Conscious Capitalism goes back decades, most notably to Whole Foods co-founder John Mackey. Mackey has long championed the idea that business is about much more than just creating “value” for shareholders. To zealots of Conscious Capitalism, profits are a natural byproduct of a company succeeding at its mission, but there’s nothing noble in pursuing profit without a greater purpose.

Whole Foods’ business triumphs and success in staying true to its mission of providing whole, healthful foods to communities even after being acquired by the embodiment of capitalism in perhaps its most pure form — Amazon, is a testament to the movement’s legacy, which has been well-intended but at times fanciful.

Another company is now bringing Conscious Capitalism to public markets, again showing that putting ethical business and sustainability first isn’t just ESG gibberish but an actually winning strategy underpinning one of the most impressive brands in the world.

That company is Vital Farms, ticker: VITL. It was founded by Matt O’Hayer, who, after befriending Mackey back in 1984, understands Conscious Capitalism better than almost anyone.

Today, I want to estimate the intrinsic value of this popular producer of pasture-raised eggs to see if there’s an “egg-cellent” investment opportunity at hand 🍳

— Shawn

Vital Farms: The Booming Ethical Food Biz

I’m as skeptical as anyone that a business premised around Conscious Capitalism can be a good investment, where management is tasked to consider what’s best for all stakeholders in their decisions, including employees and the environment. Either a business is being run in the best interest of shareholders, or it’s not, and the consequences of that managerial philosophy can lead to vastly different outcomes for otherwise profitable companies.

Unfortunately, in many cases, the interests of shareholders do not perfectly align with the lip service management pays to virtuous goals around employee and ecological welfare, except in the rare case where a brand’s success with customers is truly tied to its ethics.

In such cases, it is actually a risk for the company not to conduct itself at a higher ethical standard than is common throughout the corporate world. Vital Farms is one of these companies, where shoppers happily pay 2-3x the regular price of eggs for a product they believe treats animals more humanely, has a more limited environmental footprint, rewards farmers for more sustainable practices, and correspondingly tastes better or is healthier.

Bullsh*t-Free Food

But someone only shells out $10 for a carton of eggs if they genuinely believe it’s “bullsh*t-free,” as the Vital Farms motto goes. Correspondingly, an essential part of the Vital Farms branding is using their packaging and marketing to convince shoppers that they really do what they say they do — something that is depressingly uncommon in the natural foods world.

Product labels like cage-free, pasture-raised, grass-fed, and even organic are all too easily exploited as an easy way to charge higher prices by some food brands, to an extent that often leaves customers willing to dig beneath the surface disappointed by just how loosely these labels can be used and how there isn’t as much regulation around them as you might think.

Yet, one thing is clear: People genuinely want to know where their food comes from. They want to feel good about how animals and crops are raised, and they want to feed their families nutritious meals from animals that haven’t been stuffed with antibiotics, given feed chock-full of pesticides, or raised in sickly conditions in a factory.

Via the non-profit Farm Forward

That seemingly low bar for food production is one that most food brands hardly come close to clearing, which is why grocery shoppers across the USA have become fiercely loyal to Vital Farms, a brand that has blossomed by meeting ethical food-production standards agreeable to the broader public at scale.

With an 80%+ share of the country’s niche pasture-raised egg market by the end of 2023, Vital Farms has taken grocery stores by storm. These colorfully packaged and folksy eggs aren’t just at Whole Foods; they’re everywhere, from Food Lion to Publix and Kroger, with distribution at over 24,000 retailers.

And people love them, so much so that 36% of Vital Farms customers reportedly will choose to leave the store empty-handed without eggs if Vital Farms is sold out (which is a common problem due to the brand’s surging popularity), opting to go without or visit another store instead of trading down to brands they perceived as lower quality and less ethical.

Eggs are supposed to be a commodity, but Vital Farms’ devotees couldn’t feel more differently — they see a brand so committed to traceability that every carton tells you the name of the farm where the eggs came from, with a website allowing you to virtually explore and learn more about said farm.

Boosted by its B Corp status and third-party credentials like the Non-GMO Project and Certified Humane, along with guarantees that all hens can access at least 108 square feet of outdoor space on rotating pastures (minimizing damage to specific plots) and snazzy marketing — like the Vital Times newspaper cutout in every carton that tells stories about the hens and farmers and even declares a “Bird of the Month” — the company has put on a masterclass in marketing and PR.

A Strong Brand Is Good For Business

Since 2017, Vital Farms has grown revenues by 34% per year, and after first turning profitable in 2018, net income has risen 10-fold.

Given the premium pricing for their eggs, Vital Farms boasts a gross profit margin that’s nine percentage points higher than their peer, Cal-Maine Foods, producer of Egg-Land’s Best.

With a network of 375 family farms held to the highest standards in the industry (and plans to add another 250), and a processing station that can pack 6 million eggs a day, Vital Farms is scaling at a pace that might not have seemed possible just a few years ago, given that this company was humbly founded on a single farm in Austin, Texas in 2007 with just 27 hens.

What’s most impressive is that as the brand has gone nationwide and as retailers offer more variations of Vital Farms products, sales volumes have only risen further. Typically, as consumer packaged goods brands become more readily available in different sizes and flavors, there’s a degree of cannibalization where individual SKUs (stock-keeping units) see a slowdown, but that largely hasn’t happened for Vital Farms.

After discovering Vital Farms, customers seemingly buy in quickly and increase their purchases of their products over time. For example, perhaps they buy eggs weekly, but initially, they treat themselves to Vital Farms only once a month. After a few months or years, the number of times per month they purchase Vital Farms tends to rise until, at least for a chunk of customers, they almost exclusively purchase Vital Farms’ eggs.

This is a story where branding is everything. Otherwise, no one would voluntarily pay more than twice the national average for a 12-count carton of eggs. In the podcast I did about the company, I get into allegations of greenwashing and related lawsuits, but I’ll spare you from that drama here.

After spending dozens of hours researching the company, my personal conclusion is that Vital Farms is, unsurprisingly, not perfect, but their efforts are legitimate, even if some things are misleading.

For example, hens having “access” to the outdoors doesn’t mean they spend all day foraging in the woods. Instead, they almost certainly have limited time to do so and spend most of their time in barns. And the company’s signature deep orange yolk coloring isn’t solely because their hens are happier and healthier; it’s largely due to adding marigolds and paprika to their feed, which Vital Farms does openly acknowledge on its website.

A deep orange yolk is what makes Vital Farms so special to some shoppers

It’s really a question of expectations. If you have romantic ideas of some Hen Heaven, you will be disappointed, but their practices are likely considerably more humane and environmentally mindful than most other commercially available brands, even those that similarly claim to be pasture-raised.

And whether you personally buy into $10 ethical eggs doesn’t really matter. The question is whether other people do, and if so, is that belief premised on a solid foundation, or is the brand’s reputation one exposé away from crashing and burning?

Again, I believe the former, but whether you think the company deserves its customers’ trust is critical to any long-term bullish thesis.

More Than An Egg To Crack

Vital Farms offers 23 different SKUs, with their conventional pasture-raised eggs in 6, 12, and 18-count cartons in medium, large, XL, and jumbo sizes. They also upsell these core products with organic versions and even a “restorative” set of egg products with the highest environmental impact standards.

Additionally, they offer heirloom True Blue eggs that are, well, blue, owing to the specific types of Azur hens that produce them. Plus, they produce liquid egg cartons, packaged boiled eggs, and a range of artisanal grass-fed, hand-churned butter with and without sea salt.

A sampling of VITL products

Could they continue to expand into other categories? Maybe. This is just speculation, but I’m sure they could eventually expand into cheese and yogurt since they’ve started producing butter. For now, though, the focus continues to be on capturing some of the untapped potential they still see in the egg market.

What’s An Egg Business Worth?

There’s a lot to like about Vital Farms as a brand. Heck, I’m a consumer of their products myself and a satisfied one, too. But how does that translate into value for shareholders?

In 2024, the stock rose to the tune of more than 140%, so the company’s shares are coming off a banner year.

With a price-to-earnings ratio north of 34, Vital Farms is by no means cheaply priced, though that’s not surprising given its track record of growth and expectations for further growth.

The seemingly high valuation, alongside speculation that the brand’s margins or sales volumes will fall off either as shoppers become more financially constrained or as new competitors challenge their market share, has made the company a ripe target for short sellers betting against the stock. At the time of writing, nearly 30% of the company’s shares have been sold short, making it one of the most heavily shorted stocks anywhere in markets.

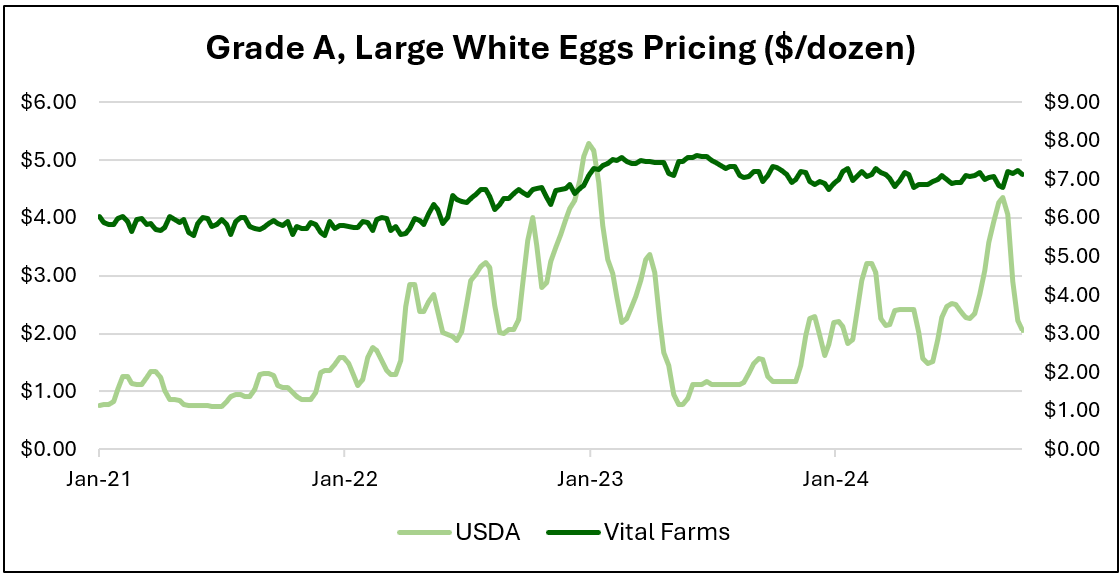

Two years ago, when regular egg prices had been driven so high by Bird Flu outbreaks (resulting in millions of chickens being culled), it might have only cost an extra dollar to trade up to Vital Farms. And if you have to pay an elevated price for even the cheapest eggs, you might as well pay a little more for something more ethical, right?

Short sellers noticed this and thought the boost to Vital Farms’ business was only temporary, set to fall off when egg prices normalized.

It was certainly valid to wonder whether shoppers would remain loyal to VITL as regular egg prices came down and the premium price spread for Vital Farms’ eggs rose.

To jump to the punchline: They did stay loyal (if they hadn’t, we wouldn’t be talking about the company today.) No noticeable trading down occurred, which is why I remain puzzled at why the short interest in this company is so high.

Not only have customers not fled the brand as its eggs have become more relatively expensive, but they’re increasing their purchases of the company’s eggs on average, showcasing that Vital Farms does have lasting customer loyalty and pricing power.

From my perspective, the resilience of Vital Farms in the last 12 months should have been enough to convince short sellers to back away from the stock, but it continues to be heavily sold short, presumably because Wall Street sees this as a fad similar to Beyond Meat, where customers will stop paying double-digit egg prices once they wake up one day and realize it’s not worthwhile to do so.

That day could come. However, I don’t think Vital Farms is entirely a fad.

I agree with the notion that our society increasingly cares about animal welfare, nutrition, and environmental sustainability, and I think Vital Farms’ success is very much a product of those shifting values, especially as so many other brands fall short of those values in practice or fail to convince customers of those values with their marketing.

I also have concerns. A lot of concerns. Will folks opt for cheaper brands of premium eggs that are just cage-free rather than pasture-raised during a recession? And how easily can a competitor challenge Vital Farms with savvy marketing and build up their own network of family farms? (Or perhaps, what if a competitor comes in and offers to pay farmers even more to work with them exclusively?)

In other words, does Vital Farms have a lasting moat? I’m not sure, and it could be too early to say.

Valuation

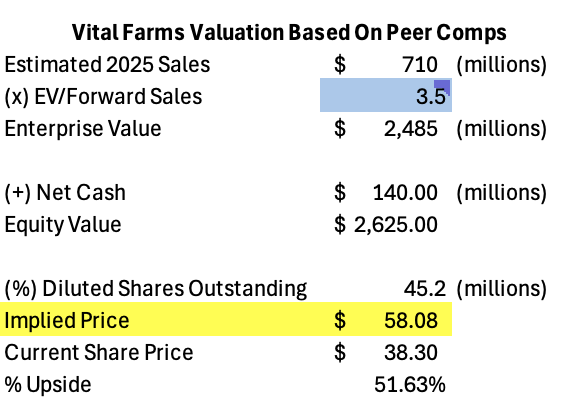

Still, I want to estimate what the company is worth. In my podcast episode on Vital Farms, I looked at the company’s enterprise value as a multiple of its sales, which has risen over the last year but is modest compared with a number of other fast-growing, pure-play consumer packaged goods brands like Freshpet, Monster, and Celsius.

Vital Farms has grown faster and is expected to grow faster than its peers, yet trades at the lowest ratio of enterprise value to sales

So modest, in fact, its EV/sales ratio is about one-half to one-third of these peer companies who are growing roughly as fast or slower than Vital Farms. Here’s a spreadsheet I put together showing the peer comps — you can experiment with increasing the EV/Sales ratio for Vital Farms, and it’ll spit out a target price and implied upside depending on what you think is comparatively appropriate.

This valuation approach is known as “relative pricing” (as opposed to a DCF), looking at valuation metrics the market has used for similar companies to assess whether your company of interest is fairly valued.

But this isn’t the only and certainly not the best way to value a company.

Here in the newsletter, I want to take another swing at the company’s valuation from a different perspective. For starters, while the multiple of sales investors are willing to pay for a company says something about its expected growth and profitability, it doesn’t tell you everything.

So, while you could say that Vital Farms’ EV/sales ratio should converge toward brands like Celsius and Freshpet, which would mean the stock price rising by 50% or even more than doubling, this would also imply the stock’s price-to-earnings ratio rising to an eye-watering level of 70.

With enough growth in earnings, a P/E of 70 could be justified, but I don’t want to base a thesis for a company around its P/E rising from 35 to 70.

Analysts are estimating that over the next two years, though, Vital Farms can grow its EBIT (earnings before interest & taxes) — a proxy for operating profits, from $58 million to ~$92 million (26% CAGR), which is compelling.

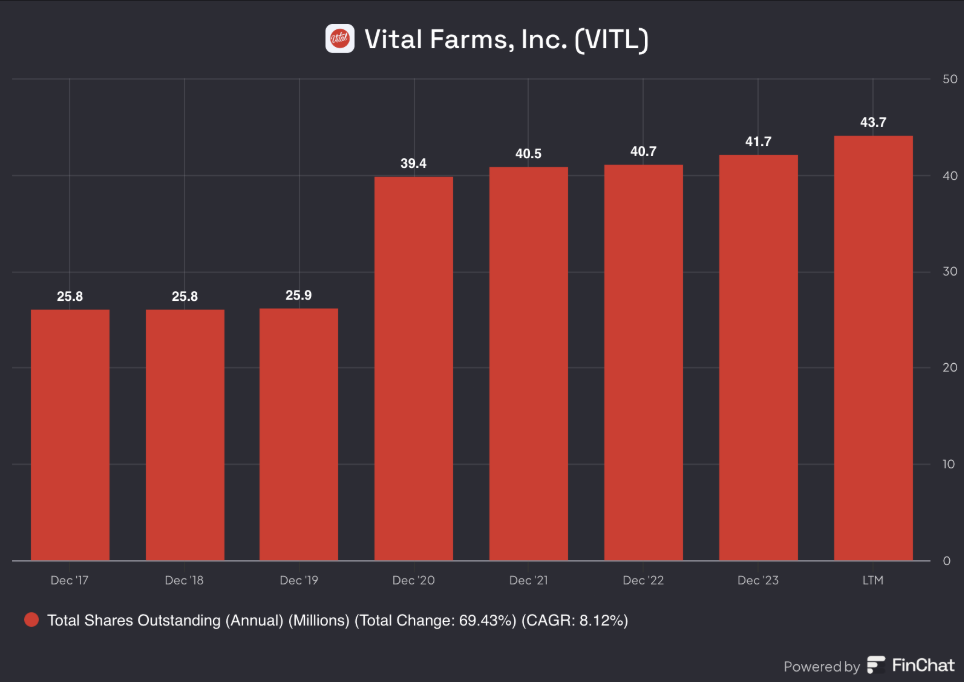

You’d expect similarly impressive growth in earnings per share, except Vital Farms has been compensating its employees and management aggressively with stock, increasing shares outstanding by 8% per year on average. If earnings are flat, earnings per share will decrease as more shares are created out of thin air, so this is a considerable headwind for returns.

This also assumes that Vital Farms can stay as profitable as it was in 2024, which is no guarantee — a 10%+ operating profit margin is an outlier compared to its results in past years of: 2.4% in 2019, 5.7% in 2020, 0% in 2021, 1.2% in 2022, and 7% in 2023.

That volatility in profit margins and growth in shares outstanding makes me think that, even if Vital Farms can continue growing revenue at 25-30% per year, earnings per share are unlikely to grow in the same proportion. And should there be a recession, I’d think Vital Farms’ revenues would be very vulnerable.

As a result of all this, I’ll say that I wouldn’t be surprised at all if this company does generate 20%+ returns per year over the next few years, assuming it can keep growing, maintain its 2024 margins, and slow down its rate of stock dilution, but those are some optimistic assumptions that I don’t think I could sleep easily at night with.

Portfolio Decision

So, I’m passing on Vital Farms, even though I love the brand and loved learning more about it. I think they’re doing something really special, and I wouldn’t want to bet against them at all. I’d be inclined to bet on them if I had to, but the wonderful thing about investing is you don’t have to do anything.

I will miss out on some of the biggest gains to be had as I wait to see whether they can scale profitably, whether they can endure an economic slowdown where people have less disposable income, and whether they can continue to devour market share but I will also dodge massive losses if things move against the company, too.

In short, I want to see the business mature a bit further before I put my capital on the line, but I don’t blame anyone for having the conviction to bet boldly on them today — as I’ve said, there are many things to like about the company.

I’m afraid that since I think so highly of what they do from a consumer standpoint, there’s a part of me that wants to like the company as an investor. It has taken some discipline for me not to start buying shares in it, and in part, that boils down to me being bothered by how aggressively they issue stock, as well as a realization that the company’s profit margins aren’t as impressive as I would’ve hoped, which does make sense given all of the extra overhead cost that goes into the quality and transparency of their products.

I also want to better understand the company's relationships with farmers — how “special” and durable are those relationships, and how easy is it to recreate not only the network of family farms that they have but also their trust with consumers? My gut says these are hard to recreate, but I’m not confident in it.

Let me know what you think in the poll at the bottom of this newsletter, and please leave a comment to expand on your answer! Listen to the rest of my breakdown of Vital Farms here.

I’ll be back again next week, breaking down another compelling business and looking for opportunities to add high-quality stocks to The Intrinsic Value Portfolio, but keep reading below for important portfolio updates.

Weekly Update: The Intrinsic Value Portfolio

Used selloff to build a position in Alphabet and increase stake in Ulta

Notes

Alphabet’s stock sold off roughly 10% after reporting earnings last Tuesday, allowing me to build a 4.5% stake at an average price of $188 per share

I’m hoping to add to the position in Alphabet further, making it up to a 5-7% holding, if there’s continued weakness in its share prices

Ulta’s stock sold off a bit down to $380 per share, which I used as a chance to increase my stake from 5% to 6% and lower my average cost to $402 per share

Slowly but surely, we’re building the portfolio, yet there’s still a lot of cash to allocate!

This is what readers had to say about Alphabet last week:

“Yes, with caveats: a) monopoly - great while it lasts but won't last forever for two main reasons. The government is already after them and will continue, likely split these individual parts into forced spinoffs yet can foresee a Standard Oil process and outcome. Second reason is it seems easy to see a future where AI is dominant in search. Gemini is trailing behind others, much like Explorer did during the internet's infancy and formative years (Yahoo, Ask Jeeves, etc). Advertisers will fish where the fish are. Buying below fair value where ideally growth rates stay high or moderately decrease given, as shown, about 70% is ad revenues. Gradually, then suddenly... Blockbuster to Netflix... Netscape Navigator to Explorer to Yahoo to Google...”

“I love Alphabet's products and I like that they have a lot of optionality. However, regulatory risks always give me pause and I think entry on this stock requires quite a margin of safety to cover for any aspect of the thesis being disrupted.”

“‘Ask Mr. Chat’ is my new everyday search engine. And a lot of people I know are starting to use those more and more. Certainly, I am a software engineer, but once you start using LLMs, Google is losing you…It's just so much nicer to ask a specific question and get a specific answer. I think Google is losing its moat more and more and now has lots of competition.”

“It will be interesting to see if Alphabet is forced to break up. But I am with you on starting to buy it at values under $180. Thanks Shawn.”

Quote of the Day

"When I stopped looking for the payoff — the big bucks, that’s when I had the biggest success.”

— Matt O’Hayer, Vital Farms’ founder, reflects on being a serial entrepreneur

What Else I’m Into

📺 WATCH: Aswath Damodaran on how DeepSeek crashed the “AI Party”

🎧 LISTEN: Listen to the Q1 Mastermind episode on We Study Billionaires with myself, Stig Brodersen, and Tobias Carlisle

📖 READ: Tariffs, explained

Your Thoughts

See you next time!

Enjoy reading this newsletter? Forward it to a friend.

Was this newsletter forwarded to you? Sign up here.

Use the promo code STOCKS15 at checkout for 15% off our popular course “How To Get Started With Stocks.”

Follow us on Twitter.

Keep an eye on your inbox for our newsletters on Sundays. If you have any feedback for us, simply respond to this email or message [email protected].

What did you think of today's newsletter?

All the best,

© The Investor's Podcast Network content is for educational purposes only. The calculators, videos, recommendations, and general investment ideas are not to be actioned with real money. Contact a professional and certified financial advisor before making any financial decisions. No one at The Investor's Podcast Network are professional money managers or financial advisors. The Investor’s Podcast Network and parent companies that own The Investor’s Podcast Network are not responsible for financial decisions made from using the materials provided in this email or on the website.