looks like, averaging out margins over several years.

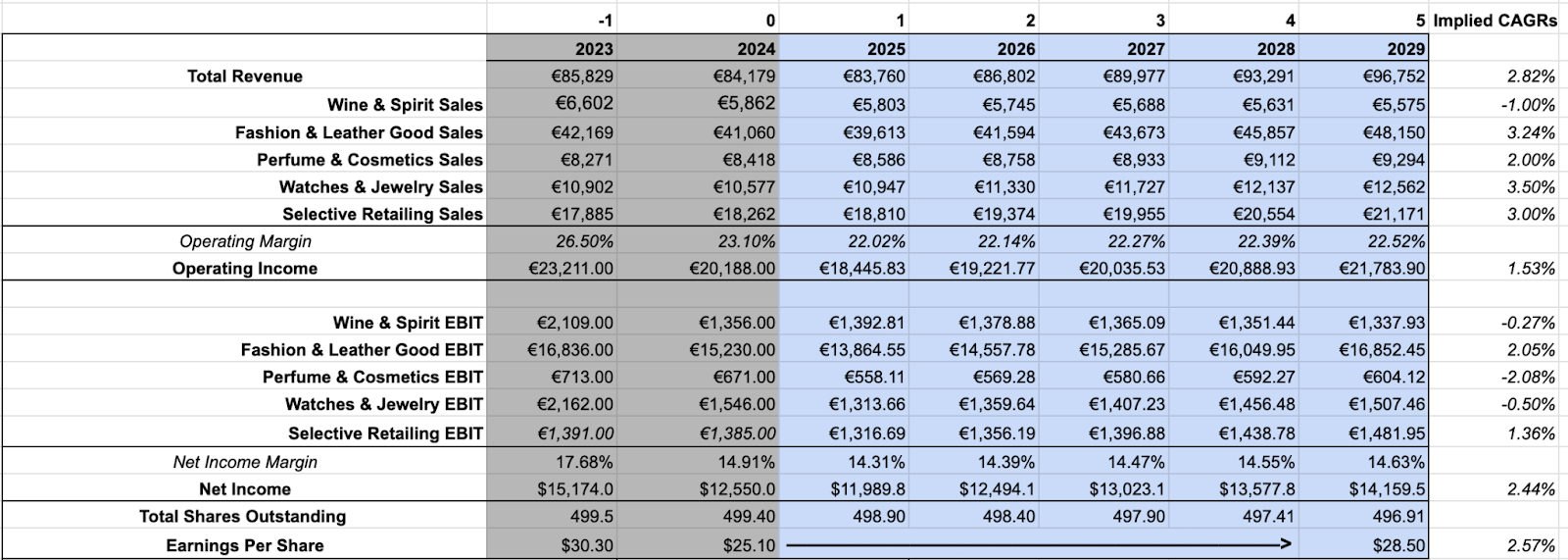

And in the bear case, shown below, I try to think through everything that could reasonably go wrong. Maybe some flat or declining sales that further reduce margins and also drive a lower valuation multiple, for example.

Bear Case Financials

And so, across these three scenarios, you can imagine I get very different price targets. In a base case, the stock starts to look attractive at about 400 euros per share, which is a 10-15% discount to current levels.

But in a bull case, which I should say, is not even the most aggressive bull case you’d find out there, the stock looks considerably undervalued, and at today’s prices, you could plausibly underwrite an estimated return of around 18-19% per year on paper.

Bull Case Range of Returns

I should emphasize, though, that this is the bull case, so it only takes up a small weighting in our overall price target calculation, as this is meant to reflect a world where everything goes right for them.

From there, I calculated the target buy prices for all three scenarios, and then gave a 60% weighting to the base case, since it’s what I view as approximately most likely, and then a 20% weighting to the bull and bear scenarios.

And when we do that, the blended price target is about 412 euros, which is the price that I estimate we’d need to be able to buy at to clear our hurdle rate of 12% annual returns, relative to the current market price of closer to 450 euros.

Final Thoughts

While I think LVMH is likely cheap on a relative basis, I have trouble getting as comfortable with the fundamental valuation, and it’s hard for me to see much organic growth for this business, plus they may be running out of attractive acquisition targets that move the needle, adding to their growth challenges. It’s the same issue at Berkshire.

I’ll be the first to say, though, I’m not an expert on luxury or fashion, which is in part why I can’t get as comfortable with this opportunity as I’d like. I’m sure there are readers who know far more about LVMH and can more confidently project higher rates of growth, but it’ll take me more time and research to get to that point.

The stock has gotten closer to being screamingly cheap since I first looked at it, but still not enough for me to wave away my concerns. So, Daniel and I agreed that this will probably not be the last luxury company we cover, and as we get more familiar with the industry, or if the stock falls dramatically, we may take a second look. And, of course, we’ll let you know if we do. For those interested, you can access our full valuation model on LVMH here.

In our podcast, we go even deeper on LVMH, exploring a backdoor way to invest in LVMH through Dior’s stock listing that may offer as much as a 20% discount. Listen to the episode here.

Weekly Update: The Intrinsic Value Portfolio

We started the year with 100% cash and have been slowly investing it

Notes

Evidently, no major changes this week. In fact, it’s been a few weeks since we’ve added anything to the Portfolio, reflecting how hard it is to find great opportunities at the moment. Looking back, our decision to “buy the dip” in April, in response to the initial tariff headlines, worked out well, but now, as the markets have rallied, most of our favorite stock ideas look less attractively valued to add to or initiate new positions in.

Last week, we did a more comprehensive review of our Portfolio, with updates on the companies we follow. If you missed it, you can read our mid-year Portfolio update here.

Quote of the Day

"A good product can last forever.”

— Bernard Arnault

What Else We’re Into

📺 WATCH: Jeff Bezos interview with 60 Minutes during the early days of Amazon

🎧 LISTEN: How Warren Buffett became Warren Buffett, with Kyle Grieve

📖 READ: Aswath Damodaran on the uncertain payoffs from alternative investments

You can also read our archive of past Intrinsic Value breakdowns, in case you’ve missed any, here — we’ve covered companies ranging from Alphabet to Airbnb, AutoZone, Nintendo, John Deere, Coupang, and more!

Your Thoughts

See you next time!

Enjoy reading this newsletter? Forward it to a friend.

Was this newsletter forwarded to you? Sign up here.

Use the promo code STOCKS15 at checkout for 15% off our popular course “How To Get Started With Stocks.”

Join the waitlist for our exclusive Intrinsic Value Community.

Follow us on Twitter.

Read our full archive of Intrinsic Value Breakdowns here

Keep an eye on your inbox for our newsletters on Sundays. If you have any feedback for us, simply respond to this email or message [email protected].

What did you think of today's newsletter?

All the best,

© The Investor's Podcast Network content is for educational purposes only. The calculators, videos, recommendations, and general investment ideas are not to be actioned with real money. Contact a professional and certified financial advisor before making any financial decisions. No one at The Investor's Podcast Network are professional money managers or financial advisors. The Investor’s Podcast Network and parent companies that own The Investor’s Podcast Network are not responsible for financial decisions made from using the materials provided in this email or on the website.