By Matthew Gutierrez and Shawn O’Malley

Another day, another all-time high for stocks.

Meanwhile, natural comparisons between Cisco’s 1990s run and Nvidia’s rally over the past few years are taking shape.

Cisco erupted for a 3,590% stock surge until its peak in March 2000. As market strategist Charlie Bilello notes, in the five years into its peak, Cisco’s price-to-sales ratio moved from 7x to 39x, and it briefly became the world’s largest company.

In the five years before its June 2024 peak, Nvidia’s price-to-sales ratio moved from 9x to 42x, and it briefly became the world’s largest company, too.

Which company did each briefly pass? Microsoft.

— Matthew & Shawn

Here’s today’s rundown:

Today, we'll discuss the biggest stories in markets:

Investors can’t stop talking about geopolitics

Why aren’t stock pickers doing better?

This, and more, in just 5 minutes to read.

POP QUIZ

Chart(s) of the Day

Sponsored Content

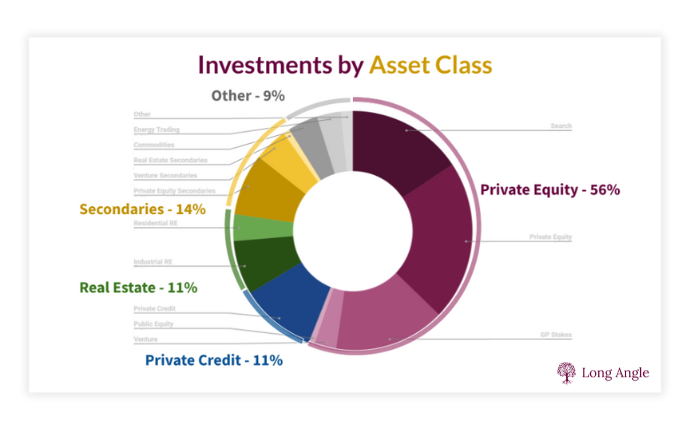

Private Markets, Powered by Collective Expertise of HNW Investors

Investing in private market opportunities is challenging. The difference between success and failure in private markets comes down to your network.

Long Angle is a vetted community of 3,000 high-net-worth investors who leverage their collective expertise and scale to access and underwrite some of the world’s best alternative asset investments.

After reviewing hundreds of opportunities, Long Angle diligence deal teams greenlight a dozen deals each year. Asset classes range from Private Equity, Search Funds, and Private Credit to Secondaries, Real Estate, and Venture.

No membership fees. All members receive equal access to negotiated fee discounts powered by the community’s $45 billion in collective assets.

In The News

🌍 Investors Can’t Stop Thinking About Geopolitics

Politics, politics, politics. Investors just can’t stop talking about a seemingly destabilizing shift in the geopolitical status quo in recent years.

Obsessed much? This year, the topic has consumed a number of high-profile business events. In February, former U.S. Secretary of State Mike Pompeo told an audience of investors, which included Blackstone’s CEO and the head of Saudi Arabia’s $900 billion+ sovereign wealth fund, that it has become “impossible to separate geopolitical risk from capital allocation,” reports the FT.

Similar opinions have been shared at events hosted by JPMorgan for corporate bond investors, the Milken Institute Conference, and gatherings of those in the futures and derivatives industry. Many of these meetings have similarly featured former U.S. government officials, generals, and historians lecturing financial professionals on the importance of preparing for a more conflicted world.

The last few weeks have offered no shortage of political volatility to validate these concerns, from the drama of the Biden-Trump debate to electoral change-ups in France and the UK to the ongoing saber-rattling in the South China Sea, Houthi attacks on ships in the Red Sea, U.S. commitments to longer-term support of Ukraine against Russia, and so on.

The idea that the world isn’t just enduring a temporary bout of instability is gaining wider acceptance, too, with some embracing the notion that this may be a structural shift with long-term impacts for investors.

While pockets of instability are well-tolerated by financial markets, an increase in such shocks, especially in usually stable democracies, “represent a sea change,” writes the FT.

Narratives vs. Reality: Such narratives aren’t entirely new, and ultimately, they are narratives. In practice, it’s less clear that investors are structurally discounting a paradigm shift in global stability. Yes, gold is up over 70% in the past 5 years in U.S. dollar terms (even more in other major currencies), but the stock market is at all-time highs, volatility indexes are at multi-year lows, and oil prices have traded in a narrow range for the last 12 months.

Companies like Nvidia and TSMC, which are firmly in the crosshairs of a U.S.-China conflict, have risen 163.27% and 80.59%, respectively, this year. And rising yields on U.S. Treasury bonds have had more to do with delayed expectations for Fed rate cuts than with fears of exploding deficits.

Why it matters:

Are investors not properly reflecting the risks? Maybe, though, that won’t last forever. AllianceBernstein’s chief executive told the FT, “Those people (geopolitical experts) are in high demand…Every Wall Street firm is bringing around people like that for (investors) to meet…there’s a profound realignment happening, and it does spook the hell out of me.”

That could mean investors come to value resiliency over efficiency.

Resiliency > Efficiency: In a stable geopolitical world, differences between companies and financial assets, like whether a stock is listed in China or the U.S., are less consequential, so focus on efficiency reigns supreme.

But if the best company globally in an industry was in Russia and you invested there in 2021 as a result, by 2022, your entire position would be worthless following Russia’s invasion of Ukraine and corresponding Western sanctions.

In that case, it’s less important to invest in the best-run (or most efficient) company anywhere in the world and far more important to invest in assets fundamentally less likely to be brought down by geopolitical fallout.

Yet, being a first mover in anticipating geopolitical crises isn’t usually rewarded in financial markets — an investment manager is unlikely to be penalized for not foreseeing a Black Swan event that everyone missed, but they will be held accountable for underperforming the market by investing too conservatively.

Human nature compels us to keep betting on things that have worked until they don’t anymore, no matter how much lip service is paid to geopolitical risks in the meantime.

Read more (FT)

More Headlines

📈 The countries with the most high-net-worth individuals

💼 Friday’s jobs report shows a cooling labor market, with the unemployment rate slightly higher at 4.1%

🇬🇧 U.K. PM concedes defeat as Labour Party claims landslide victory

🚗 Tesla is now an official Chinese government car

💬 Nerves after the bankrupt exchange Mt. Gox finally begins making payouts to creditors drive falloff in Bitcoin prices

🤔 Why Aren’t Stock Pickers Performing Better?

Made Using DALL-E

If this is supposed to be a “stock picker’s market,” why are many active fund managers struggling to beat the market?

Today’s conditions should theoretically favor stock picking. In fact, the environment appears to be ideal.

The CBOE implied correlation index suggests that stocks are moving in unison less than usual, and dispersion — how widely individual stock returns differ from the average — is abnormally high.

No luck: But evidently, these traditional measures may be less meaningful in today's market because, in the first half of 2024, only 18.2% of actively managed mutual funds and ETFs benchmarked to the S&P 500 managed to beat the index.

That’s down from 19.2% in the first half of 2023 and 19.8% for the full year 2023. Over the past decade, an annual average of just 27.1% of these funds have outperformed the S&P 500.

Concentration: A key factor contributing to active managers' underperformance is the market's extreme concentration.

The three largest stocks in the S&P 500 — Microsoft, Apple, and Nvidia — account for nearly 21% of its total market value. The top five stocks make up 27%, and the top 10 comprise over 36% of the index.

This level of concentration poses a challenge for active managers who typically aim to control risk by diversifying their portfolios. Basically, if you don’t have a decent chunk of your portfolio in a Magnificent Seven company, you’re probably underperforming.

Actively managed U.S. stock funds have an average of 14.2% in their top three holdings and 20.8% in their top five, well below the concentration of the S&P 500. It’s an underweighting of top performers that has hurt their relative performance.

Cold, hard facts: As Jason Zweig of The Wall Street Journal wrote this week, “Portfolio managers can talk all they want about how it’s becoming a stock picker’s market. But, unless they picked exactly these (tech) stocks—and unless they picked massive quantities of exactly these stocks—they aren’t going to outperform anytime soon. Fund managers flinging around statistics can’t change that cold, hard fact.”

From The Wall Street Journal

Why it matters:

It’s another example of how today’s market is all about a few big winners that have outperformed virtually everything else. In essence: We’ve got a handful of winners and hundreds of laggards.

The S&P 500 rose 4.28% in the second quarter, while the Russell 2500 index, which tracks small and midsize stocks, was down 4.27%.

Nvidia alone accounted for nearly one-third of the S&P 500's total return in the first half of 2024. Only five stocks — Nvidia, Microsoft, Amazon, Meta Platforms, and Eli Lilly — contributed 55% of the market's return.

Bottom line: Despite claims of a "stock picker's market," fund managers are unlikely to outperform the index unless they have heavily concentrated their portfolios in these top-performing stocks.

The Executive Upgrade: Dealmaker Pants

Imagine closing a million-dollar deal in pants so comfortable, you forget you're wearing them.

The Dealmaker Pant is the ultimate power move for the modern gentleman. Featuring a timeless design, impeccable craftsmanship, and unparalleled comfort, these pants are the embodiment of understated luxury.

Save 15% with code READ15, exclusive to readers.

Quick Poll

Out-of-office statuses are popping up everywhere as we move deeper into summer — have you taken your "big" vacation yet?

On Wednesday, we asked: Do you currently hold an S&P 500 index fund in your portfolio?

— Roughly two-thirds of readers do. “VOO and IVV,” one said. Another added, “Majority of our stock holdings are in only a handful of index funds. No better way to pace the market than to own the market. Less headache, easier to manage, just need to rebalance as an individual would like, and you'll beat the professionals 80% of the time.”

— Another stated, “If the S&P index were a food, I’d be considered morbidly obese.”

TRIVIA ANSWER

See you next time!

That's it for today on We Study Markets!

Enjoy reading this newsletter? Forward it to a friend.

Was this newsletter forwarded to you? Sign up here.

Use the promo code STOCKS15 at checkout for 15% off our popular course “How To Get Started With Stocks.”

Advertise with us.

Follow us on Twitter.

Keep an eye on your inbox for our newsletters on weekdays around 6pm EST and on weekends. If you have any feedback for us, simply respond to this email.

You can also leave your comments/suggestions/feedback anonymously here.

What did you think of today's newsletter?

All the best,

P.S. The Investor's Podcast Network is excited to launch a subreddit devoted to our fans in discussing financial markets, stock picks, questions for our hosts, and much more!

Join our subreddit r/TheInvestorsPodcast today!

© The Investor's Podcast Network content is for educational purposes only. The calculators, videos, recommendations, and general investment ideas are not to be actioned with real money. Contact a professional and certified financial advisor before making any financial decisions. No one at The Investor's Podcast Network are professional money managers or financial advisors. The Investor’s Podcast Network and parent companies that own The Investor’s Podcast Network are not responsible for financial decisions made from using the materials provided in this email or on the website.