Welcome to the first-ever edition of The Intrinsic Value Newsletter! If you’ve been a reader of We Study Markets, things have changed a bit, but we’re as committed as ever to delivering high-quality financial information to you.

Every week, here and on the sister podcast, I’ll break down a different company's business model, estimate its intrinsic value, and decide whether it should be added to The Intrinsic Value Portfolio—a portfolio of stocks we’ll build together over time.

So today, I'll go through the thesis for Madison Square Garden Sports Corp. (MSGS), the publicly traded holding company that owns the New York Knicks and Rangers.

More below 👇

— Shawn

MSGS: Own The Knicks & Rangers

As mentioned, Madison Square Garden Sports Corp. (MSGS) is a vehicle for owning the NBA’s New York Knicks and the NHL’s New York Rangers.

The thesis is pretty straightforward: Forbes has an excellent track record in estimating the valuations for professional sports teams, and they currently estimate that, combined, the Knicks and Rangers are worth $11 billion ($7.5b for the Knicks, $3.5b for the Rangers.)

At this valuation, you’re, in theory, getting the Rangers entirely for free and a discount on the Knicks. At the time of writing, MSGS trades at a $5.4b equity value and $6.3b enterprise value, which is obviously a considerable discount from what Forbes estimates. And, on average, Forbes ends up typically being a bit conservative in their estimates, too (from 2021 to 2023, 15 teams in major U.S. sports leagues sold partial or full ownership stakes that were, on average, at a 17% premium to Forbes’ valuations — see below.)

Meanwhile, the Knicks have compounded their Forbes valuation at 20% per year for 15 years, while the Rangers have compounded at 9% per year over that same period.

More Than The Numbers

In short, MSGS is a rare opportunity to invest in two premier sports franchises in public markets, of which the two franchises potentially trade for 50-60% of their net asset value.

And that’s before accounting for the decent chance that they’ll continue to compound their value at double-digit rates going forward as they have in the past decade and a half — sports teams are the ultimate crown jewel for billionaires, and there are more billionaires than ever to bid on them, while there is only a fixed supply of franchises in the U.S.’s four major sports leagues.

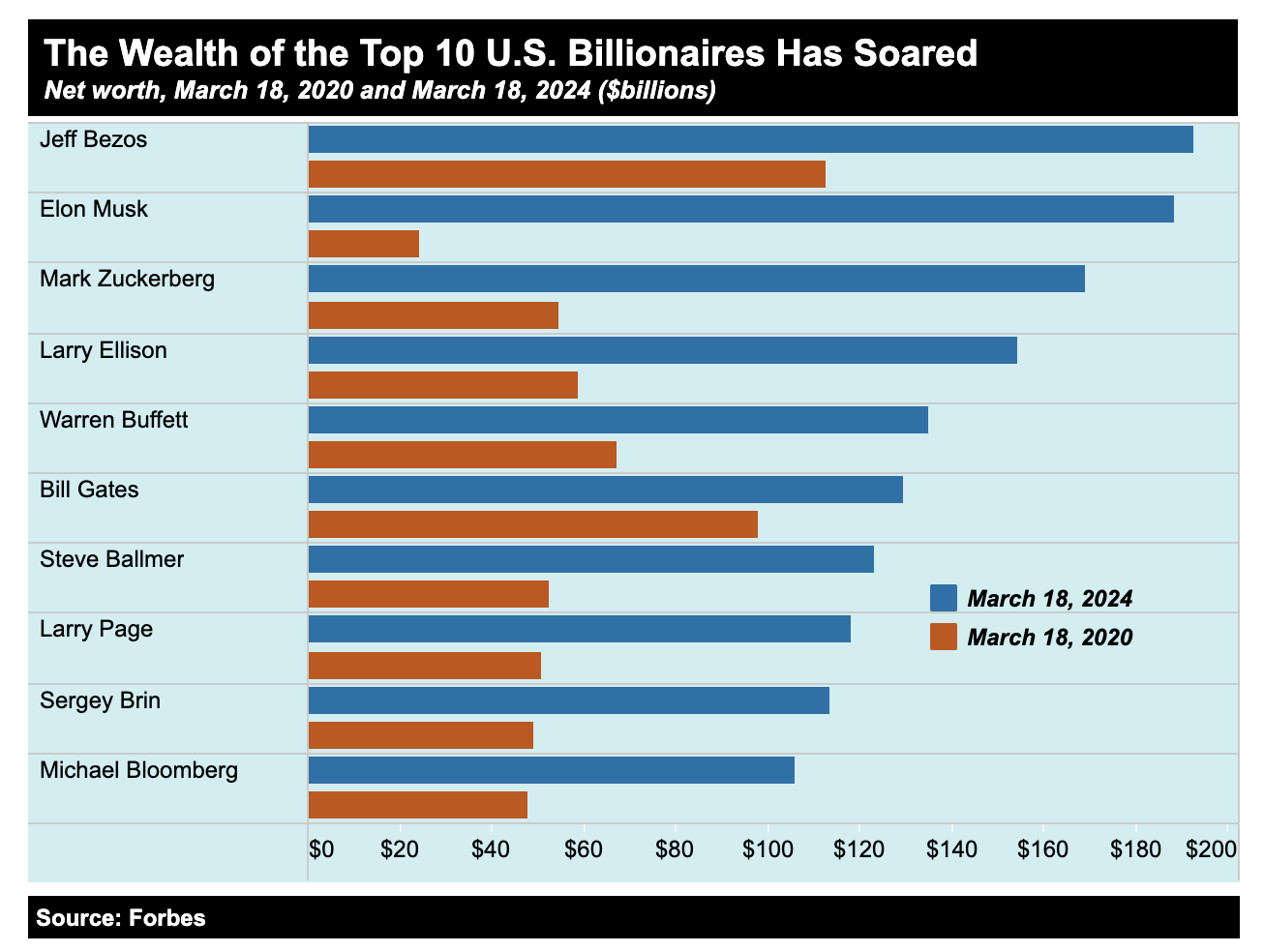

Billionaire wealth has rocketed in recent years, giving them more spending power to use toward trophy assets like sports teams.

There’s a considerable non-economic and egotistical component to buying sports teams. They’re a luxury good for billionaires and the pride and joy of entire major cities. They also elevate billionaires’ status. Jerry Jones and Marc Cuban wouldn’t be household names if it weren’t for their ownership of the Cowboys and Mavericks.

Additionally, there are some very real tax-shelter benefits for buying teams known as the Roster Depreciation Allowance (RDA.)

With the RDA, there’s essentially a double-tax benefit, where not only can MSGS deduct the actual salary costs for players from its income, but it can also amortize the intangible value of its players as “roster assets,” further reducing the income that’s reported to the IRS and saving the company on taxes.

The double benefit arises because, under the RDA, owners amortize the purchase price of the team, player contracts, and other intangible assets like TV contracts and franchise rights over a 15-year span, on top of actual payroll expenses.

This partially explains why sports franchises are such attractive purchases to billionaires. They can effectively be used as a tax shelter, where teams may be cash-flow profitable but can report considerable paper losses that reduce tax liabilities.

When David Tepper paid $2.3 billion for the Carolina Panthers, that produced amortization expenses of around $140 million per year, more than wiping out any of the Panthers’ profits reported for tax purposes.

Why The Discount?

For starters, this is probably a classic sum-of-the-parts value trap. Short of the Dolan family, which controls 70% of the voting rights in MSGS, agreeing to sell the two teams, there are limited ways to realize this differential between what Forbes estimates the two teams to be worth and the value the stock market is willing to place on them.

Add on to this some Succession-like family drama, where most of the Board is run by the Dolan family (and paid generously), and the picture becomes rather complicated.

The family patriarch, James Dolan, is actually the CEO of MSGS and two other public companies: Madison Square Garden Entertainment (MSGE) and Sphere Entertainment (SPHR). And he’s not exactly a good guy, either — he settled a 2007 sexual harassment suit for $11 million and has more recently been sued for allegedly assaulting a woman in coordination with Harvey Weinstein.

MSGS’s Board

While the Dolans are the worst people I’d ever want to run a company I invest in, that is, ironically, part of the bull thesis here. As lawsuits, scandals, and fan resentment stack up, the Dolan family may be forced to sell the teams, which would be a major catalyst for realizing the difference between the stock's market value and the private valuation of the Knicks and Rangers.

For reference, see what happened with Donald Sterling, the Clippers’ former owner, and Dan Snyder, former owner of the Redskins/Commanders.

Besides that, there’s a case to be made for further share buybacks to narrow the valuation gap (MSGS has spent $400m on repurchases since 2015) or even the sale of a sizable minority stake in the team to private equity firms. Still, the Dolan family selling out completely is necessary to really move the valuation gap.

A Range of Outcomes

I see a range of plausible outcomes:

A) Moderate narrowing of the 50-60% gap to Forbes’ estimated NAV provides a tailwind to returns, while the value of the Knicks and Rangers continues to compound.

B) the stock doubles promptly and fully realizes the valuation gap if the Dolans sell both teams.

Or, C) the valuation gap continues to widen in the short-to-intermediate term if the Knicks or Rangers have poor seasons, causing the stock to stagnate or decline modestly.

There are, of course, other possibilities, but those are sort of the overarching ones I see, and over a long enough time horizon, it seems like the odds tilt in favor of things working out pretty well for any new investors today.

There’s a fourth possibility that’s becoming increasingly plausible, though, which would spell trouble for MSGS investors — most of MSGS’s estimated value comes from the New York Knicks, and there’s a chance that, after years of compounding in value, that the Knick’s valuation begins to decline (or, more likely, slow its rate of compounding dramatically.)

Close followers of the NBA will know this well, but the league is struggling on a few different fronts. Players are shooting more 3-point shots than ever, and the league’s grueling 82-game season has led many coaches to embrace the concept of “Load Management,” frequently resting star players with little notice.

Thus, fans have become more hesitant to buy tickets because there’s no guarantee star players will play, even if they’re not injured. Who wants to pay $400 to bring their family to see Lebron James in action, only for him to be a last-minute scratch?

And as mentioned, the proliferation of 3-point shots, plus a litany of rules that favor offensive players, have only worsened the quality of the product in many fans’ eyes, combining together to underpin a substantial decline in ratings over the last decade.

Ratings for this season are down more than 20% year over year and, by some estimates, have fallen by half since 2012.

The league has found ways to continue growing monetization, from squeezing out more favorable media rights deals with TV partners to embracing social media, but structurally, these gains can probably only extend so far if built on top of a declining sport.

I don’t think it’s too late by any means for the NBA to reverse these trends and reclaim momentum in its favor, but it’s something any investor in MSGS should keep an eye on, as it lends credence to the stock market’s pricing of MSGS with reduced implied values for the Knicks and Rangers.

Valuation

I did some rough math below, but in short, if you add up the Forbes estimates of the teams’ value and subtract out net debt, you can estimate the team’s net asset value, aka NAV. From there, I divided that value by the shares outstanding and, for the sake of conservatism, added a 15% discount (85% of NAV).

That spits out a target price of roughly $348 per share. Over the next three years, if the stock converges to just 85% of its 2024 net asset value (while the value of the Knicks and Rangers continues to appreciate), investors would see at least a 16% annual return.

Potentially, even more so, if the Dolans (unexpectedly) sell the teams and fully realize the current estimated values for the Knicks and Rangers.

If, over the next 3 years, the stock closes the gap with current estimates of the Knicks & Rangers values to 85% of NAV (from ~50%), the stock would generate a 16% annual return

Conclusion

Is MSGS a good long-term bet? Maybe.

That three-year rate of return sounds enticing until you consider that it’s a completely arbitrary timeline — there’s nothing besides the hope that the Dolans will sell all or part of the team within three years or repurchase stock far more aggressively than they previously have, to explain why MSGS's stock would close the valuation gap with Forbes’ estimates.

My hangup is that the Knicks' and Rangers' underlying businesses aren’t that great. In part, that’s because players have a lot of leverage and can demand salaries that are a considerable chunk of teams’ revenues. Also, the business fluctuates dramatically with how well the teams are doing on the court or on the ice, making earnings very volatile.

When the Knicks or Rangers have a bad season, ticket revenues, merch sales, and food & beverage sales can fall off dramatically. With both teams actually having done well lately, that success is priced in, and the risk is more skewed toward the teams falling short of expectations.

While I don’t have any reason to argue that the Knicks aren’t worth almost $8 billion to a motivated buyer, I also don’t want to premise long-term investments around the price others are willing to pay for things. Even if there’s precedent for Forbes’ estimates being realized, these numbers are still just subjective estimates.

In other words, if the business behind the Knicks and Rangers were of higher quality, I would be more confident in their estimated valuations. Based on actual cash flows, MSGS is worth a fraction of the value I estimated above. So, the thesis boils down to whether you a) trust the estimates from Forbes, b) believe that, as a trophy asset, sports teams will continue to sell for more and more every year, and c) think the stock’s valuation gap with Forbes can or will close in the coming years.

Without a clear sales catalyst to close the gap with the company’s estimated net asset value and better business opportunities elsewhere, I’m inclined to pass on MSGS for now and not add it to The Intrinsic Value Portfolio. Still, I can completely understand the bull thesis, and it’s a decision I may change my mind on down the road.

Am I wrong? Let me know what I missed by hitting reply to this email or leaving your feedback in the poll at the bottom of this newsletter.

For the complete breakdown, listen to my podcast on MSGS here.

Weekly Update: The Intrinsic Value Portfolio

Quote of the Day

"I never attempt to make money on the stock market. I buy on the assumption that they could close the market the next day and not reopen it for five years.”

— Warren Buffett

What Else I’m Into

📺 WATCH: Why the NBA might be dying

🎧 LISTEN: The Art of Thoughtful Wealth Creation with William Green

📖 READ: Pitch for Madison Square Garden Sports on the Value Investors Club (free to read with email sign-up)

Your Thoughts

See you next time!

Enjoy reading this newsletter? Forward it to a friend.

Was this newsletter forwarded to you? Sign up here.

Use the promo code STOCKS15 at checkout for 15% off our popular course “How To Get Started With Stocks.”

Follow us on Twitter.

Keep an eye on your inbox for our newsletters on Sundays. If you have any feedback for us, simply respond to this email or message [email protected].

What did you think of today's newsletter?

All the best,

© The Investor's Podcast Network content is for educational purposes only. The calculators, videos, recommendations, and general investment ideas are not to be actioned with real money. Contact a professional and certified financial advisor before making any financial decisions. No one at The Investor's Podcast Network are professional money managers or financial advisors. The Investor’s Podcast Network and parent companies that own The Investor’s Podcast Network are not responsible for financial decisions made from using the materials provided in this email or on the website.