What’s more American than Levi’s blue jeans and apple pie?

Well, honestly, probably nothing, but John Deere is in contention. Few brands have left a bigger cultural mark on rural America than Deere. Throughout America’s heartland and from coast to coast, people proudly don hats with Deere’s signature logo and green & yellow branding, while inheriting Deere equipment is something of a rite of passage for the next generation of family farmers nationwide. 🚜🌾

But Deere isn’t just some old-timey, blue-collar brand; it’s a tech company, a manufacturer, and a financial services business all wrapped into one. And the tech focus is an increasingly large part of the story.

More below on everything you could ever want to know about Deere’s iconic brand, business, valuation, and whether it earns a spot in our exclusive Intrinsic Value portfolio of attractively priced, high-quality stocks — in just a few minutes to read.

— Shawn

John Deere: Good Ol’ American Ingenuity

Deere’s story begins nearly 200 years ago when John Deere himself established the company in Illinois in 1837 after designing a steel plow that was far better suited for the sticky soil of the Midwest Prairie than the more common cast-iron plows of the day.

Deere distinguished himself further by not just designing a better plow but also by embracing a more commercial mindset. Instead of humbly waiting for someone to order a plow to start building it, he realized that he could improve the customer experience by building his plows in advance, storing them as inventory, and then delivering them as soon as a customer had finalized the purchase. This had the added benefit of enabling prospective customers to see and try the plows for themselves before purchasing.

Word of Deere’s improved and easy-to-purchase plows spread across the corn belt, and he was soon selling hundreds and eventually thousands of plows each year.

A few years later, John Deere adopted its iconic leaping-Deer logo, but it wasn’t until 1918 that the company began producing what it’s most famous for now: tractors.

John Deere’s first tractor, the “Waterloo Boy”

Tractors are the lifeblood of John Deere, though the company has grown to become a giant in the broader agricultural, forestry, and construction industries. Deere’s reputation for quality across product lines has long preceded it, too, driven by the now-famous tagline “Nothing Runs Like a Deere.”

But this marketing magic almost never was. The story goes that as a last-ditch effort, an advertising agency copywriter rifled through discarded headline ideas in his trash can for Deere’s new line of snowmobiles — only to then re-discover what would become a staple of one of the world’s most recognizable brands.

Yet, we are here to discuss John Deere as an investment in 2025. Surely, if we could spin back the clocks 100 years, we all would have invested in it (you’d actually have to spin back the clock 113 years to 1912 to participate in its New York Stock Exchange IPO.)

Tech Company?

Still, to survive and thrive for as long as Deere has as a company is telling of its continued quality and winning culture. Deere today still sells heavy machinery, but its focus is increasingly on cutting-edge technology.

These are not ‘dumb’ machines that Deere sells. We’re talking about equipment so productive and important that it underpins the very existence of our modern world. Using less land and labor than ever, machines like the ones Deere makes have made farming increasingly sophisticated at keeping billions of people fed.

Starlink-powered satellite internet, advanced GPS systems, machine vision to identify weeds and damaged crops in real-time, autonomous self-driving and electric tractors, planters that can shoot out over 1,000 seeds per second, and a virtual command center mapping out everything happening across a farmer’s acreage — this is what I mean when I say Deere is much more high-tech than you might first think.

Deere’s See & Spray technology can, as mentioned, recognize weeds or diseased crops on a second-to-second basis and then spray the perfect portion of herbicide to kill the unwanted flora, reducing the amount of herbicide farmers use by as much as two-thirds.

Deere’s equipment has thousands of sensors that work together to form a digital map of a farm, which can then be used for simulating different scenarios and making recommendations to farmers on the most optimal ways to do things, from the most efficient path to drive their tractors on to the types of crops they should grow or how to respond to weather events.

This video is a great illustration of Deere’s tech at work.

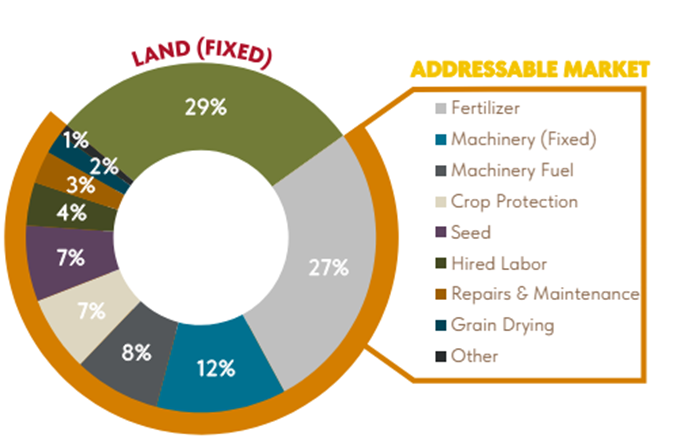

From a business perspective, Deere’s machinery pays for itself by saving farmers on costs elsewhere (fertilizer, pesticides, seeds, time, etc.). So, farmers need to upgrade their equipment every few years to stay up-to-date on the latest efficiency-enhancing technology since cost is the primary thing they compete on in commodity production.

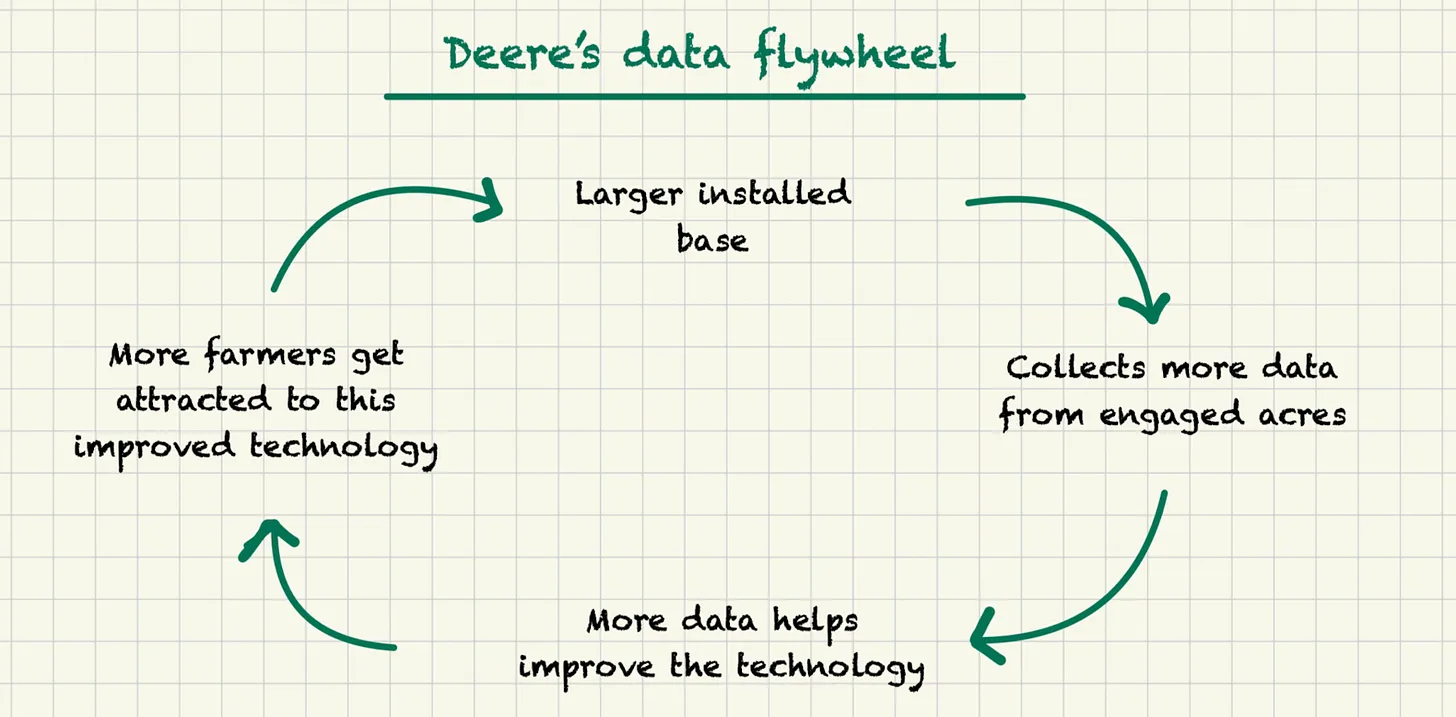

But all of these software offerings fundamentally change Deere’s business model from machine sales & maintenance to recurring subscription revenues, data packages, and high-tech equipment add-ons.

Breakdown of costs for farmers

While Deere’s business has always been cyclical, as farmers collectively delay major purchases in ‘bad years’ when poor weather, crop disease, or interest rates make it a less-than-ideal time to ~ pay the price of a new house ~ for an updated piece of equipment, software subscriptions are generating higher-margin and more recurring revenues that nerf some of the undesirable fluctuations in the company’s business.

By 2030, Deere’s management hopes that 40% of its revenues will come from recurring services, including routine parts sales and maintenance, as well as subscriptions.

That maintenance and servicing is a big part of the story: Deere’s competitive advantage lies, in part, in its vast network of dealerships, particularly in the U.S. but also worldwide, which makes it comparatively far more convenient to own a Deere since a dealership is never too far away to assist.

Farmers work on tight margins with compressed periods (tilling, planting, harvesting) to cram their work into, so they cannot afford to have important equipment offline for extended durations. And as tractors and combines have gotten more advanced, the more specialized it has become to service them, making it all the more important to be able to quickly have maintenance done.

Financial Services?

Revenue breakdown — Production & Precision Ag is the largest component

Beyond the promises of a tech-led transition that can materially improve the quality of Deere’s business (in terms of profit margins and recurring-ness/reliability), Deere has long run a financial services division that generates a bit less than 8% of its revenues.

This in-house financing serves solely to drive more equipment sales and, again, is a competitive advantage in a way. Given that we’ve already established a large piece of farm equipment could cost as much as or more than a new house, being able to provide loans directly to farmers hugely streamlines the purchasing process compared with having to get a loan from a local bank.

Since Deere isn’t actually a bank, its Financial Services division has to effectively borrow money from others, fortunately at very low interest rates — thanks to Deere & Co’s nearly pristine credit rating — and then lends out those funds to customers to finance equipment purchases at higher interest rates, capturing the spread between what rates they borrow and lend at as profit.

This has the added benefit of making the purchasing process easier for customers and also boosting cash conversion, as Deere Financial can ensure that the loan proceeds are used to pay Deere’s manufacturing team upfront.

In other words, Deere Financial ensures the manufacturing team is paid when products are delivered, while customers repay Deere Financial over time with interest.

Having the company take on this leverage and credit risk head-on is certainly a risk, but it’s important to remember that Deere probably knows its customers better than anyone after having served farmers for almost two centuries and now collecting a vast amount of data on their operations.

Relatedly, Deere Financial is lending against the company’s own equipment as collateral. They know exactly how much a used machine is worth and that is backstopping their loans.

When you look at Deere’s balance sheet, it appears to have an inordinate amount of debt (~$60 billion), but most of this is tied to the financial division, so Deere’s operations have a much more conservative financial position (~$5-6 billion in net debt.)

Deere has an excellent track record in disciplined lending and has managed to do so profitably throughout the business cycle, so this isn’t a major concern for me, but any investor in the company should get comfortable with this dynamic and understand how its financial services division affects the overall business.

Valuation

So, where does that leave us? There’s a lot to like about Deere’s resilience, customer loyalty, brand power, and industry-leading positions in both market share and technology. Of course, we want to know how that all translates into value for shareholders who own the business.

I will say upfront that Deere is by no means an easy company to create a simple valuation for. Considering its cyclical sales, R&D spending on new technology, and financing division can all be real complicating factors.

Since Deere remains an inherently cyclical business tied to capex spending cycles for machinery, I used a framework from Aswath Damodaran — a globally revered professor of finance at NYU — for valuing cyclical companies to guide me.

In short, he advises looking at a company’s average operating margins over the last decade, which are easy to find and calculate using a service like Finchat.io, as shown below.

See bottom row

Instead of trying to guess where we are in the sales cycle for a company like Deere, you can multiply this average profit margin by whatever the company’s revenues are over the past year to get a ‘normalized’ estimate of operating profits.

With an estimate for the profits Deere’s operations can generate in a normal year, using a few variables, you can then guesstimate the present value of all of Deere’s future operating profits. The formula is a little messy, so I copied it below.

The growth rate (or “g”) is the rate at which the company can grow long-term, and for the sake of conservatism, I put this in line with inflation at 2% to assume no real growth. And then, as mentioned, I just pulled the company’s historic returns on capital, tax rates, and cost of capital according to Finchat and plugged them in.

That gives a present value of the company’s lifetime operations, and then you just make some adjustments to that number by adding in cash (an asset), subtracting out debt (a liability), and dividing by the number of shares outstanding to get a target share price.

Below, on the left, you’ll see the numbers I used and the value per share I got on the right.

That obviously suggests that the stock is priced too expensively today at over $450 per share, but this oversimplified model doesn’t reflect that technology and software subscriptions are structurally improving Deere’s profitability, so averaging their results over the last decade may not be the best indicator of their normalized future profit margins.

As a result, I crunched the numbers again using a revised operating margin of 20% based on what management has said they expect to average going forward, and that naturally gave a higher valuation but still suggested the stock was trading at a premium.

To be even more aggressive, we could not only use management’s target average margins but also account for the fact that 2024 was a downcycle year, where revenue was only 80% of what management thinks they can earn "mid-cycle.” So, by normalizing both revenues and margins, I can get a valuation that says the stock is slightly undervalued, but it’s a stretch:

For the record, I don’t do these exercises to generate strict price targets. Even simple models like this are fraught with assumptions. For example, slight changes to the cost of capital (aka “WACC”) can dramatically change a company’s estimated valuation, and as I’ve shown, changing the company’s average operating margin to 20% from 14% can add over $100 of estimated value per share, and there’s no simple answer for which one will be more representative of reality in the future.

Charlie and Warren don’t exactly think highly of relying on cost of capital calculations as discount rates, either.

As such, take that all with a grain of salt, but you’re welcome to play around with my model here for illustrative purposes.

More tangibly, I like to look at the free cash flows companies can produce (this is effectively what is left over after accounting for operating expenses, reinvestments, and removing the effects of non-cash accounting adjustments.)

Free cash flows are what drive returns for stock investors implicitly or directly through dividends & share buybacks, and so the free cash flow yield (the amount of free cash flow per share relative to the price of the stock) is an important metric to look at in understanding a company’s valuation.

Deere’s free cash flow yield is around 3.6%, but if you believe management’s guidance that 2024 was a below-average year where the company earned about 80% of what it can on average over time, then the company’s ‘normalized’ FCF yield is 4.5% (3.6%/0.8).

As such, assuming Deere didn’t grow at all and its valuation multiple didn’t expand or contract, we would expect to earn an average of 4.5% per year over the next 5-10 years — derived directly from that FCF yield.

Of course, Deere will continue to grow its sales and earnings (net income grew at 15.5% per year over the last decade), and that will only enhance expected returns. If Deere can grow free cash flows by 5.5% per year going forward, adding that to the existing FCF yield already implies a 10% annual return.

And, if you really believe in Deere’s technology and ability to earn more recurring revenues, then that quality would very likely be rewarded by the market in the coming years with a higher average price-to-earnings ratio that would further boost returns beyond 10% per year.

Portfolio Decision

That all sounds pretty good, so why am I deciding not to add Deere to The Intrinsic Value Portfolio? I suspect the answer will become something of a common excuse in this newsletter: Deere falls into my too-hard pile.

Merit points aren’t given for working harder at finding decent investments. Hard work can certainly help you uncover opportunities, but hard work for the sake of working hard isn’t always productive, and I prefer not to make investing any harder than it already is.

That insight isn’t unique as many great investors follow the idea of having a too-hard pile, where they just can’t fully wrap their head around an investment for some reason, so instead, they just move on to the next. There are thousands and thousands of companies globally to invest in — I’m not anywhere close to having to worry about running out of options.

There are all sorts of accounting considerations for treating Deere more like a tech company, such as capitalizing spending on R&D as assets on the balance sheet rather than expensing them immediately, and the financial services division introduces a whole lot of leverage and different risk dynamics that I’m not too comfortable with, either, on top of the fact that Deere is still a cyclical company, meaning its results do not come in a straight line, up and to the right, that’s easy to value.

I grew up in the suburbs, and even though I’d heard of John Deere, something about it is less intuitive to me than Ulta, which I added to the portfolio last week. I’ve been inside Ulta stores dozens of times, I know plenty of women who love Ulta’s beauty products, and they operate a relatively straightforward retail business that doesn’t rely on technology in nearly the same way as Deere, so I feel much more comfortable thinking through the thesis with Ulta.

With Deere, I worry there’s an element of “not knowing what ya don’t know,” and there’s a lot I don’t know about agriculture. That said, I do find the company compelling, and maybe one day I will feel as though I understand Deere well enough. I wouldn't be surprised if the company earned 10%, 15%, or 20% returns per year if they really deliver some of the innovations they’ve hinted at.

But for now, I’m happy with concluding that Deere is approximately fairly valued and moving on because I’d rather miss out than get burned by a business I don’t understand.

So, next week, I’ll be back again in your inbox breaking down another interesting business, looking for a second addition to the portfolio. And let me know your thoughts on my decision in the poll at the bottom of this email.

For more on Deere, listen to my full episode on the company here, and check out this excellent write-up from Leandro of Best Anchor Stocks.

Weekly Update: The Intrinsic Value Portfolio

No additions made this week

Notes

Just one holding in the portfolio so far: Ulta

Ulta has risen ~3.4% since being added to the portfolio last week at an average price of $404.68

The portfolio’s returns effectively resemble cash at the moment with a 95% cash weighting — building a concentrated stock portfolio takes time and patience

Quote of the Day

"Know what you own, and know why you own it.”

— Peter Lynch

What Else I’m Into

📺 WATCH: How Dicks Sporting Goods made billions killing their own stores

🎧 LISTEN: Sol Price, the retail visionary behind Costco

📖 READ: How Countries Go Broke (an early excerpt from Ray Dalio’s new book)

Your Thoughts

Do you agree with Shawn's decision on John Deere?

Last week, readers mostly agreed with the decision to add Ulta to the portfolio. Here are some of the comments:

“Thank you for going out of your way in writing your thesis on Ulta. It does sound compelling, and as you stated, in spite of its vicissitudes, it’s still running its business with the correct survival mindset to streamline its core operations.”

“ULTA is a great stock. They have really high ROIC in an industry where that’s hard to find. The only hesitation I have is that, at one point, it was in Buffett’s portfolio, and then a few months later, he sold it. It’s likely Todd or Ted bought this, not Buffett. That being said, it’s hard for me to buy something Buffett sold — why did he buy it and then sell it a few months later? What does he see that I don’t? That’s why I haven’t pulled the trigger.”

“Ulta is a growth company transitioning into a mature company. Is simply buying back shares enough to compensate for that? In the US they have built out their footprint of stores — very few locations left for new stores. Their locations within Target don't seem to be very profitable. Target may be getting the better of that deal. Their experiment in Mexico may or may not succeed. Very few US retailers are able to transition their formats to meet the tastes of foreign shoppers.”

“It's a logical breakdown, but I'm curious about what’s driving the valuation multiple compression. My thoughts are possibly two difficult to deal with issues. One being changing views on beauty or maybe just more volatility as we continue to see more drastic shifts in belief systems for digital-first generations (z and alpha). Secondly, the store locations are a strong moat assuming suburban demographics remain stable, there is a question here as well around location of their target customers and how the appeal of suburban life again changes with generational shifts. That said, it's a very similar business to Druni in Europe, which has a very similar product range but focuses on urban locations.”

See you next time!

Enjoy reading this newsletter? Forward it to a friend.

Was this newsletter forwarded to you? Sign up here.

Use the promo code STOCKS15 at checkout for 15% off our popular course “How To Get Started With Stocks.”

Follow us on Twitter.

Keep an eye on your inbox for our newsletters on Sundays. If you have any feedback for us, simply respond to this email or message [email protected].

What did you think of today's newsletter?

All the best,

© The Investor's Podcast Network content is for educational purposes only. The calculators, videos, recommendations, and general investment ideas are not to be actioned with real money. Contact a professional and certified financial advisor before making any financial decisions. No one at The Investor's Podcast Network are professional money managers or financial advisors. The Investor’s Podcast Network and parent companies that own The Investor’s Podcast Network are not responsible for financial decisions made from using the materials provided in this email or on the website.