Imagine owning a toll road on one of the three major bridges connecting Canada with the U.S. via Michigan. Such a road would be a critical piece of infrastructure, linking the world’s biggest economy with its resource-rich neighbor to the north.

From a business perspective, once the bridge is built, the operations would be extremely profitable. Beyond some routine maintenance, there are hardly any marginal costs to be had, dropping incremental tolls down to the bottom line as almost entirely profit.

The toll-road business would also be blessed with stability and virtually guaranteed customers, given the demand for transiting back and forth between the countries and the lack of alternatives.

There wouldn’t be many ways to grow the business beyond raising prices, but it sure would spit off a ton of cash flows that could be invested elsewhere.

No, I don’t have a literal toll-road company to tell you about today; I actually have something much more powerful: a business that operates like the toll road I describe above, yet for the entire internet 👀

— Shawn

VRSN: The Internet’s Toll Road

Please allow me to introduce you to VeriSign, ticker: VRSN — a company that caught my attention over the last two months when Berkshire Hathaway became its largest shareholder after first investing in the business in 2012.

Warren Buffett doesn’t do “tech” stocks, but I think you’ll soon see that, despite the technical nature of its operations, VeriSign’s business model is much closer to his usual understandable, wide-moat picks than it first seems.

Toll Roads Are Miserable (Unless You Own Them)

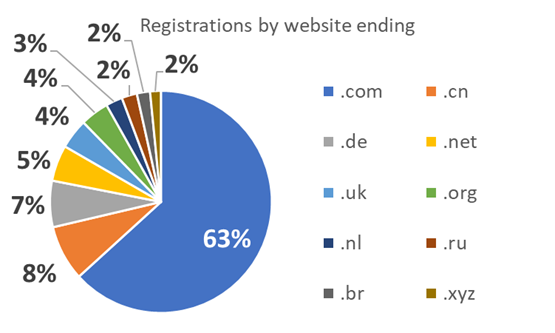

VeriSign is the ultimate toll road business, underpinning the infrastructure behind the modern internet. To grossly over-simplify things, VeriSign plays a critical role in the global internet’s functioning by acting as a “domain registry.” To venture away from the toll-road metaphor momentarily, managing domain registries as Verisign does is sort of also like overseeing an official phone book tracking the IP address and ownership details of every website domain ending with “.com” in the world.

Thanks to contracts with the Department of Commerce and the non-profit organization ICANN (I’ll spare you from spelling out ICANN’s acronym in full — it’s a marvel of bureaucratic jargon), VeriSign controls the registries for both the “.com.” and “.net” domains.

The .com domain is by far the most common and most valuable domain

Any website ending in .com must indirectly pay VeriSign $10.26 per year to continue making their website available to the public; otherwise, their web domain would be de-listed from the global registry system and become inaccessible. This is clearly a critical service provided by VeriSign, as their infrastructure quite literally enables trillions of dollars of commerce annually on the internet and billions of search queries to happen.

In other words, without VeriSign’s services, most of the internet’s websites would become unusable. Now, I’m overstating slightly because if VeriSign dropped off the face of the Earth tomorrow, regulators would eventually find another entity to fulfill registry services for .com domains, but on a day-to-day basis, they’re a critical node in a network that ensures we can access the right websites when we type a domain into our computer’s search bar.

With Power Comes Diminished Returns

This tremendous power isn’t without cost, though. VeriSign is only permitted to raise prices for its .com domain (the Golden Goose of its business) by 7% per year in the last 4 years out of every 6-year period.

This is defined explicitly in its contract with ICANN, but on the bright side, VeriSign gets to hold its monopoly over the .com domain for six years at a time. Then, the contract automatically renews again, restoring VeriSign’s monopoly for another six years. Short of some catastrophic technical failure on VeriSign’s end that violates its commitments to neutrally keeping the internet working without hiccups, there’s no reason to think this monopoly-granting contract won’t be renewed.

There’s too much at stake if a transition of oversight for the .com domain registry is botched, and in 25 years of overseeing the .com domain, VeriSign has had “100% uptime” with zero significant issues from either internal glitches or cyber-attacks.

Ample Profits

Thanks to this powerful regulated monopoly structure, VeriSign has consistently earned a 55% free cash flow margin over the last decade and boasts the fifth-highest net profit margin in the S&P 500, tied with Nvidia — not a bad peer to have.

The business model is quite simple. VeriSign oversees a network of privately run data centers that distribute its risks and add redundancies, ensuring that the domain registry system and the internet continue operating smoothly in conjunction with ICANN and other groups.

For VeriSign’s part, as mentioned, it oversees a giant phone book, tracking who owns which web domains, such as “theinvestorspodcast.com.”

ICANN references this domain registry and oversees a network (aka the Domain Name System or “DNS”) that connects an IP address to these domains so that we can type in a website in English (or any language), and then that can be converted into a computer-readable address, allowing your browser to locate and connect you to the correct website.

So long as the number of websites ending in .com is growing, so is VeriSign’s business.

Estimating the company’s revenues is as simple as multiplying the number of domains registered by VeriSign by the rate they charge — i.e., $10.26 for .com domains (the vast majority of their sales.)

Like the toll road I described, where the operations are hugely profitable after the initial infrastructure is built out, the same is true for VeriSign. Their data centers have been acquired over nearly three decades, and now, there aren’t many major expenses left to be had. Sure, there are employee costs and routine maintenance, but no new sizable capital expenditures are needed to keep things running.

Correspondingly, VeriSign touts an eye-watering 55% free cash flow margin that has remained steady for at least the last decade, meaning that 55 cents from every dollar of revenue becomes free cash flow.

There are essentially no investments being made into large growth projects because regulators aren’t keen to let them expand their monopoly further into other domains or to try and vertically integrate by, say, building a domain registrar business like GoDaddy’s that’s focused on selling domains to end customers. (VeriSign’s customers are the domain registrars, not the website publishers.)

It just spits off cash flows, and then those cash flows are returned to shareholders through share repurchases:

VeriSign puts most, if not all, of its free cash flows toward repurchasing stock

Looking For A Domain?

Let’s go through an example to make this all more tangible, though let me just say that it can be a little confusing. Feel free to skip to the following section if your head starts to spin:

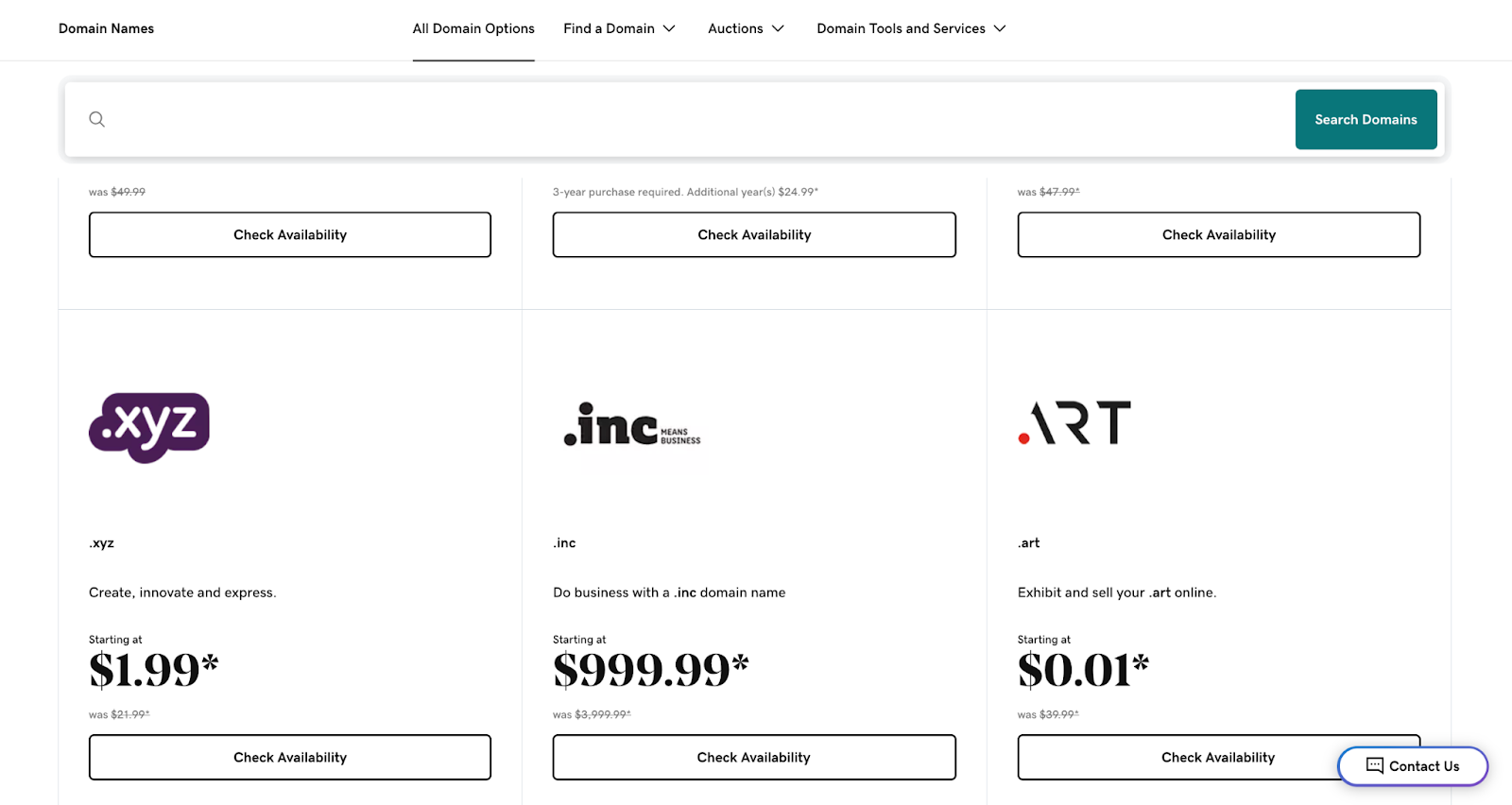

To register your own web address, start by choosing a domain name and checking its availability using a domain registrar, such as GoDaddy, Squarespace, or Wix. If the domain is available, you can purchase and register it by filling out a form with the domain name and your personal information.

GoDaddy’s website for selling domains to website publishers

For domains ending in .com, your registrar communicates with VeriSign to record your domain in the authoritative .com database. The registrar acts as the intermediary, handling availability checks and registration processes, while VeriSign manages the official database of .com domains. (Note that the process would be the same with a different company than VeriSign for other domain endings, like .xyz, .shop, .org, and hundreds more.)

After registration, you'll need to configure DNS records through your registrar or hosting provider, connecting your domain name to the IP address of the server hosting your website.

Once your domain is registered and DNS settings are correctly configured, anyone can access your website by typing your domain name into a browser.

The simple takeaway is that domains are sold via registrars like GoDaddy, making VeriSign dependent on them for new domain registrations. The .com domain is the bread-and-butter of the domain world, and by overseeing registries for it, VeriSign is an essential intermediary.

What’s Happening With The Business

The catch here is that, in recent years, the number of domains has slowly declined.

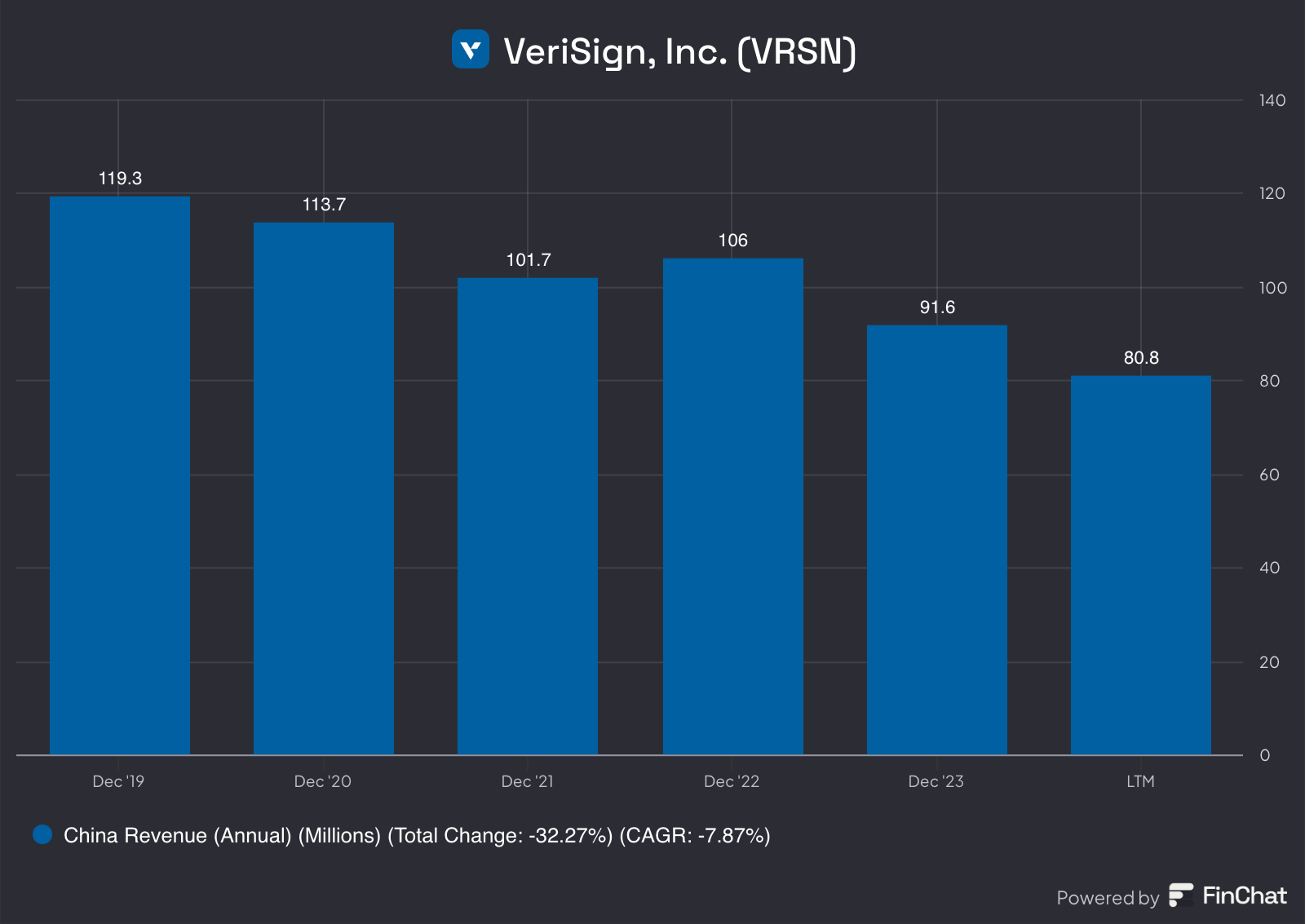

In part, that’s because Covid pulled forward the number of web domains being created (people were at home with time to play around with launching websites and new businesses) and also because of headwinds from China, where the government has made it more difficult for citizens to acquire and register domains, basically leading to fewer Chinese websites.

Chinese revenue for VeriSign

However, VeriSign’s revenues have continued to grow in the low-to-mid single digits, thanks to contractually permitted price hikes that offset marginal declines in total domain registration. If the number of registered domains falls 1% but prices for the remaining domains rise 4%, overall revenues still grow ~3%.

With its contracts for controlling the .com and .net domains recently renewed, VeriSign has once again (predictably) extended its monopoly, but it’s in a two-year window where it cannot raise prices. Starting in 2027, it can raise prices for .com domains by 7% per year through 2030, when the contracts are up for renewal again and sooner for .net domains, with a price cap of 10% per year.

In a nutshell, VeriSign is a toll road for the internet, a company that collects fees from the mere existence of websites with a ton of corresponding operating leverage. Incremental revenues almost entirely drop to the bottom line. But it’s not the 1990s anymore, and the domain registry business isn’t exactly booming — it’s a very mature, possibly structurally declining industry.

Number of registered websites with VeriSign has declined in recent quarters

Decline Isn’t All Bad

That said, VeriSign is managing that quite well, allocating almost all of its free cash flows each year to share buybacks, while raising prices, on average, well in excess of the percentage declines in domains we’ve seen in the past few years. As such, assuming the company takes advantage of the price hikes it’s legally allowed to do in the coming years, even with a continued decline in the total number of .com/.net domain registrations and while also continuing to buyback around 3% of its shares each year, I see a business with very high odds of growing free cash flow per share by 8% per year through 2030.

Assumes a 3% decline in shares outstanding, price hikes of around 7% starting in 2027, and a decline in total domains of -1% per year. Still equals roughly an 8% expected return from current prices

Assuming that we are through the worst of the Chinese-domain headwinds, returns could easily be in the double digits.

On a risk-adjusted basis, I see this opportunity as being fairly attractive. 29x earnings for a business with little real growth isn’t cheap, though.

Concerns & More Valuation

The most practical risk is that domain registrations fall off more than expected, especially given the effects of generative AI. If many searches can be replaced by chatbot queries or AI summaries, there may be structurally less need for as many websites, leading to a rapid falloff in domain registrations. This has yet to come to fruition and is another perspective on the same question at the center of Alphabet’s valuation: How will generative AI impact search?

A related concern is the rise of alternative domains, slowly eating into .com’s market share. There are more options than ever to put at the end of your website, with a vast range of prices and connotations. The prestigious .inc domain can cost as much as $1,000 per year, while domains like .xyz are cheaper but trendier and popular with tech startups.

Domains are a subtle but important part of branding, and while the .com domain is Ol’ Reliable, new website publishers may want to use something more unique, communicating more nuanced messaging to visitors.

Or, increasingly, businesses and publishers may not have websites at all, relying only on an app or social media presence.

Fortunately, if any of these prove to be lasting issues, regulators might permit VeriSign to eventually raise prices as needed to offset mounting domain losses.

After all, even if VeriSign doubled its prices, $20 per year is a fairly inconsequential cost relative to the value of having a website. Put differently, while this is entirely speculative, there’s a scenario where VeriSign could remain quite profitable, even if generative AI leads to fewer and fewer websites simply by raising registry fees for remaining domains.

Looking at my model for VeriSign, which you can download for free here (Hit “File” and then “Download” to save to your computer for edits.)

My fair value for the stock is around $230, where the implied return (based on growth in free cash flow per share) comes out to about 8% — a modest premium to the current long-term borrowing rate for investment-grade corporate bonds, reflecting that VeriSign’s earnings quality is about as close to a corporate bond as it gets in public equity markets.

If we’re going to treat VeriSign as something that nearly resembles a corporate bond, given the near certainty of its sales and profitability over the next 5 years, we also have to consider that price matters hugely, more so than in most other potential stock investments. Unlike, say, Alphabet, where a price target can be flexible since the company’s growth can easily bail you out when overpaying, the same isn’t true with VeriSign (or corporate bonds, for that matter.)

A modestly lower price paid can be the difference between earning 8% a year and 10% or even 12% per year.

With VeriSign, to earn the sort of double-digit annual returns that I look for in stocks, the stock would have to be priced below $200 per share and, more preferably, below $190 per share, according to my calculations.

As such, I intend to be very strict with these targets. Assuming there isn’t an unexpectedly dramatic falloff in domain registration, I want to try and accumulate a small position in VeriSign — 5% or less — if I can snap up shares below $190. And at that price, I feel confident I can earn a 10-12% return or, in a more pessimistic scenario, still receive a tolerable 6-8% annual return.

Conclusion

With that said, that’s all I have for today, folks. I hope you enjoyed learning a bit about VeriSign and internet infrastructure. Don’t be surprised if VeriSign isn’t added to the portfolio any time soon, or at all, if I can’t get an acceptable price that offers a sufficiently attractive expected return and margin of safety relative to my fair value estimate.

If you enjoy these write-ups, please forward them to a friend, and for more on the business and risks facing VeriSign, I’d encourage you to check out my roughly hour-long podcast on the company here. See you again next week with another intrinsic-value breakdown.

Weekly Update: The Intrinsic Value Portfolio

Notes

AutoZone remains above my price target, so it hasn’t been added to the portfolio

No changes to the portfolio this week. Alphabet and Ulta continue to be a bit depressed, but I’ve already used that as a chance to lower my average price. I’m hoping to find some fresh investments to further diversify into

Quote of the Day

"For the investor, a too-high purchase price for the stock of an excellent company can undo the effects of a subsequent decade of favorable business developments."

— Warren Buffett, on how corporate earnings are similar to bond coupons

What Else I’m Into

📺 WATCH: Can Japanese automakers survive the threat from Chinese EVs?

🎧 LISTEN: William Green interviews “Billionaire Brit” Terry Smith

📖 READ: Eddie Elfenbein’s 2025 Buy List of stocks

Your Thoughts

Readers’ feedback from last week on AutoZone:

“One item that is not discussed (the elephant in the room) is the potential impact of tariffs. It could impact new car prices and parts. The questions are: what will be the tariffs, when will they apply, on what and whether they will be able to pass on the higher prices to consumers without eating their margins? Notwithstanding the questions above, the immediate impact of tariffs is uncertainty which is a dirty word for investors.”

“Agree with waiting for a dip and not buying at current levels.”

“The real trick is to find a company like Autozone back in 1998. A company who is starting to buyback shares consistently! Another great analysis!”

“Thank you very much! Even when I'm inundated with emails, I look forward to seeing what you write. Maybe you'll write about some interesting small-cap company?”

See you next time!

Enjoy reading this newsletter? Forward it to a friend.

Was this newsletter forwarded to you? Sign up here.

Use the promo code STOCKS15 at checkout for 15% off our popular course “How To Get Started With Stocks.”

Follow us on Twitter.

Keep an eye on your inbox for our newsletters on Sundays. If you have any feedback for us, simply respond to this email or message [email protected].

What did you think of today's newsletter?

All the best,

© The Investor's Podcast Network content is for educational purposes only. The calculators, videos, recommendations, and general investment ideas are not to be actioned with real money. Contact a professional and certified financial advisor before making any financial decisions. No one at The Investor's Podcast Network are professional money managers or financial advisors. The Investor’s Podcast Network and parent companies that own The Investor’s Podcast Network are not responsible for financial decisions made from using the materials provided in this email or on the website.