You’ve heard it all before. “The Amazon of China.” “The Amazon of Latin America.” “The Amazon of Africa.”

There is only one Amazon, and if you were fortunate enough to invest in it at any point in the past 25 years and continue to hold it, you’ve done quite well.

Coupang is not exactly Amazon, but it’s impressive in its own ways.

It’s a company whose delivery times actually put Amazon to shame, with an ecosystem of valuable services for its members that much resembles Prime.

Today, I’ll go through the intrinsic value of Coupang, the South Korean e-commerce and technology giant you’ve probably never heard of.

More below, in just a few minutes to read.

— Shawn

Coupang: The Amazon of Korea

Despite operating primarily in South Korea, Coupang has traded on the New York Stock Exchange for almost four years but still hasn’t surpassed its original IPO price.

Yet, Coupang grew revenues by 40% per year from 2018-2023 and now does around $27 billion in annual sales. In a decade, the company’s revenues went from $350 million to $20 billion(!)

After the IPO, the stock tanked and traded sideways in mid-teens territory for over a year, although the financials improved each quarter. Coupang’s bumbling stock performance stems largely from too much hype around the IPO, combined with poor sentiment around Asian stocks, as well as increased competition from Chinese e-commerce companies.

Still, with a population of 52 million, nearly half of South Korea’s residents have recently used Coupang, and nearly a third are enrolled in its version of Amazon Prime, Rocket WOW.

Coupang has, in short, captured the hearts — and wallets — of nearly every household in South Korea in less than 15 years.

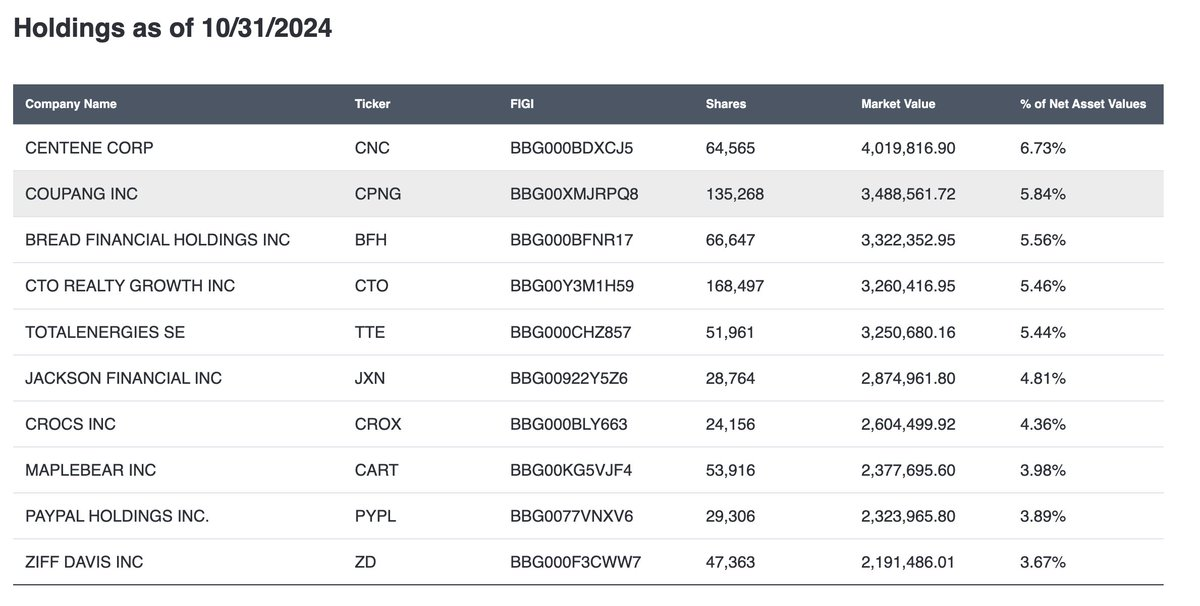

It has also caught the attention of some legendary investors, becoming a key holding of Bill Miller’s investment firm, Miller Value Partners. Miller is best known for recognizing the original value of Amazon years before anyone else, and you might say he sees something forming here with Coupang.

Miller Value Partner’s Portfolio

Jaw-Dropping Convenience

In a way, Coupang is a fusion of the best that America and South Korea have to offer. Headquartered and listed in the U.S., Coupang operates primarily in South Korea, with early backing from some of America’s biggest venture capitalists and a South Korean founder who lived in the U.S. for years and studied at Harvard.

That founder is Bom Kim. While much less widely known than Jeff Bezos, Kim has taken inspiration from Amazon and quietly built Coupang into South Korea’s most dominant e-commerce platform.

Coupang’s AI-powered, automated warehouses and fulfillment centers are a sight to behold, enabling some truly breathtaking efficiency.

One of Coupang’s automated fulfillment centers

For the vast majority of Koreans, whether ordering new socks or groceries for the week, all they must do is place an order before going to bed, and by 7 am the next morning, it’ll be on their doorsteps.

Something wrong with the order? Simply set it back outside your door — no packaging needed, and a Coupang employee will pick it up and immediately refund you.

Coupang’s unrivaled focus on convenience is tied intimately with South Korean culture, a broadly tech-savvy country that lives in dense cities and works more hours each week than any other developed nation.

For millions of South Koreans daily, streaming TV shows, watching live sports, ordering groceries & restaurant meals for delivery, and purchasing household items all go through Coupang.

Rocket WOW

If that sounds a lot like Amazon Prime’s bundle of services that’s because, well, it is. Even down to the percentage of median household income that Coupang charges South Koreans for its Rocket WOW memberships, it’s almost exactly the same as what Amazon charges Americans for Prime.

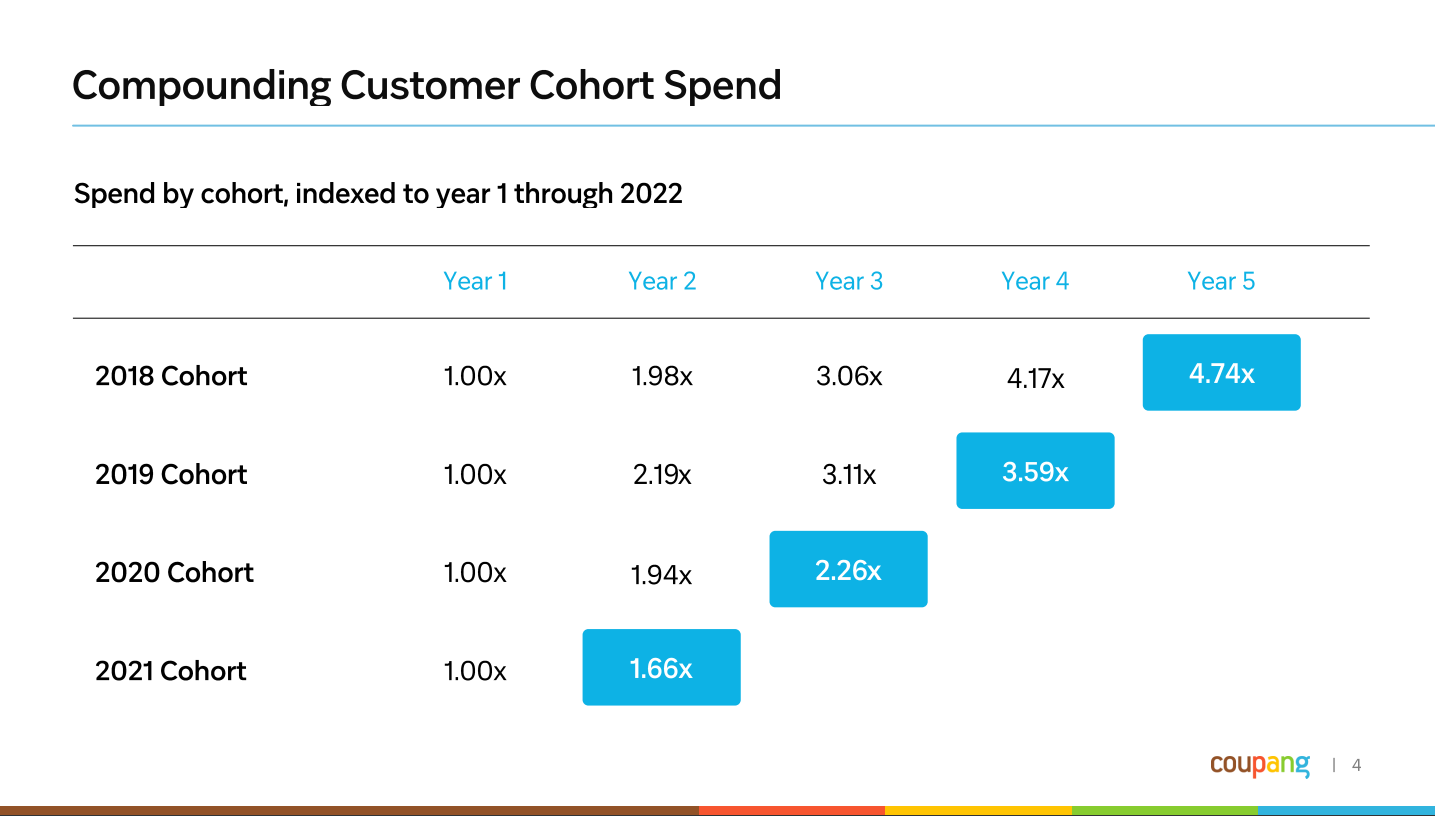

For about $5.70 per month, Coupang subscribers get streaming, lightning-fast delivery times for anything they want, and significant discounts on food & grocery deliveries. All that value for customers creates many different touchpoints that keep shoppers in Coupang’s ecosystem, spending increasingly more each year that they’re a Rocket WOW member.

Customers tend to spend more with Coupang the longer they’re subscribed

And raising prices by 58% in 2024 hardly put a dent in subscriptions, a testament to the customer loyalty Coupang has built up over the years, as it tirelessly works to solve problems for customers they didn’t even realize they had.

Some basic math tells us that Coupang probably earns close to $1 billion per year in revenue from its RocketWOW memberships, with much of the rest of the company’s revenue coming from 1st-party e-commerce sales (where Coupang sources inventory itself and sells products directly) and a small but growing 3rd-party e-commerce business (where Coupang fulfills orders for other merchants who tap into its logistics networks and pay fees to do so.)

Additionally, Coupang wields a small but, if Amazon is any guide, promising advertising business. That’s because, as you can imagine, there are thousands of different types of products you can buy on Coupang, and sellers vying with each other to rank at the top of search results for, say, “ankle socks” might pay a lot to do so.

Promoted search results have turned Amazon into one of the world’s biggest advertising businesses, and as Coupang increasingly integrates more 3rd-party merchants onto its platform, the more opportunity there is to pit them against each other to rank first while Coupang collects advertising dollars along the way.

Advertising makes up about 9% of Amazon’s total revenues and is higher margin than retailing, and if Coupang can even just grow advertising to 5% of its total revenues in the next few years, that will be a massive boost for revenues and profitability.

Not Quite The Same As Amazon

Amazon and Coupang differ in a few important ways. Firstly, Amazon dominates a far bigger market (the U.S. vs. South Korea), has had more success expanding globally, and runs more diversified business units, including its hugely profitable cloud-computing division — AWS — as well as other services like music-streaming, a podcast platform for listening and hosting, prescription drugs, and one of America’s largest grocery chains: Whole Foods.

Despite having penetrated the South Korean market very deeply, Coupang is just a younger company, so it hasn’t built out as many ancillary businesses yet nor found the same traction in new markets. However, the company is investing hundreds of millions of dollars into building a logistics footprint in Taiwan — a country with half the population as South Korea plus well-established competitors, including Amazon itself.

If you sense my skepticism, that’s because I am skeptical. In the last year or so, Coupang claims to have doubled its monthly active customers in Taiwan, yet its market share there is still negligible. Building a new logistics footprint from scratch is no small endeavor, and after Coupang already tried one failed expansion into Japan, I will be betting against them until they prove me wrong.

Still, there’s plenty of room to monetize its South Korean base further, whether by adding more third-party merchants to the platform to offer a wider selection of goods, boosting order volumes, or scaling up its advertising business in sponsored search, banner ads, or sporting rights (Major League Baseball’s 2024 season-opening kicked off in South Korea, and the event was available exclusively in the country to RocketWOW members).

Another differentiating factor for Coupang is its focus on luxury. The company hopes to bring ultra-fast shipping and convenience to the world of high-end beauty products and fashion through R.Lux and Farfetch. After acquiring Farfetch out of bankruptcy last year, Coupang seems well on its way to turning around the troubled luxury clothes e-retailer.

Valuation

With all of this said, how is one to think about valuing a company like Coupang?

With Coupang, I want to take a similar but different approach from classic discounted cash flow models by estimating the lifetime value of a RocketWOW subscriber and extrapolating from there the company’s value.

The focus, then, is on how many subscribers Coupang has and can likely grow to, and how profitable the average subscriber is, which I see as the key metrics of success for the company — Coupang will live and die by its RocketWOW memberships.

As a fair warning, I’m going to do some math here for those who are interested; otherwise, skip ahead to the next section on my final decision. You can click HERE to access the Excel model I used to evaluate Coupang and follow along with the math below.

Math

RocketWOW memberships are the foundation of Coupang’s business model, and thus, valuing them is my primary focus.

For context, with 14 million RocketWOW members, that’s $964 million in membership-fee revenue yearly ($5.74/month * 12 months * 14,000,000 subs).

Additionally, according to Bom Kim's comments, RocketWOW members order nine times more frequently each year than non-members and two-thirds of Coupang’s users are members. Thus, RocketWOW members generate a lot of revenue in excess of what they pay in monthly or annual fees.

Based on its latest filings, in constant currency terms, Coupang earns $318 per active customer each quarter — not member, but customer. In the next two lines, I’ll rework this to estimate how much revenue is earned annually per member:

$318 quarterly comes out to an average of $1,272 annually of net revenue per active customer

That average of $1,272 per customer breaks out to roughly $1,820 per WOW member but only $202 per non-member (hence, WOW members spend 9x more.)

In my basic model, I also assume that net revenues per customer continue to grow modestly over time, given that members have been shown to spend more the longer they are subscribed.

Now that we know approximately how much revenue a WOW member generates per year, we want to next determine the lifetime value of RocketWOW memberships to shareholders.

For that, we need to determine the churn rate. In other words, what percentage of current members cancel their subscriptions?

Looking at Amazon Prime as guidance here, annual subscribers have a churn rate of about 3%, and monthly subs have a churn rate closer to 30%, which equates to a weighted average churn rate of 8.4%. That makes the average expected subscription tenure 11.9 years (1/0.084).

I’m going to assume the churn rate is similar for Coupang. Thus, the very rough estimate of lifetime revenue per member is: $25,903 ($1,820 * 11.9 years).

To determine the value of existing members to shareholders: Slap on a normalized profit margin to these lifetime revenues (I went with a 5% estimate, in line with industry norms), multiply by the number of remaining subs each year who haven’t churned away, and discount these future profits to account for the time value of money. After doing all that, I get a value of existing RocketWOW members to shareholders of about $12 billion.

*Full chart not shown, extends to 2034 and set to begin at end of 2024 — Existing subs are worth roughly $12 billion

And, of course, Coupang will continue to grow. Over the next five years, if Coupang can add another 5 million net members across Korea and Taiwan, that ends up creating another $7 billion in value for shareholders by my math.

Expected future subs are worth roughly $7 billion

I mentioned it a bit earlier, but Coupang has the chance to really grow its advertising business surrounding its product marketplace. Over the next five years, if its ad biz can grow from effectively 0% to 2% of revenue (compared to 9% for Amazon) and can continue to grow modestly from there, given the higher profitability of advertising, this creates another $7 billion or so in value for shareholders.

All in all, that’s $12 billion of value from existing members, $7 billion from potential new members, and $7 billion from its yet-to-be-scaled advertising business for about $26 billion in estimated intrinsic value versus the stock’s current valuation with a roughly $40 billion market cap.

Final Thoughts

So, I’ve decided not to add Coupang to our Intrinsic Value Portfolio, largely because it falls into the too-difficult pile for me. I think you can make a case for why it’s worth much more than $26 billion, but at the same time, I don’t feel as though my assumptions are that conservative, either.

The point being: It’s not obvious to me that I need to drop what I’m doing and invest in the company despite its operations being very impressive. It’s not screamingly cheap, nor is it clear how much of the value it creates for society will accrue to shareholders.

And I’m not from Korea, so I can’t even use Coupang, and I certainly don’t have a strong grasp on the nuanced cultural differences between, say, expanding in Korea versus Taiwan. When you consider all the technology involved here, the complexity of the operations, and all of the competition in e-commerce, it becomes a lot to wrap one’s head around.

I can confidently say Coupang is well beyond my circle of competence. I will continue to wait patiently for great businesses that I can understand, trading at fair prices, to buy and hold long-term in our Intrinsic Value Portfolio.

But I want to know your thoughts on Coupang. Email me at [email protected] with your reflections. If there’s something I’ve overlooked, I’d love to know.

If you’re curious to learn more about Coupang, you can listen to my full podcast about the company here.

Weekly Update: The Intrinsic Value Portfolio

— Still no holdings yet; I’ll be back again next week with another prospective investment to add as the first position!

Quote of the Day

"What we need to do is always lean into the future; when the world changes around you and when it changes against you — what used to be a tailwind is now a headwind — you have to lean into that and figure out what to do because complaining isn't a strategy.”

— Jeff Bezos

What Else I’m Into

📺 WATCH: How a Harvard dropout built South Korea’s most-valuable start up

🎧 LISTEN: My journey into Financial Independence with Stig Brodersen

📖 READ: How Coupang conquered South Korean e-commerce

Your Thoughts

See you next time!

Enjoy reading this newsletter? Forward it to a friend.

Was this newsletter forwarded to you? Sign up here.

Use the promo code STOCKS15 at checkout for 15% off our popular course “How To Get Started With Stocks.”

Follow us on Twitter.

Keep an eye on your inbox for our newsletters on Sundays. If you have any feedback for us, simply respond to this email or message [email protected].

What did you think of today's newsletter?

All the best,

© The Investor's Podcast Network content is for educational purposes only. The calculators, videos, recommendations, and general investment ideas are not to be actioned with real money. Contact a professional and certified financial advisor before making any financial decisions. No one at The Investor's Podcast Network are professional money managers or financial advisors. The Investor’s Podcast Network and parent companies that own The Investor’s Podcast Network are not responsible for financial decisions made from using the materials provided in this email or on the website.